NFT & DeFi Bubble Detection Research

Detecting price bubble formation using SADF, GSADF, and LPPLS frameworks

Detecting Price Bubble Formation in NFT and DeFi Markets

In ProgressLennart J. Baals [ORCID]

Based on: Wang et al. (2022), Journal of Chinese Economic and Business Studies

Digital asset markets, including those for non-fungible tokens (NFTs) and decentralized finance (DeFi) instruments, have expanded rapidly and are commonly viewed as highly speculative. This research examines the extent and timing of price bubbles in these markets using daily USD prices for two capitalization-weighted benchmarks (NFT Index and DeFi Pulse Index), alongside major infrastructure coins and DeFi-related tokens. We apply SADF and GSADF tests to detect and date-stamp mildly explosive episodes, with LPPLS framework as robustness check.

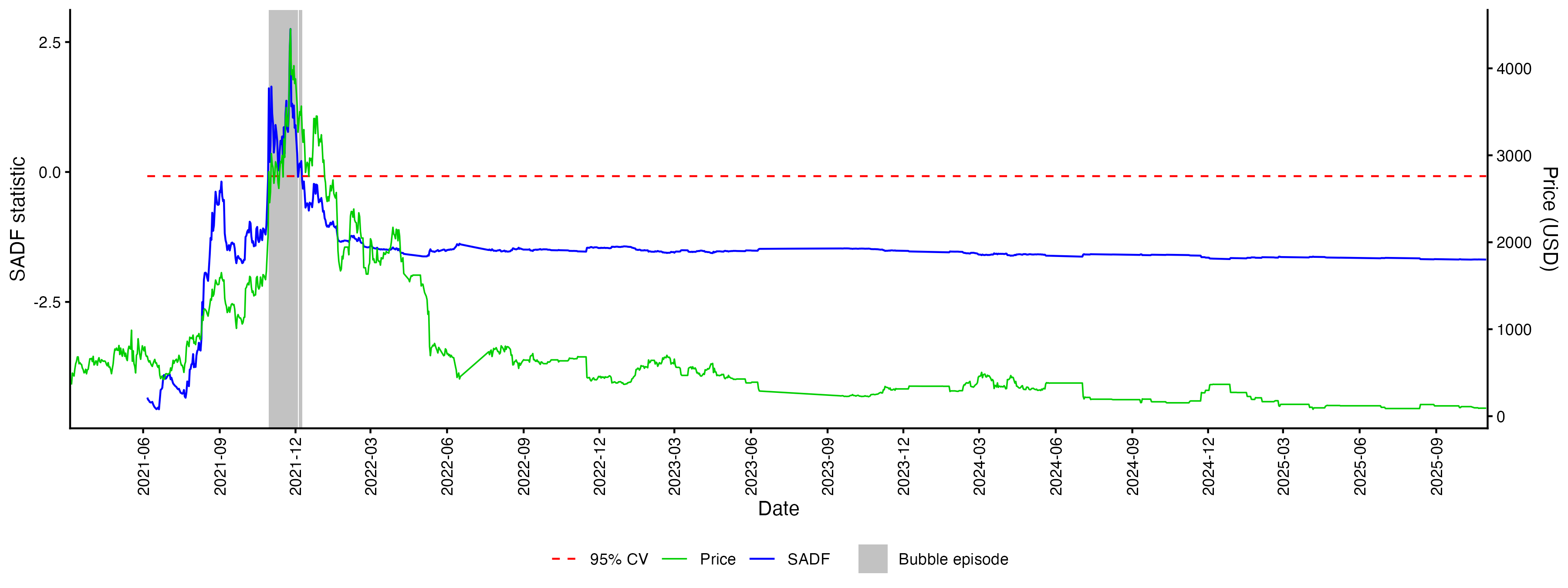

