Lecture Charts

29 static PDF charts from the Bantleon Methods lecture. Click any thumbnail to open the full PDF.

Introduction & Motivation

00. Lecture Roadmap

Overview of topics and structure

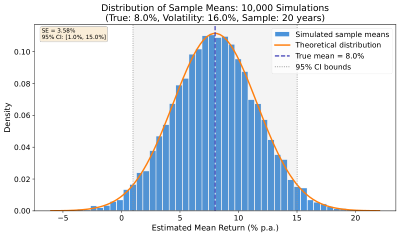

01. Return Estimation Error

Sample mean vs true mean uncertainty

01b. Estimation Error Simulation

Monte Carlo demonstration

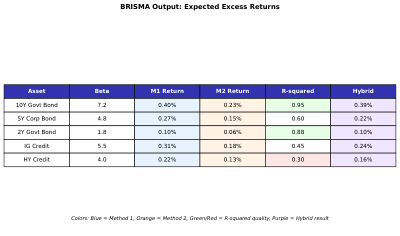

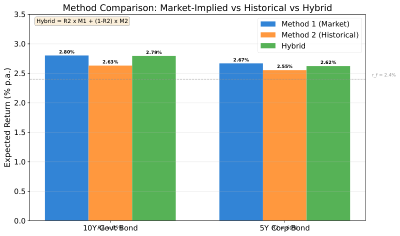

01c. Methods Comparison

M1 vs M2 vs Hybrid overview

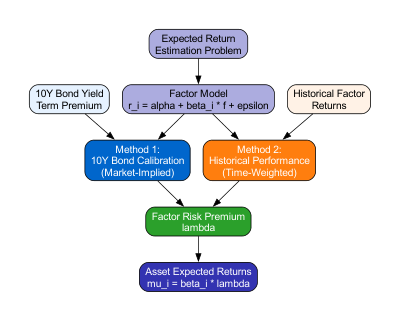

Factor Model

02. Factor Decomposition

r = B*f + epsilon breakdown

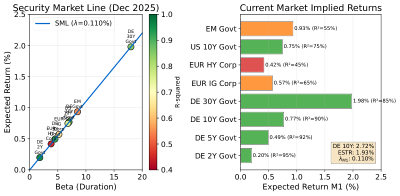

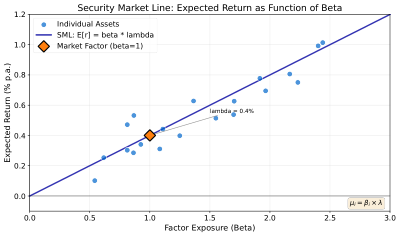

02b. Beta-Lambda Scatter

Asset betas vs implied returns

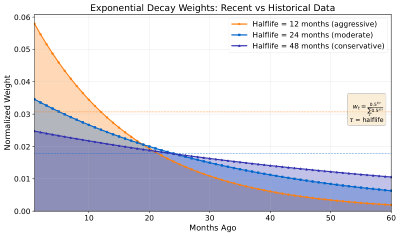

02c. Calibration Concept

How lambda is calibrated

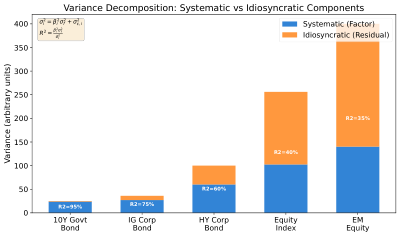

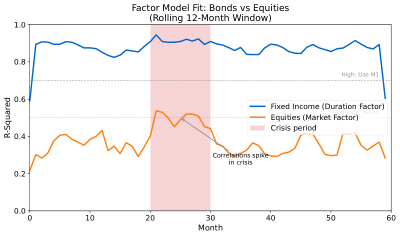

02d. Rolling R-Squared by Asset

Time-varying explanatory power

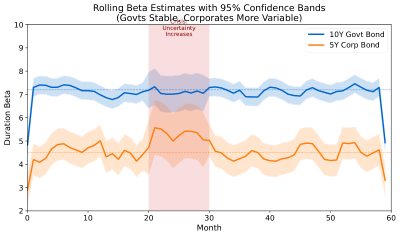

02e. Beta Stability Bands

Factor loading stability over time

Calibration Methods

Two complementary approaches for estimating implied risk premia: market-based (M1) using yield curve data, and historical (M2) using weighted factor returns.

