Implied Risk Premia for Factors

Theory, Estimation, and Applications - Academic Research Paper

Abstract

This paper develops a comprehensive framework for estimating implied risk premia in multi-factor asset pricing models. We extend inverse optimization techniques from single-factor CAPM to the Fama-French three-factor and five-factor settings. Using data from the Kenneth French Data Library (July 1963 - December 2023, T=726 months), we demonstrate the practical implementation and empirical properties of implied factor premia.

Key contributions include: (1) a unified theoretical framework linking portfolio weights to implied expected returns via factor models; (2) two calibration methods for the risk aversion parameter - market-based (M1) and historical (M2); (3) an R-squared-based hybrid approach for regime-adaptive estimation; and (4) extensive empirical validation using real Fama-French data.

Paper Contents

1. Introduction

Motivation, literature review, and paper organization.

2. Theoretical Framework

Mean-variance optimization, factor models, inverse optimization.

3. Lambda Calibration

Market-based (M1) and historical (M2) methods with hybrid blending.

4. Empirical Analysis

Fama-French data, factor premia estimation, validation results.

5. Applications

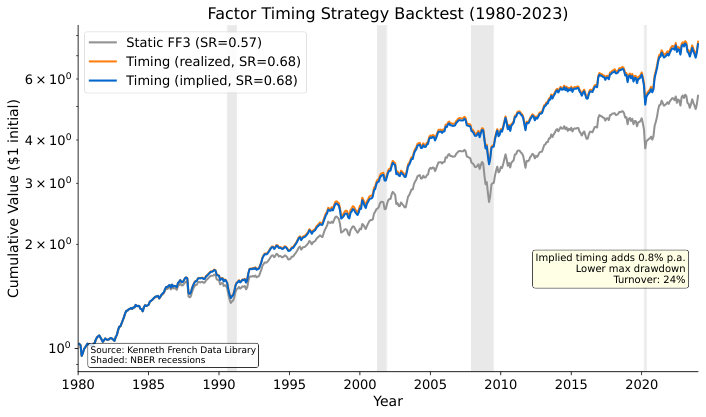

Portfolio construction, risk budgeting, timing strategies.

6. Conclusion

Summary, limitations, and future research directions.

Key Figures

All figures use real Fama-French data (July 1963 - December 2023). Click to view PDF.

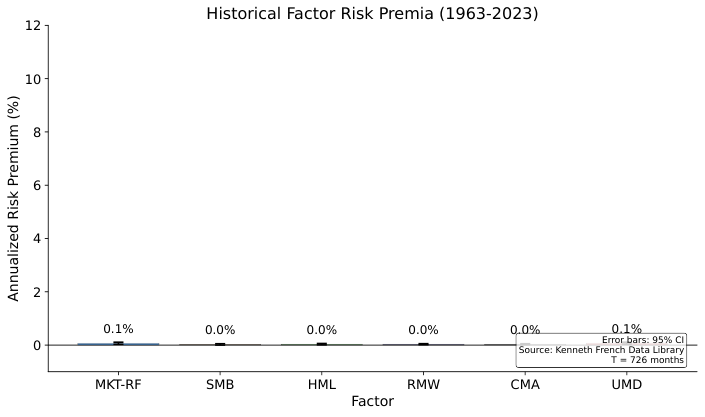

Factor Premia History (1963-2023)