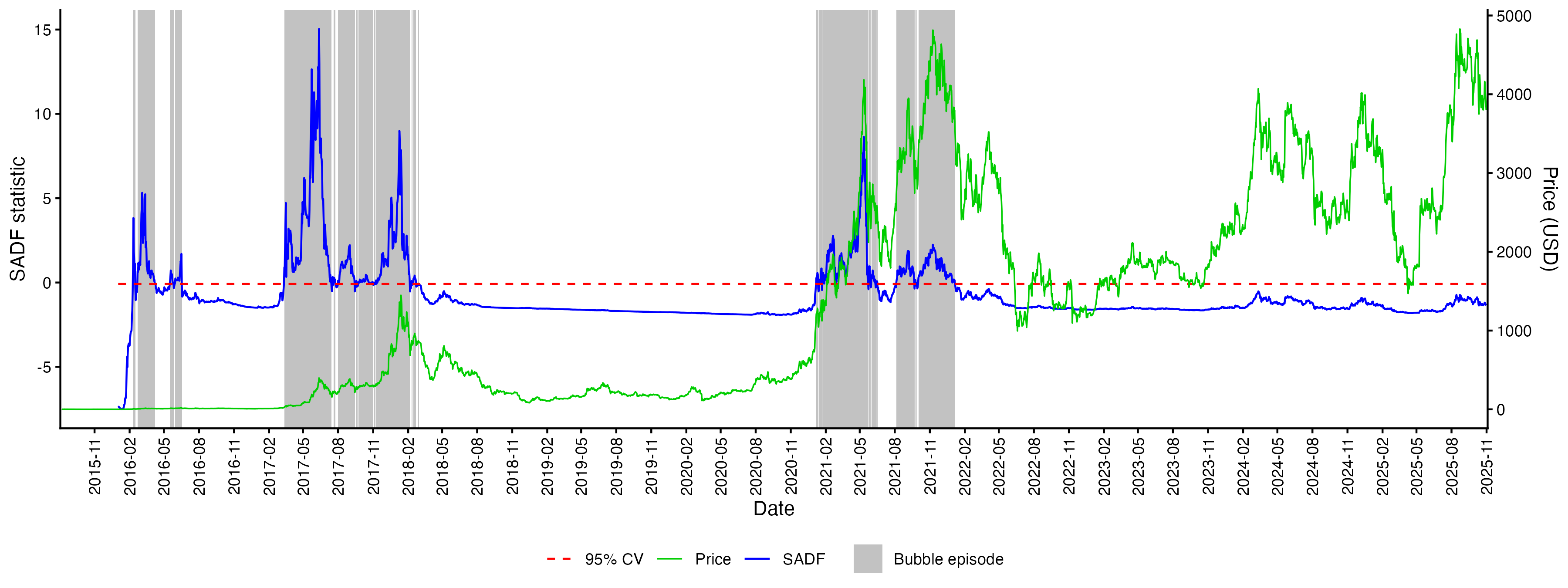

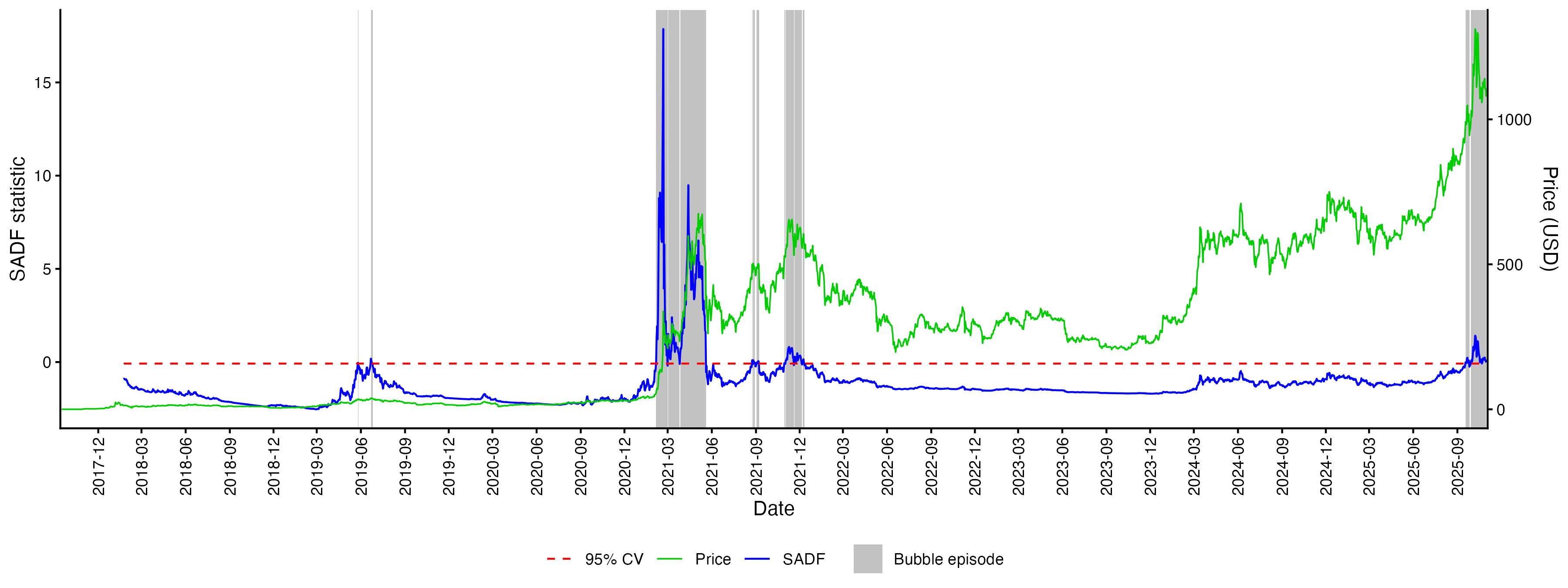

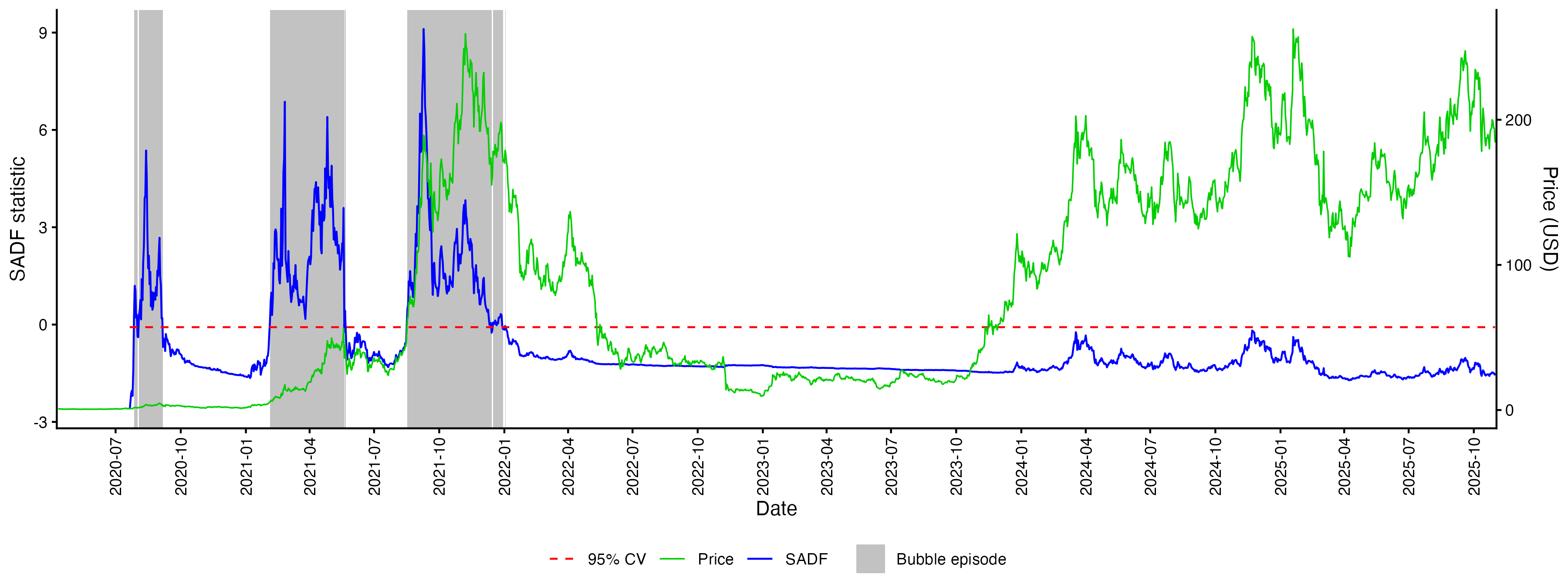

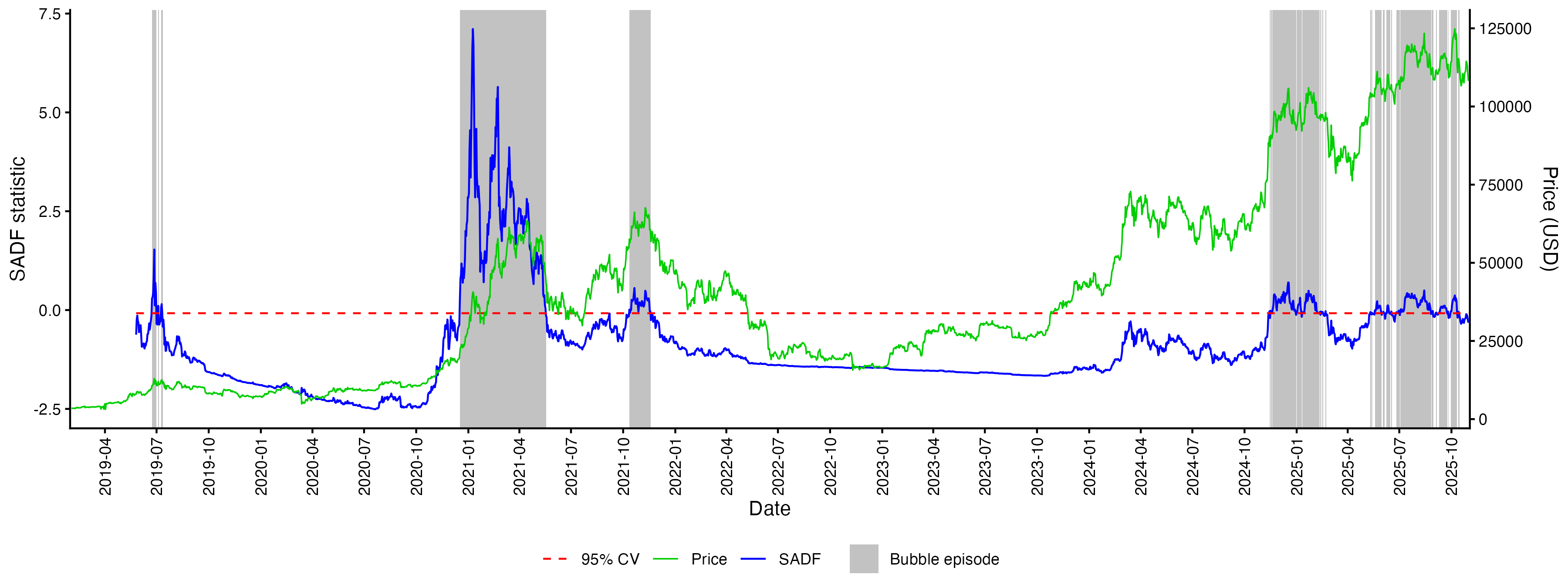

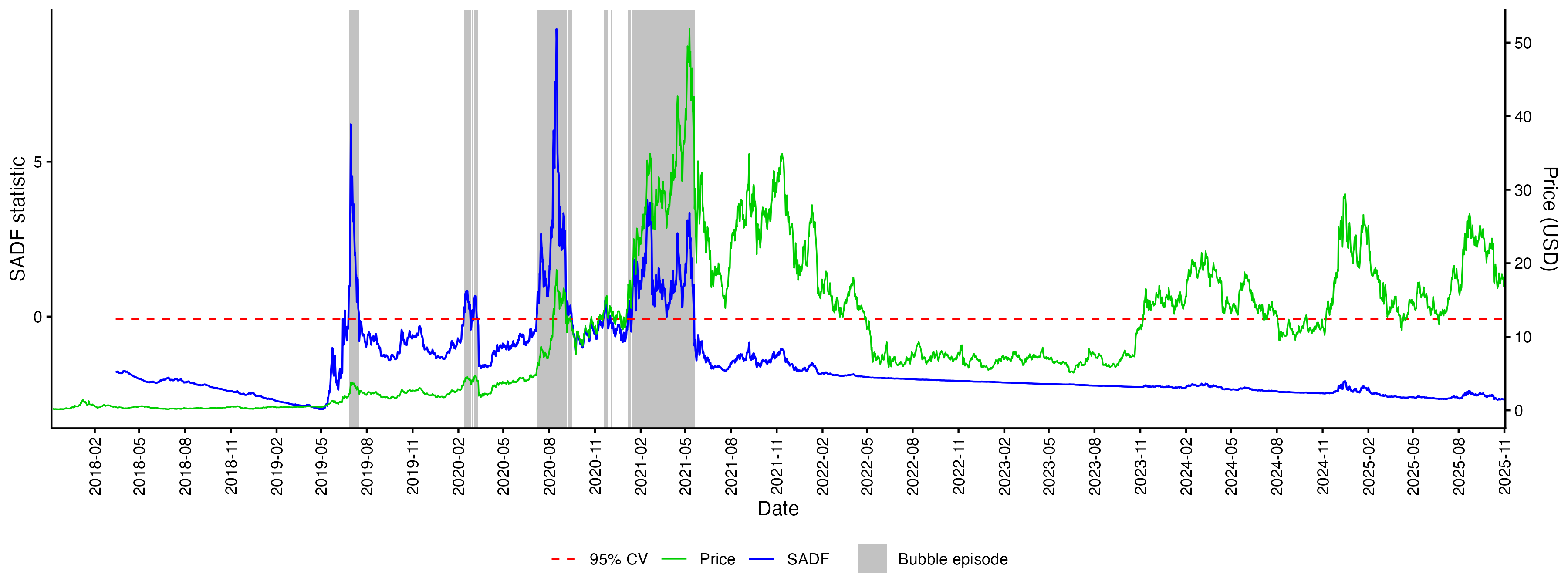