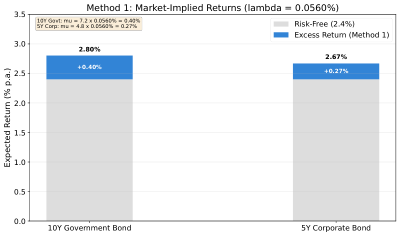

Method 1: Market-Based

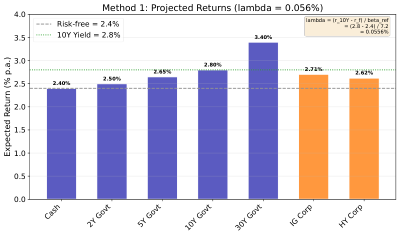

03. Method 1 Projection

Bond yield spread calibration

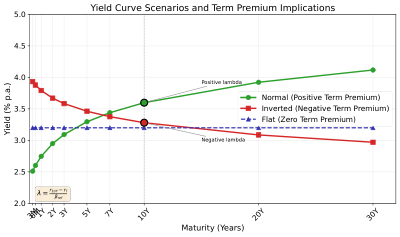

03b. Inverted Yield Curve

Special case handling

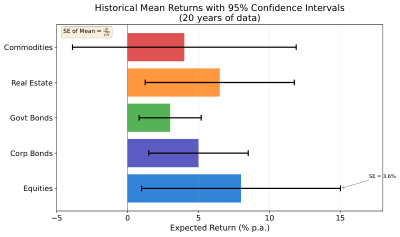

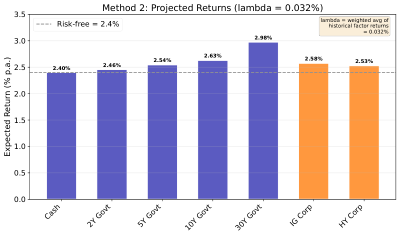

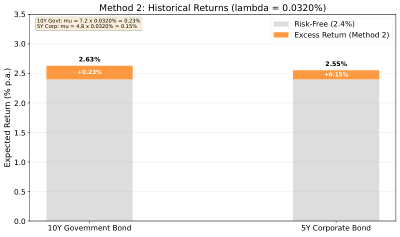

Method 2: Historical

Regime Detection

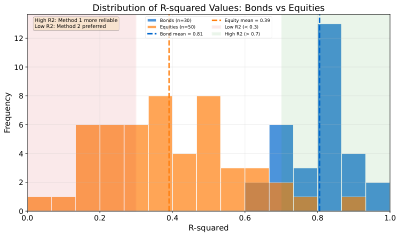

05. R-Squared Distribution

Historical R-squared values

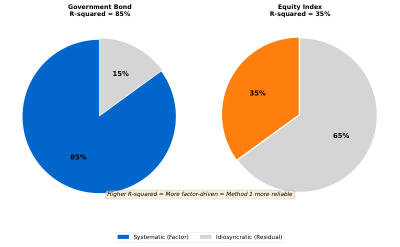

05b. Bond vs Equity R-Squared

Asset class comparison

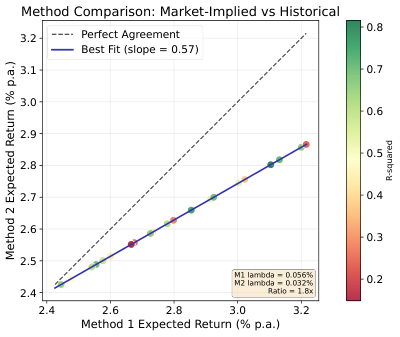

Method Comparison

06. Method Comparison Scatter

M1 vs M2 implied returns

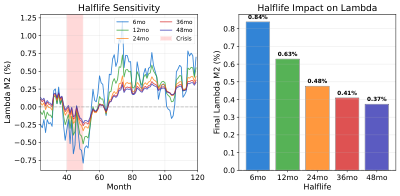

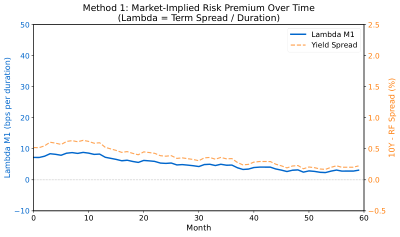

06b. Lambda M1 Time Series

Market-based lambda over time

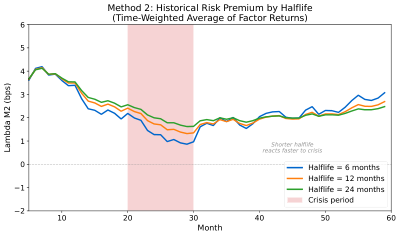

06c. Lambda M2 Time Series

Historical lambda over time

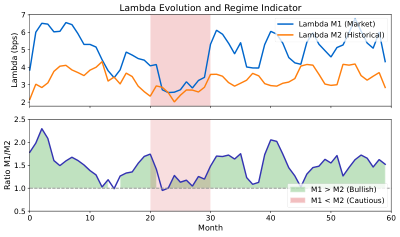

06d. Lambda Ratio Regime

M1/M2 ratio as regime indicator

Results & Validation

07. Method 1 Results

M1 implied returns output

07b. Method 2 Results

M2 implied returns output

07c. Final Comparison

Side-by-side method results

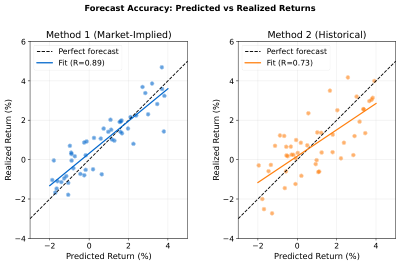

07d. Predicted vs Realized

Forecast accuracy scatter

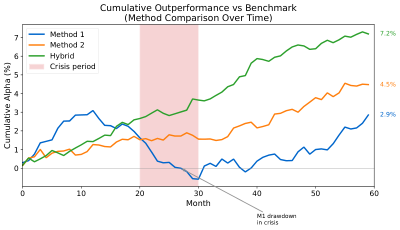

07e. Cumulative Outperformance

Strategy performance over time

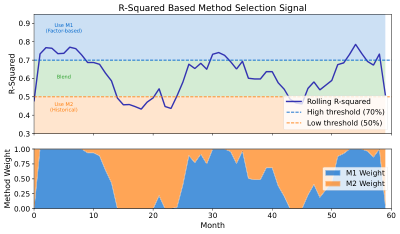

07f. Regime Switch Signals

M1/M2 switch timing