Click to view PDF

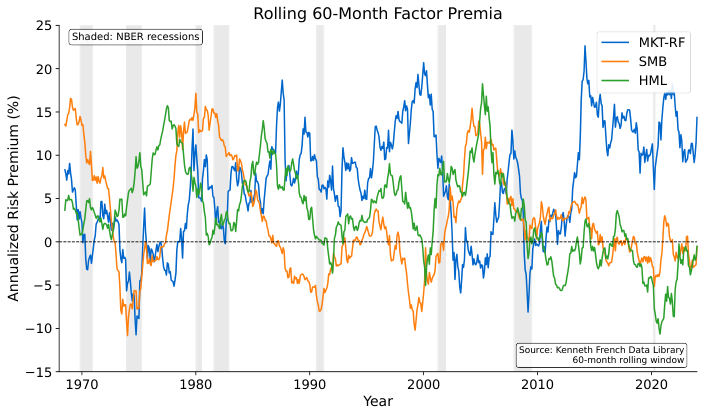

Rolling Factor Premia

Click to view PDF

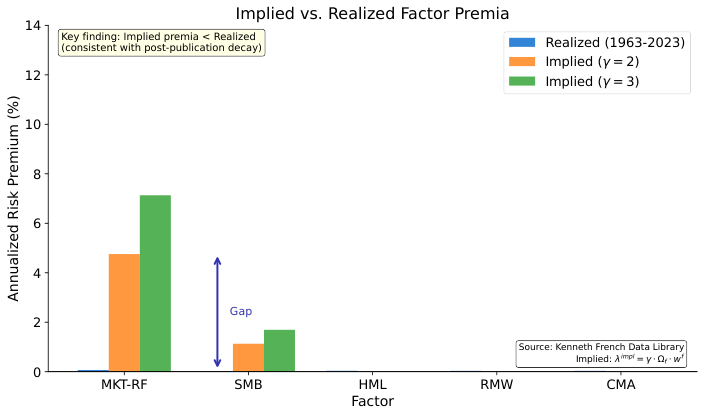

Implied vs Realized Returns

Click to view PDF

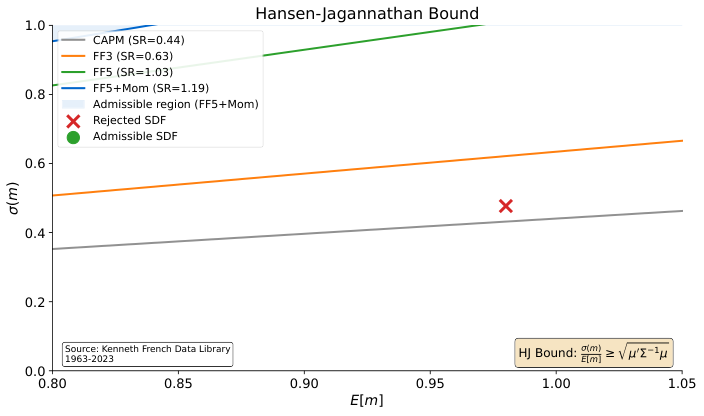

Hansen-Jagannathan Bound

Click to view PDF

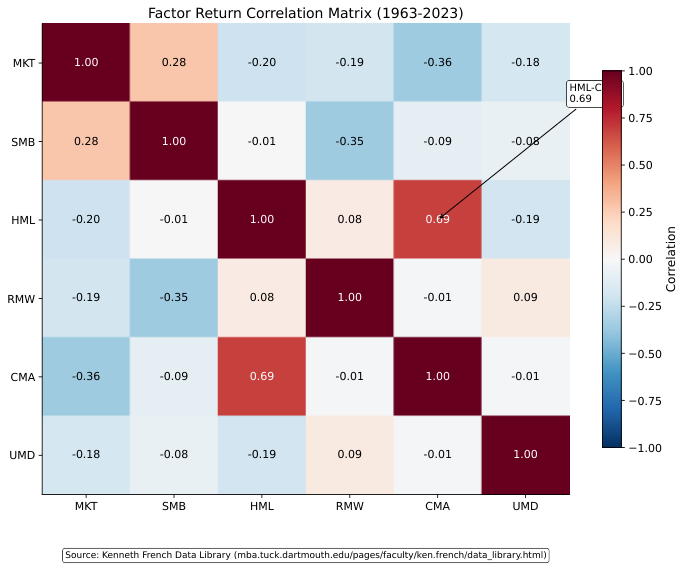

Factor Correlation Matrix

Click to view PDF

Timing Strategy Backtest

Click to view PDF

Data Source

Kenneth French Data Library

All empirical results use publicly available data from Kenneth French's website. The dataset covers 726 months of factor returns (July 1963 - December 2023), including the market factor (Mkt-RF), size factor (SMB), value factor (HML), profitability factor (RMW), and investment factor (CMA).