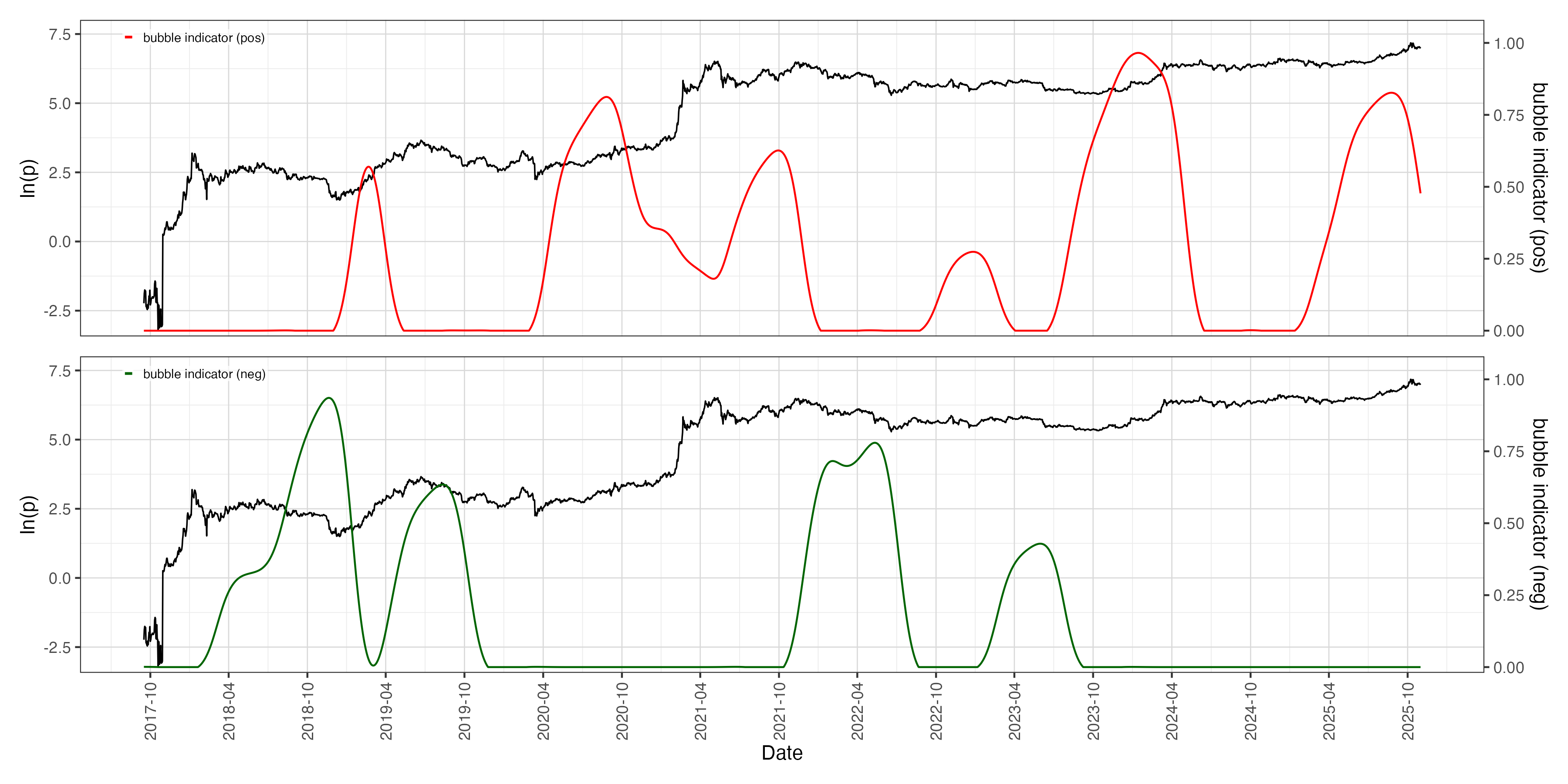

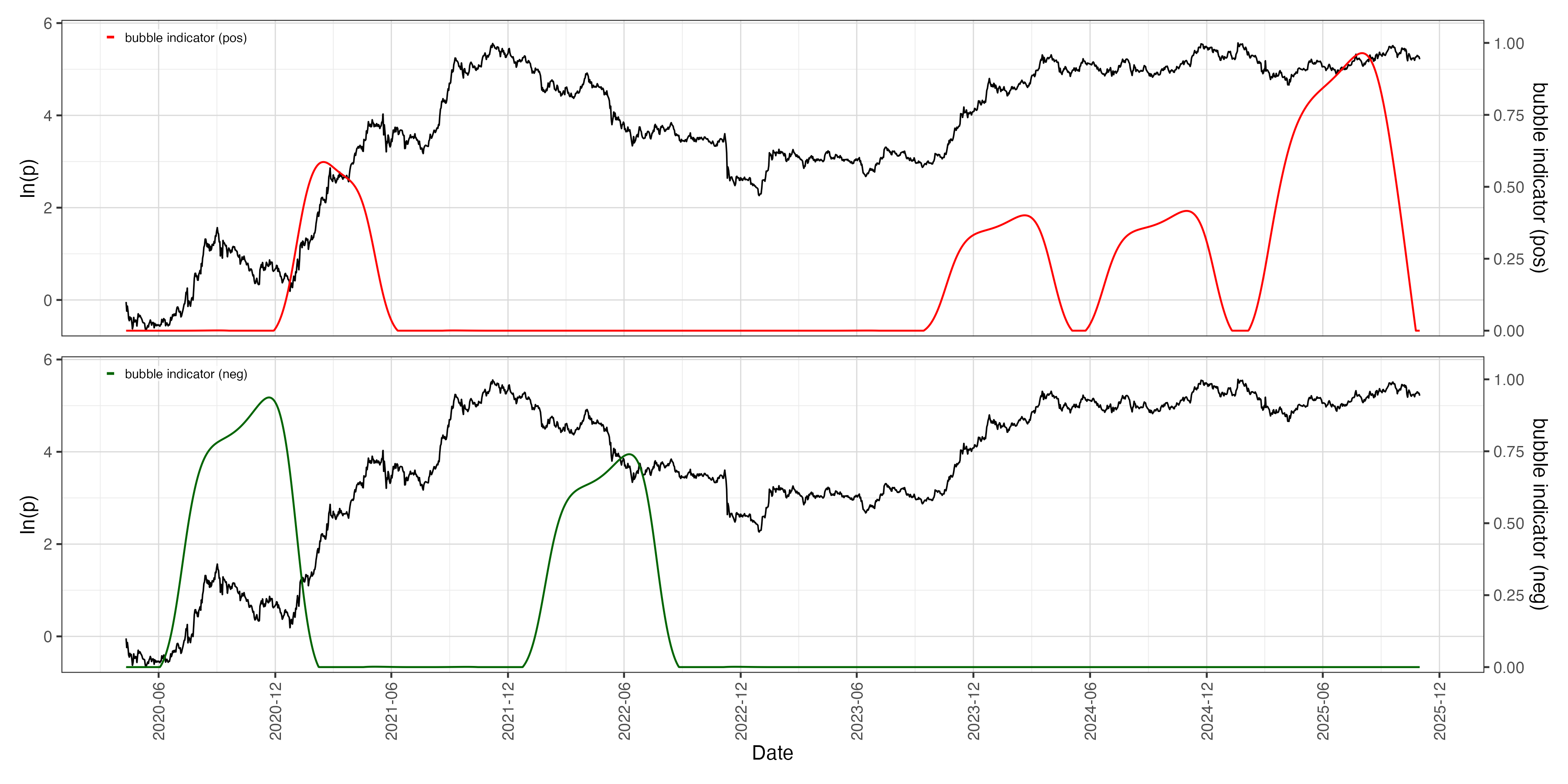

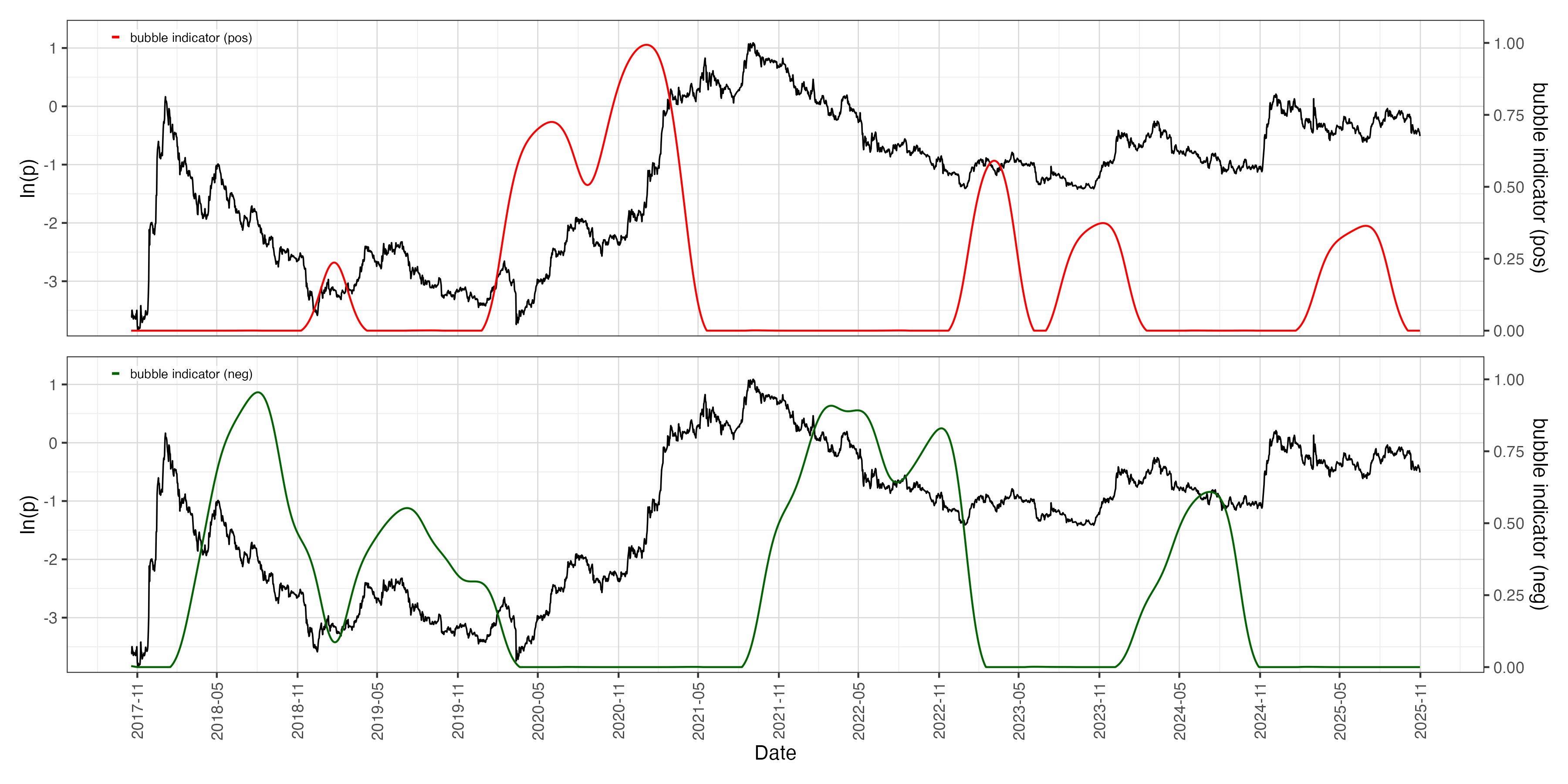

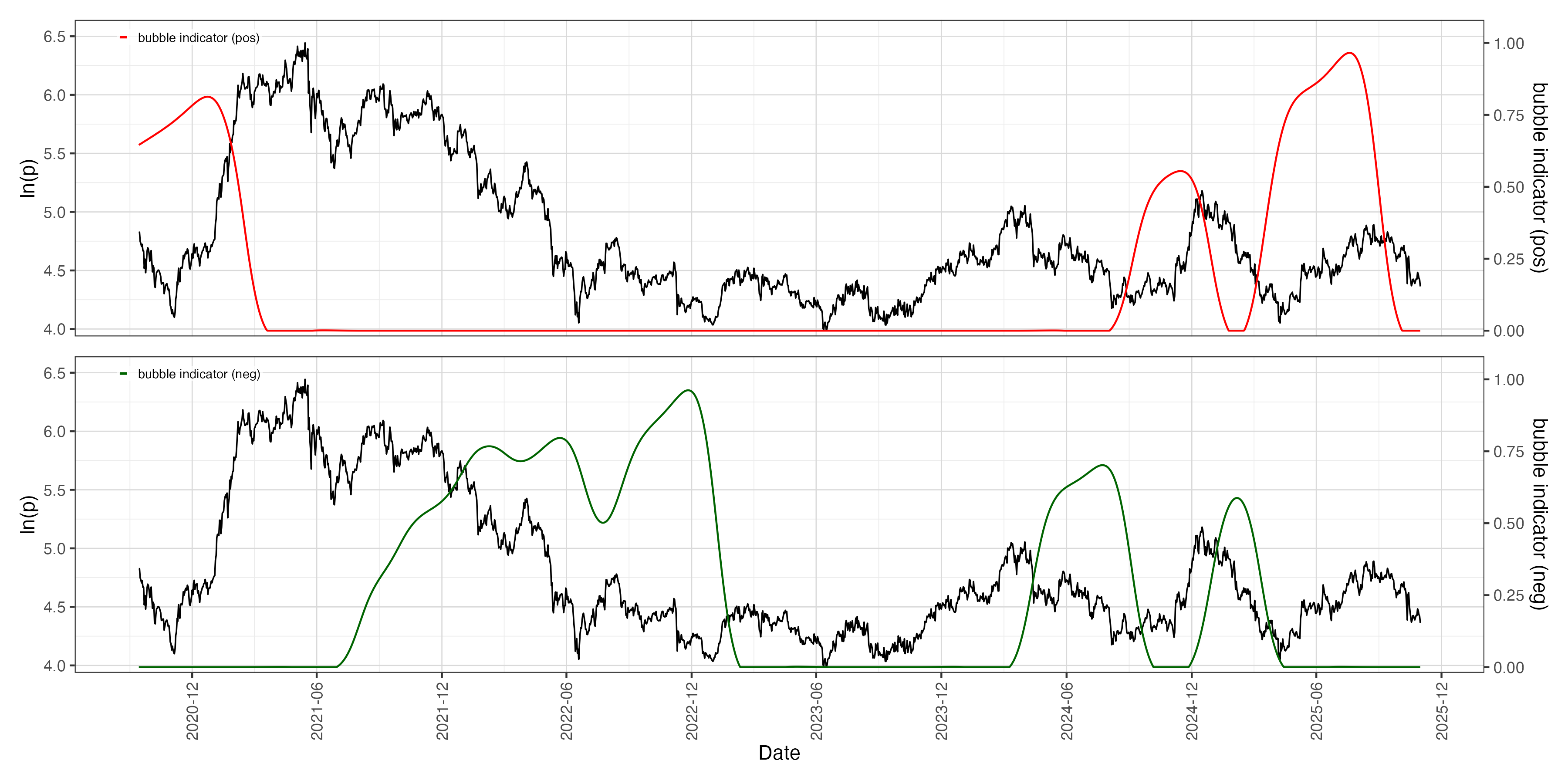

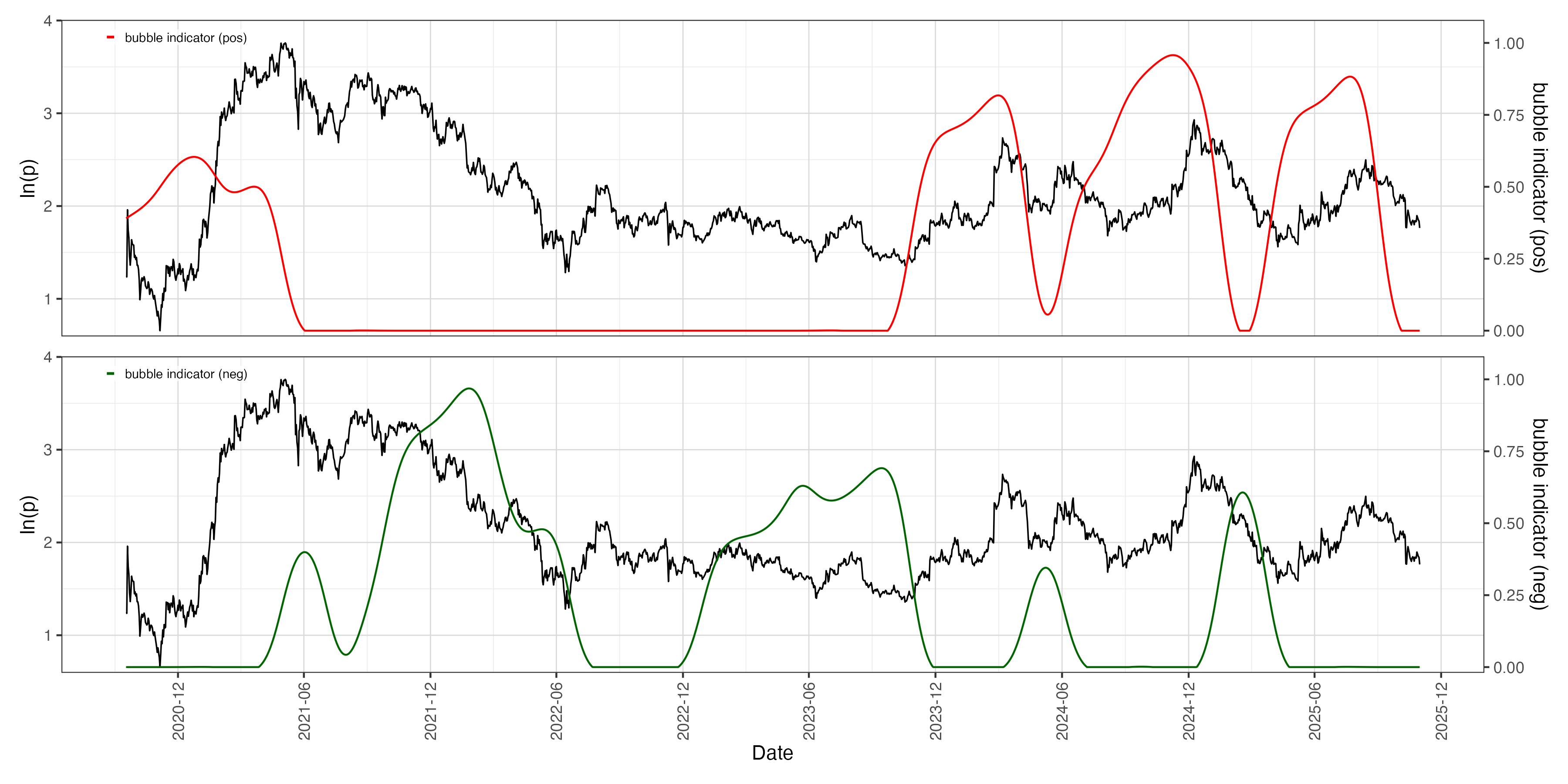

