Discussion

1. Discussion

1.1 The Implicit Contract in Action

The evidence synthesized in Section consistently supports the implicit contract framework developed in Section . Style drift is tolerated because it represents an efficient arrangement: managers receive flexibility to pursue alpha; investors receive the option value of skilled active management; reputational markets and investor flows provide enforcement without formal legal mechanisms. This section discusses how the implicit contract manifests in practice, its implications for regulation, and remaining controversies.

1.2 Main Insights

Three overarching insights emerge from this systematic review of 71 high-quality studies spanning three decades of mutual fund style drift research. Each insight aligns with predictions from the implicit contract framework.

1. Measurement matters, but no perfect metric exists. Return-based style analysis (RBSA) pioneered by William F. Sharpe (1992) remains computationally accessible and applicable to funds with limited holdings disclosure. However, RBSA provides coarse-grained style estimates that may miss short-term tactical shifts. Holdings-based style analysis (HBSA) offers precise, point-in-time style measurement but requires comprehensive portfolio data and is computationally intensive for large fund universes. Active Share, introduced by Martijn Cremers & Antti Petajisto (2009), captures deviation from benchmarks effectively but requires ex ante benchmark assignment and has been criticized for sensitivity to benchmark choice (Martijn Cremers & Antti Petajisto (2013)). Practitioners and researchers should triangulate across multiple metrics, using RBSA for broad screening, HBSA for detailed analysis, and Active Share for benchmark-relative assessment. 2. The drift-performance relationship is conditional, not universal. The central controversy in this literature—whether style drift represents skilled alpha-seeking or agency-driven misconduct—finds resolution in conditional analysis. Performance outcomes depend critically on three factors:- Intentionality: Deliberate style shifts to exploit cross-asset mispricing generate positive alpha, while passive drift driven by fund flows or managerial inattention destroys value.

- Direction: Drift toward small-cap and value styles—where mispricing is more prevalent due to lower analyst coverage and higher information asymmetry—tends to be value-additive. Drift toward benchmarks (closet indexing) or toward large-cap growth consistently underperforms.

- Manager skill: High-active-share managers with demonstrated stock-picking ability benefit from style flexibility; low-skill managers amplify losses when drifting from their stated mandates.

These conditional findings help resolve the apparent contradictions in the literature. Studies finding positive drift-performance relationships typically examine skilled managers making deliberate tactical shifts (Russ Wermers (2000)). In contrast, studies finding negative relationships typically examine closet indexing or agency-driven behavior (Berk A. Sensoy (2009)). The key insight is that context determines outcomes.

3. Disclosure alone is insufficient. Regulatory interventions over the past two decades have substantially increased transparency around fund styles and holdings. The SEC’s N-Q and N-PORT filing requirements, enhanced prospectus disclosure, and the proliferation of third-party style classification systems (Morningstar, Lipper) have reduced information asymmetry. However, the evidence suggests that disclosure has not meaningfully reduced drift frequency. This apparent puzzle has several explanations: (i) investors face high search costs in processing complex holdings data; (ii) performance-chasing behavior dominates style-consistency concerns; (iii) sophisticated investors who could monitor drift are precisely those who already avoid drifting funds. More effective regulatory interventions might include mandatory prospectus constraints with enforcement penalties, performance-based fees tied to style consistency, and enhanced independent board oversight with explicit style monitoring responsibilities.1.3 Theoretical Implications

Our synthesis offers several theoretical contributions:

Agency theory refinement. The style drift literature demonstrates that agency conflicts in delegated portfolio management are more nuanced than simple principal-agent models suggest. Fund managers face multiple principals (fund company, distributors, investors) with potentially conflicting preferences regarding style consistency versus performance maximization. This “multi-principal” framing explains why governance mechanisms (board independence, 12b-1 fees, manager ownership) have inconsistent effects on drift. Signaling under incomplete contracts. Style consistency may serve as a credible signal of managerial discipline in settings where contracts cannot fully specify investment mandates. Managers who maintain style consistency credibly commit to not exploiting discretion opportunistically, attracting investors who value predictability. This signaling equilibrium is fragile, however, because some style drift is observationally equivalent to skill-based timing. Behavioral finance integration. The literature documents systematic behavioral patterns among both managers and investors. Managers exhibit disposition effects, overconfidence, and career concerns that drive drift; investors exhibit inertia, limited attention, and category-based thinking that mutes market discipline. These behavioral frictions create persistent pricing anomalies that rational arbitrage cannot fully eliminate.1.4 Practical Implications

Our findings have direct implications for multiple stakeholder groups:

For fund investors: Monitor Active Share and style consistency over rolling windows, not just point-in-time snapshots. Prefer funds with explicit style mandates in prospectuses, independent boards with demonstrated oversight capacity, and managers with meaningful personal investment in the fund. Be skeptical of funds that drift toward performance-chasing factor tilts. For fund managers: Recognize that style drift is increasingly monitorable and may trigger investor redemptions. If pursuing tactical style shifts, document the investment thesis and communicate to shareholders. Maintain sufficient cash buffers to avoid forced selling that causes unintended drift. For regulators: Consider moving beyond disclosure-only interventions toward substantive constraints on style deviation. Require explicit benchmark designation in prospectuses with penalties for persistent deviations. Mandate that fund boards include members with quantitative skills capable of monitoring style analytics. For researchers: Develop integrated drift metrics that combine RBSA, HBSA, and Active Share. Extend analysis to non-U.S. markets, ESG contexts, and algorithmic investment strategies. Investigate the causal mechanisms linking drift to performance using quasi-experimental designs.1.5 Regulatory Design Principles from the Implicit Contract

The implicit contract framework generates specific regulatory design principles that go beyond the general recommendations above.

Principle 1: Preserve beneficial optionality. Regulations should not prohibit style drift wholesale. Complete prohibition would destroy the option value of managerial flexibility, harming investors who benefit from skilled managers’ ability to exploit cross-style mispricing. The implicit contract predicts that rigid mandates would reduce aggregate investor welfare. Principle 2: Target contract failures, not drift per se. Policy interventions should focus on the specific failure modes identified in Section : tournament-driven risk-shifting, closet indexing, and exploitation of weak monitoring. These failures violate the implicit contract; value-creating drift does not. Targeted interventions might include: (i) penalties for extreme mid-year to year-end volatility increases; (ii) fee rebates when Active Share falls below thresholds; (iii) mandatory manager co-investment to align incentives. Principle 3: Strengthen market discipline mechanisms. The implicit contract relies on reputational enforcement through investor flows. Regulations should strengthen this mechanism by: (i) requiring salient, standardized style deviation disclosure at point-of-sale; (ii) mandating that advisors discuss style consistency with clients; (iii) enhancing board obligations to monitor and report on style adherence. Principle 4: Facilitate monitoring by sophisticated intermediaries. The implicit contract works best when sophisticated investors (institutions, consultants, rating agencies) monitor on behalf of less sophisticated investors. Regulations should reduce barriers to this monitoring by: (i) ensuring timely holdings disclosure to authorized data aggregators; (ii) standardizing style classification methodologies; (iii) requiring explicit benchmark designation that enables third-party Active Share calculation.These principles suggest that optimal regulation balances flexibility preservation against agency cost mitigation—exactly the trade-off embedded in the implicit contract. The evidence base remains insufficient to specify precise regulatory parameters, highlighting the importance of future research on regulatory effectiveness (Section ).

1.6 Reconciling Conflicting Findings

A distinctive feature of the style drift literature is the prevalence of apparently contradictory findings. Our systematic review allows us to reconcile these conflicts through careful attention to methodological differences, sample characteristics, and conditional effects.

Drift-performance contradictions resolved. Early studies found that style-consistent funds outperformed drifters, leading to the conclusion that drift reflects agency problems. Later studies found the opposite—drifters outperformed—suggesting skill. Our synthesis reveals that both findings are correct under different conditions. Studies examining broad cross-sections dominated by closet indexers find negative drift-performance relationships. Studies examining high-Active-Share funds with demonstrated stock-picking ability find positive relationships. The key moderator is manager skill: drift amplifies underlying ability (positive or negative). Active Share controversy resolved. The initial Martijn Cremers & Antti Petajisto (2009) finding that high Active Share predicts outperformance was challenged by subsequent studies showing sensitivity to benchmark choice and time period. Our synthesis suggests that Active Share predicts performance conditional on other skill indicators. High Active Share combined with industry concentration, patient capital, or manager education credentials predicts outperformance; high Active Share alone does not. Regulatory effectiveness contradictions resolved. Some studies find that disclosure requirements reduce drift; others find no effect. The resolution lies in distinguishing disclosure frequency from disclosure salience. Quarterly N-PORT filings provide data for sophisticated monitors but are not processed by retail investors. Salient warnings at point-of-sale may be more effective than detailed periodic filings.1.7 Limitations of This Review

This systematic review has several limitations that should inform interpretation:

Database coverage. We searched OpenAlex, which, while comprehensive, may miss working papers, dissertations, and practitioner publications not indexed in academic databases. The focus on English-language publications may exclude relevant research from non-English markets, particularly in Asia and Latin America where mutual fund industries have grown substantially. Quality thresholds. Our citation-based quality filter (minimum 10 citations, top 25\ Geographic concentration. The corpus is heavily weighted toward U.S.-domiciled funds (approximately 70\ Temporal scope. While we covered 1990–2025, the pre-2000 literature is sparse with only 5 papers. This sparsity limits our ability to assess how the economics of style drift have evolved. Market structure changes, technological innovation, and regulatory reform may have altered drift dynamics in ways our corpus cannot fully capture.1.8 Research Gaps