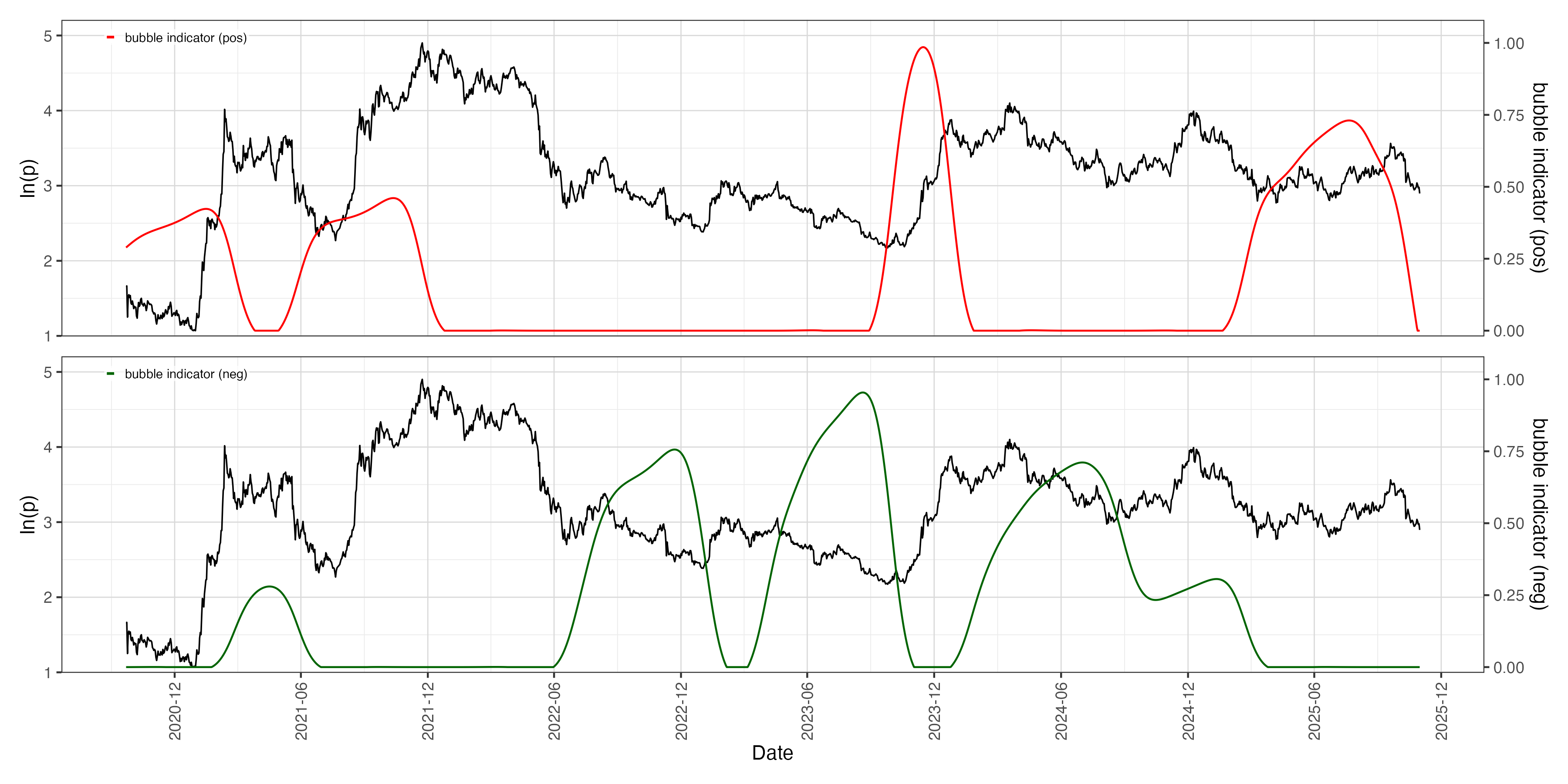

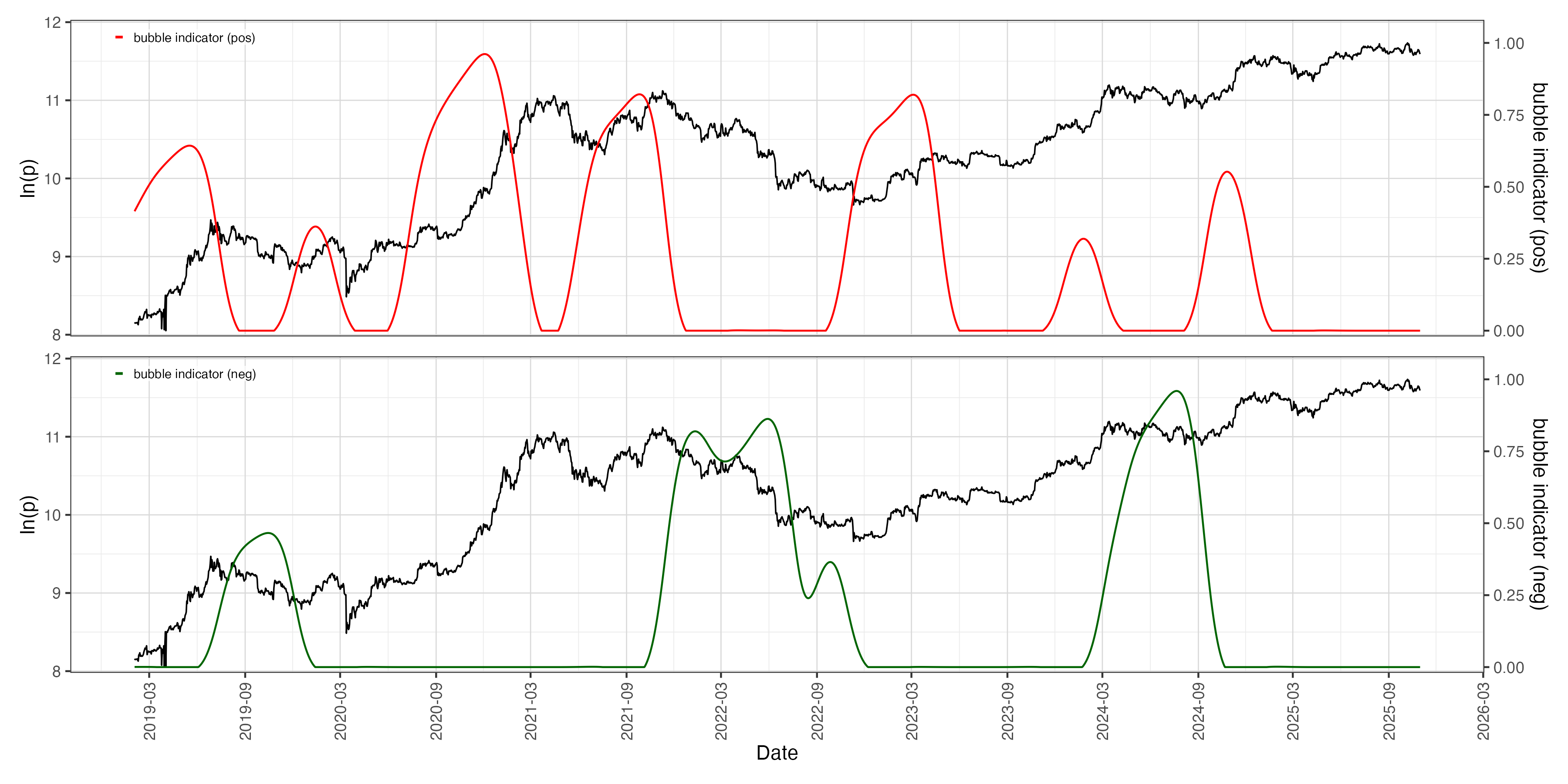

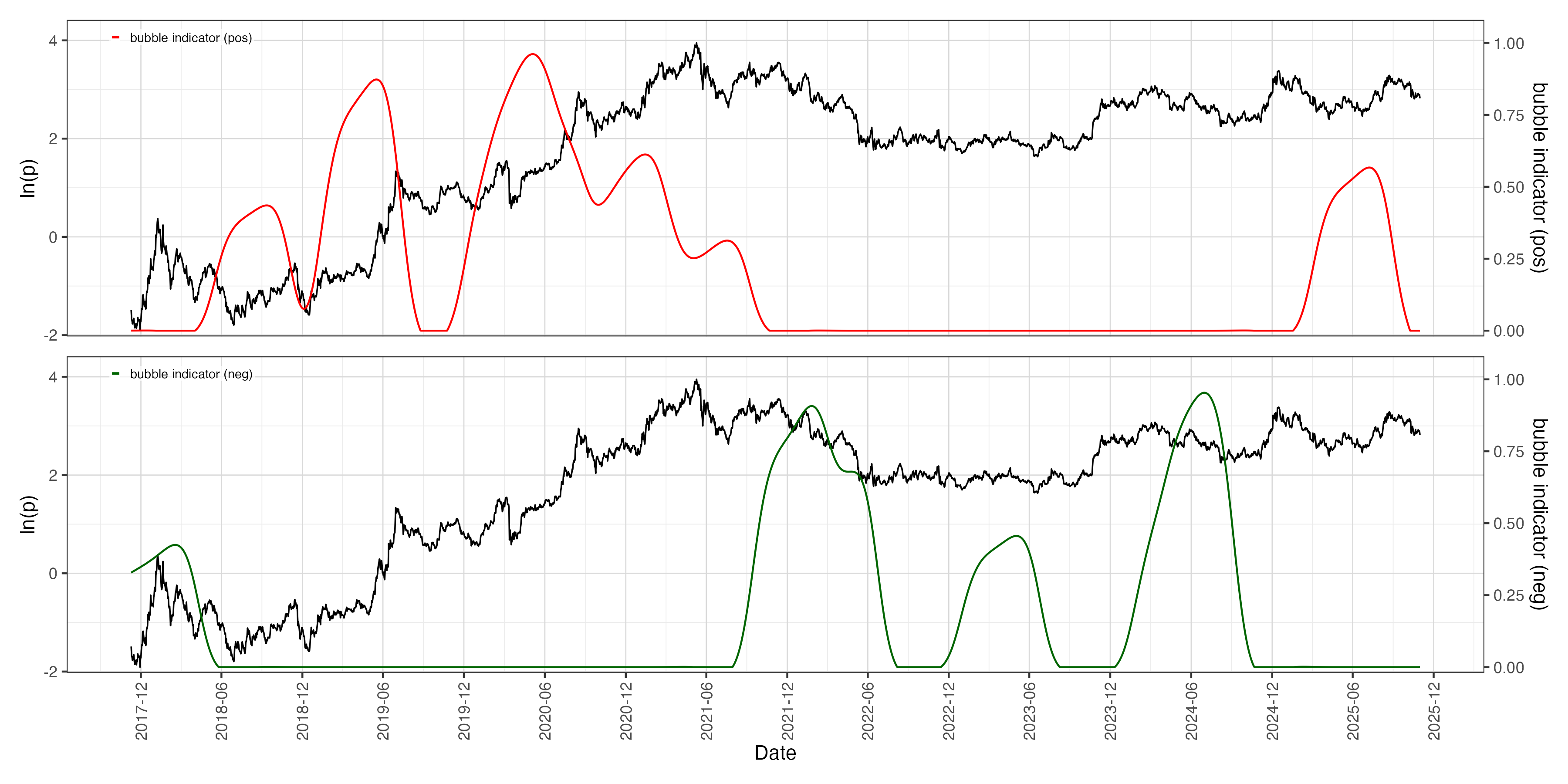

Recurrent Bubble Regimes

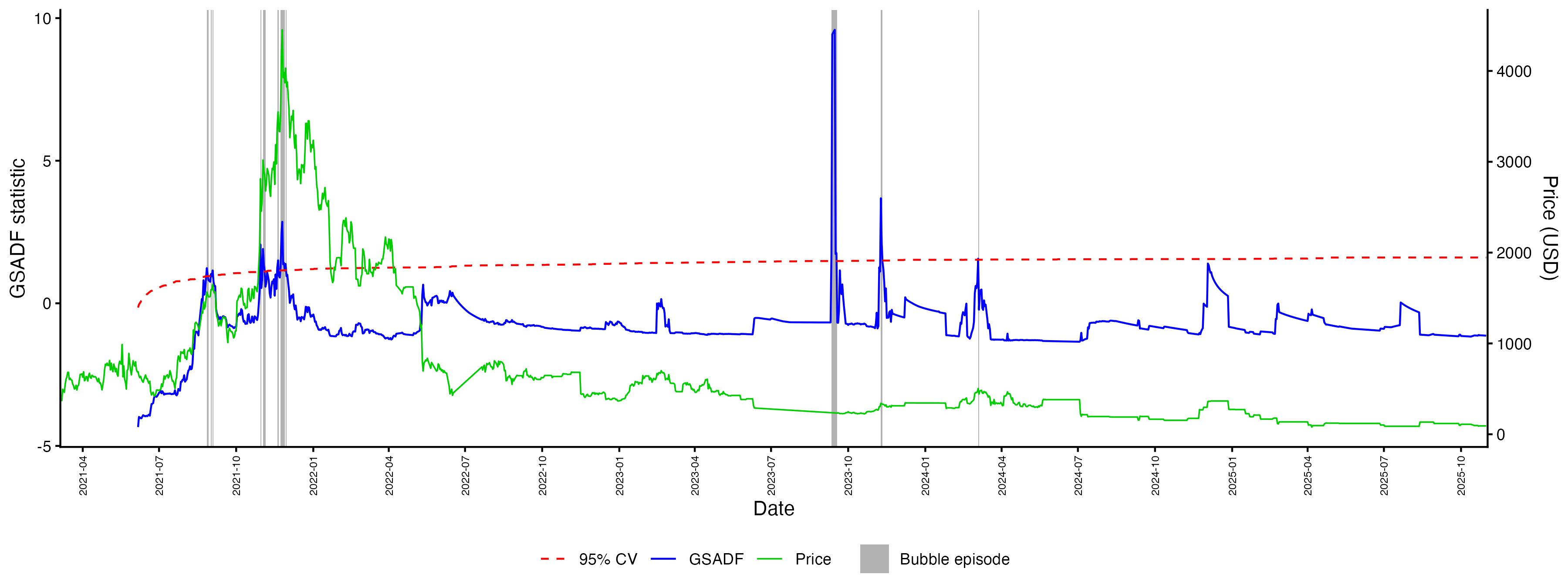

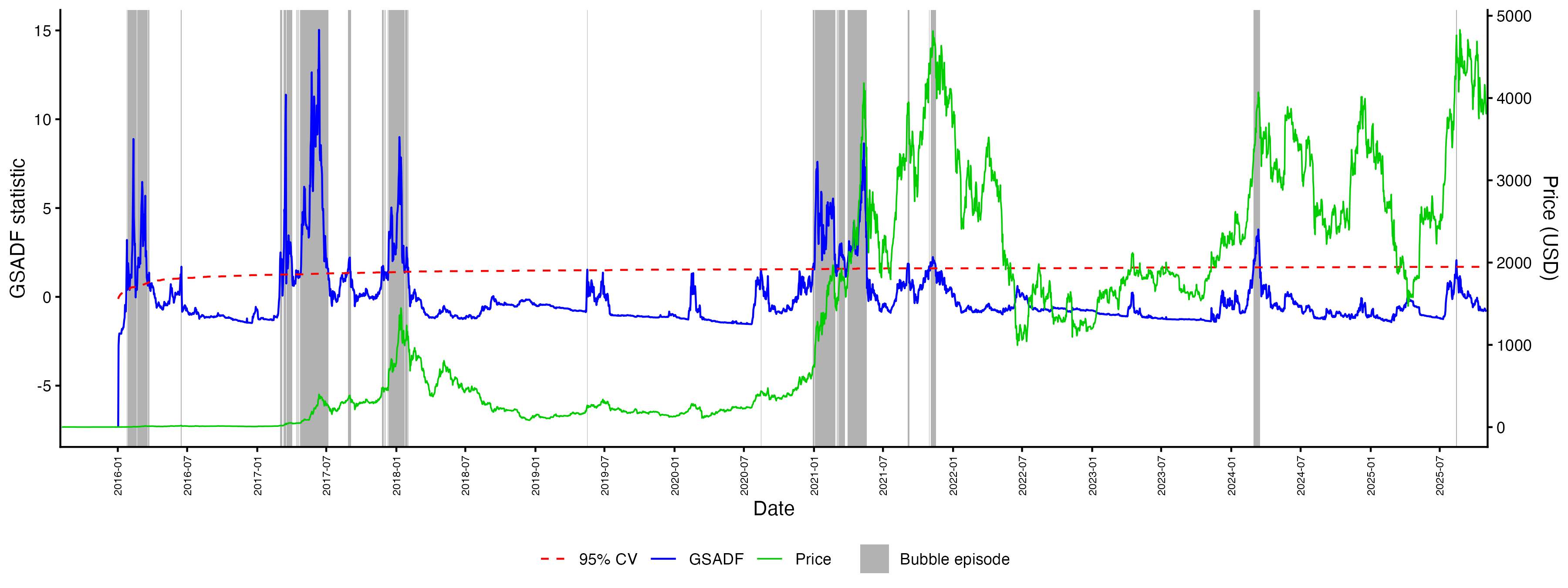