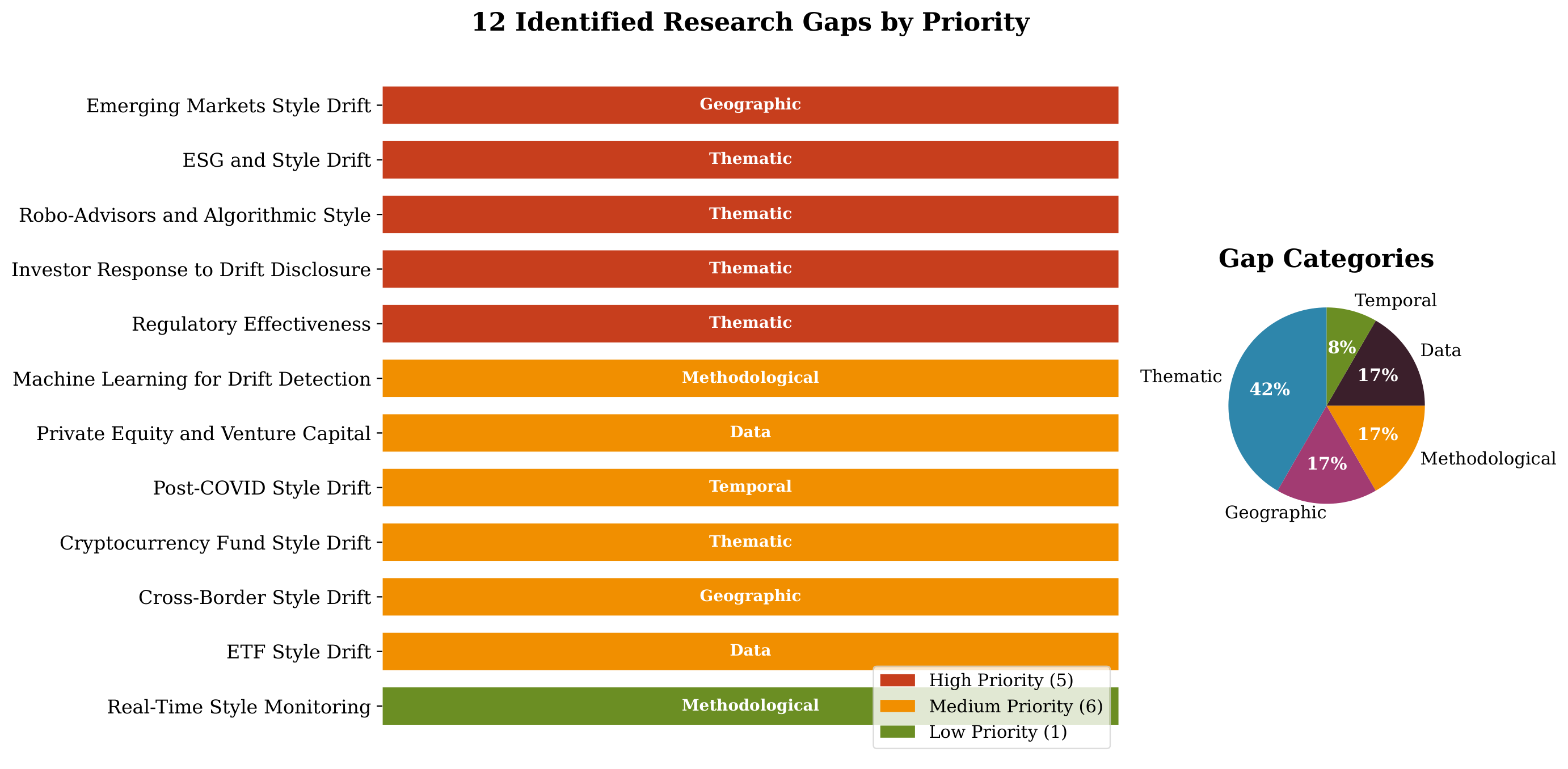

We identified twelve critical research gaps across five categories, summarized in Figure :

The five highest-priority gaps concern emerging market style drift, ESG greenwashing, robo-advisor consistency, investor behavioral response to disclosure, and regulatory effectiveness evaluation. First, emerging markets remain understudied due to regulatory heterogeneity and data limitations. Second, ESG greenwashing via style drift has grown increasingly salient given the \$35 trillion sustainable investment market. Third, robo-advisors and algorithmic style consistency merit examination as automated platforms proliferate. Fourth, research must test whether drift disclosure actually changes investor behavior. Fifth, empirical evaluation of regulatory effectiveness across jurisdictions remains incomplete.

These gaps represent significant opportunities for future research that could inform both academic understanding and policy design. We elaborate on each in Section .