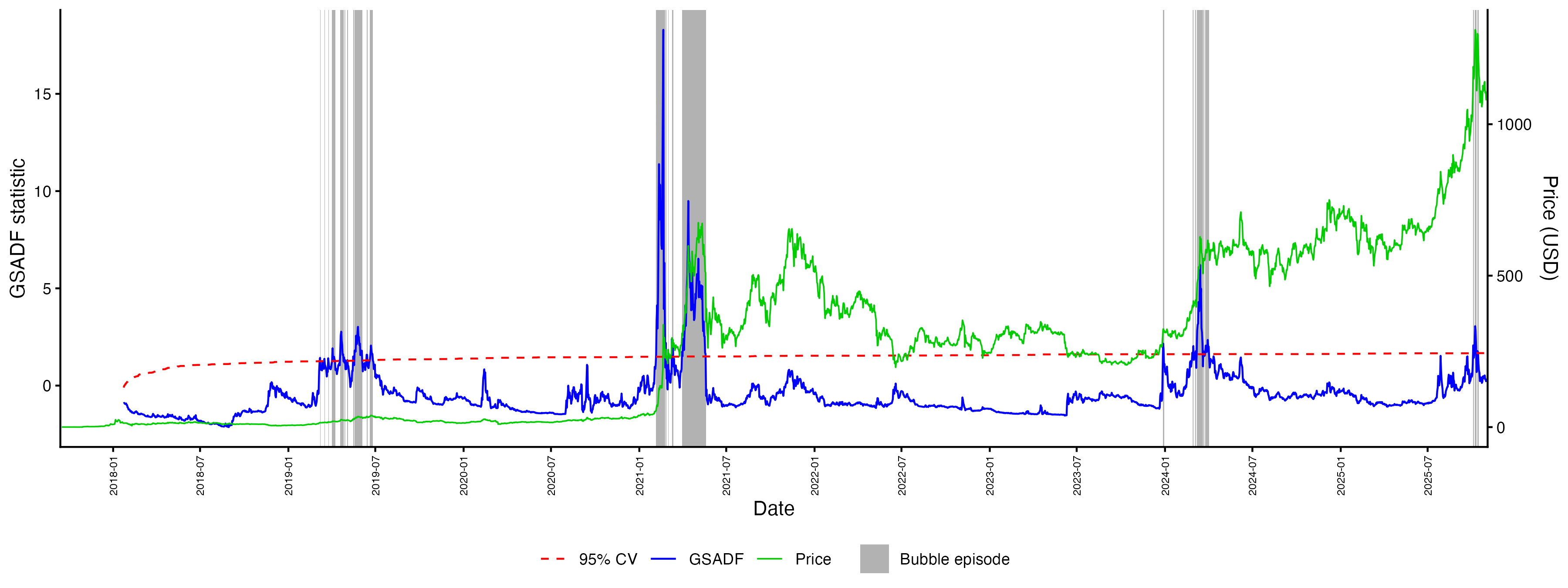

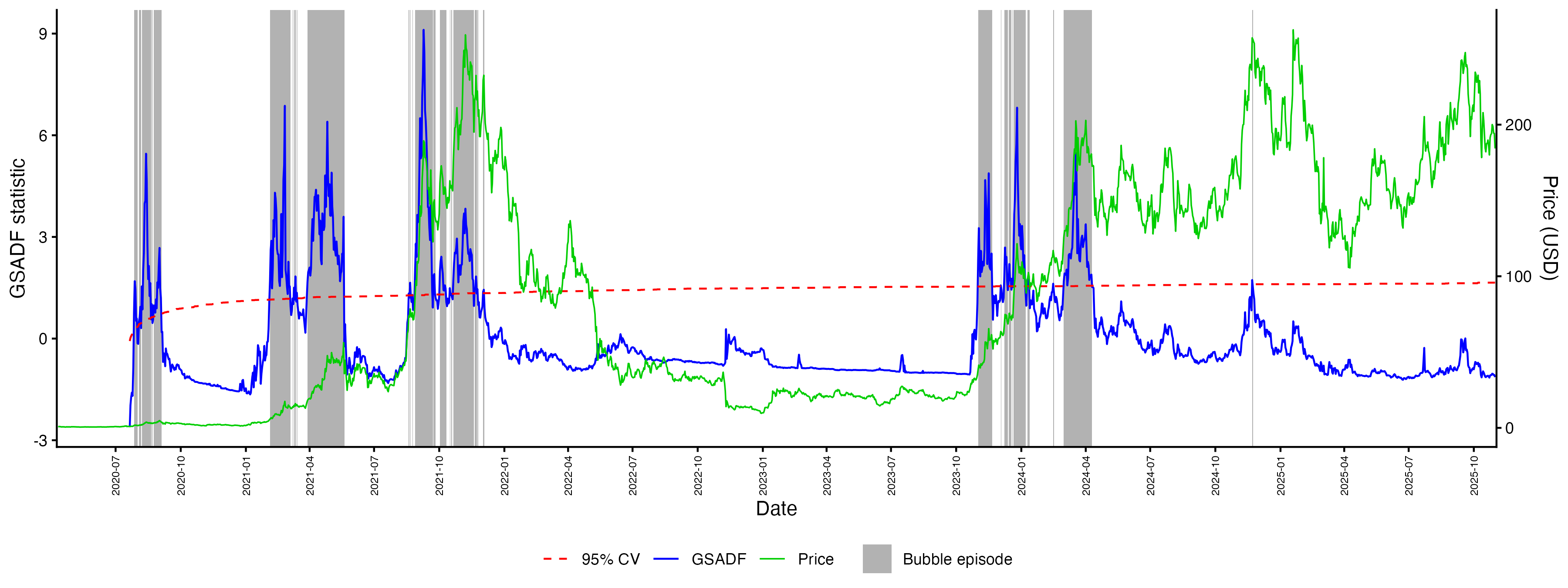

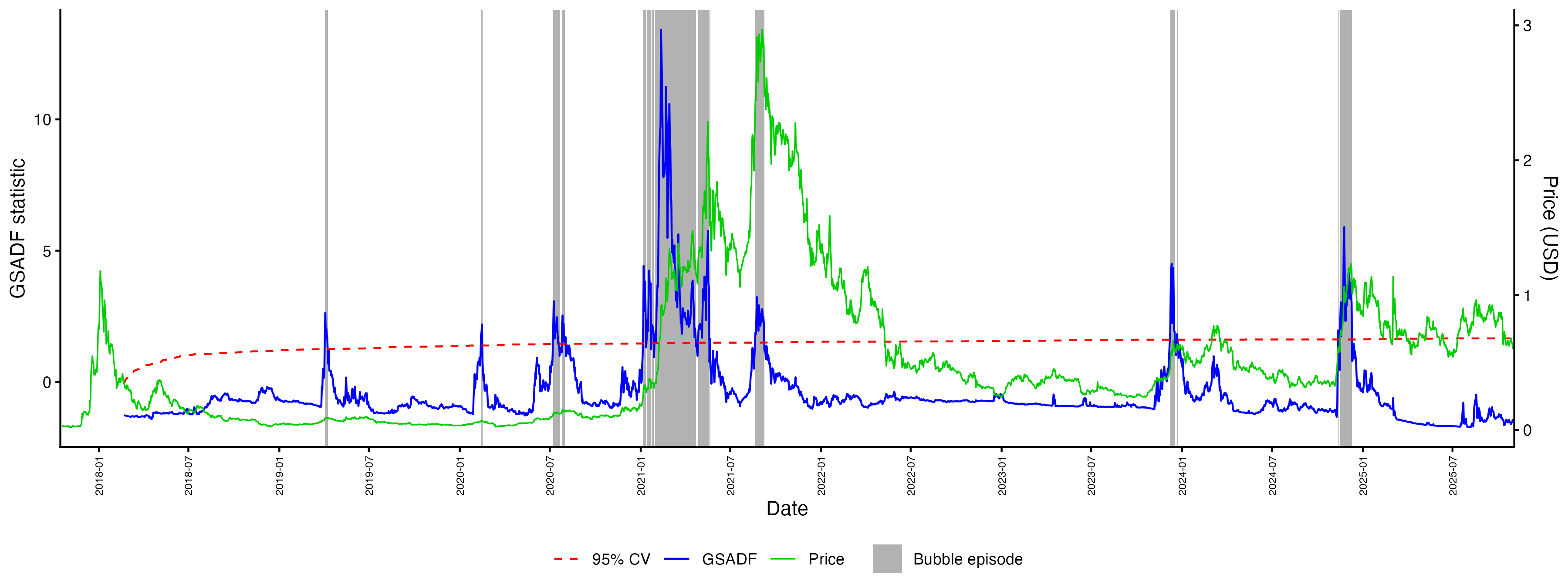

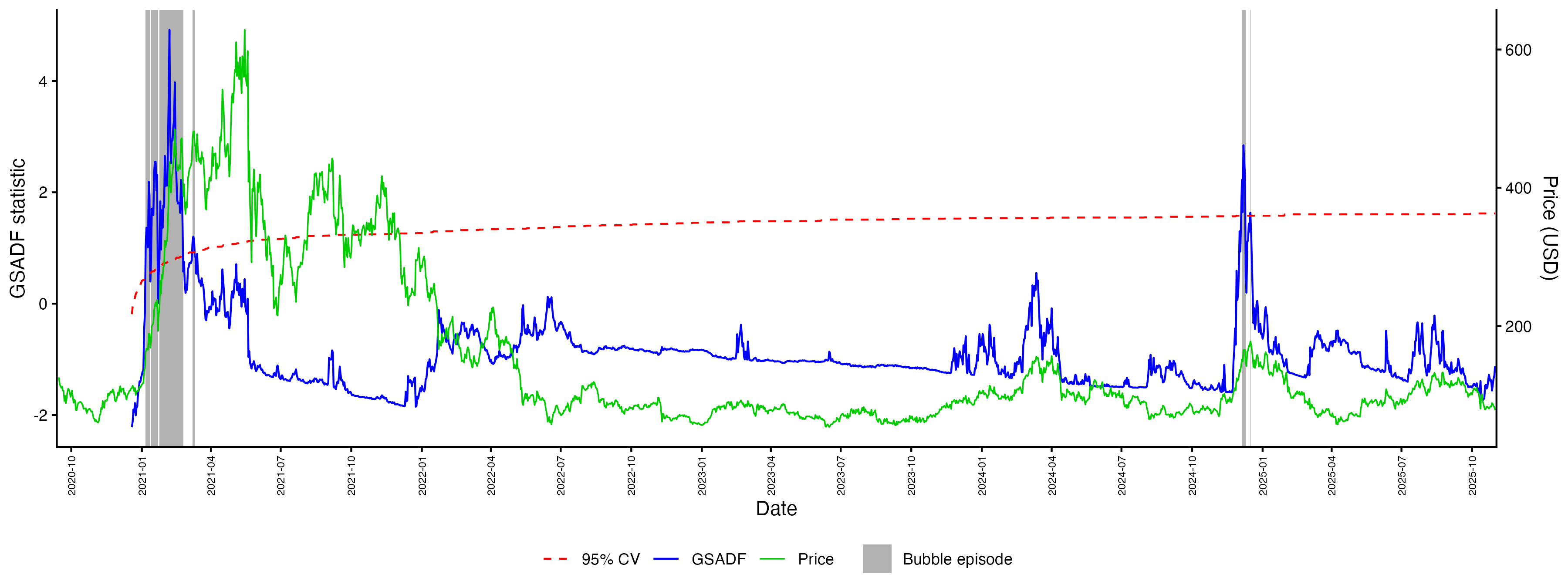

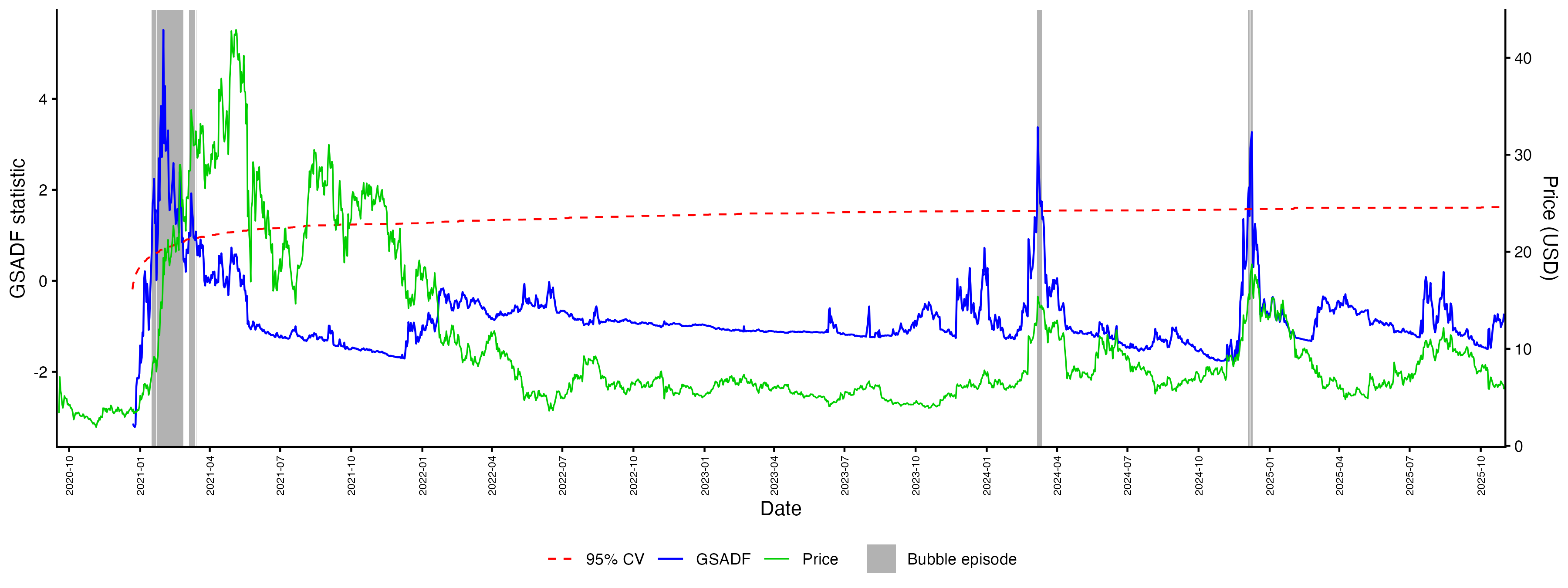

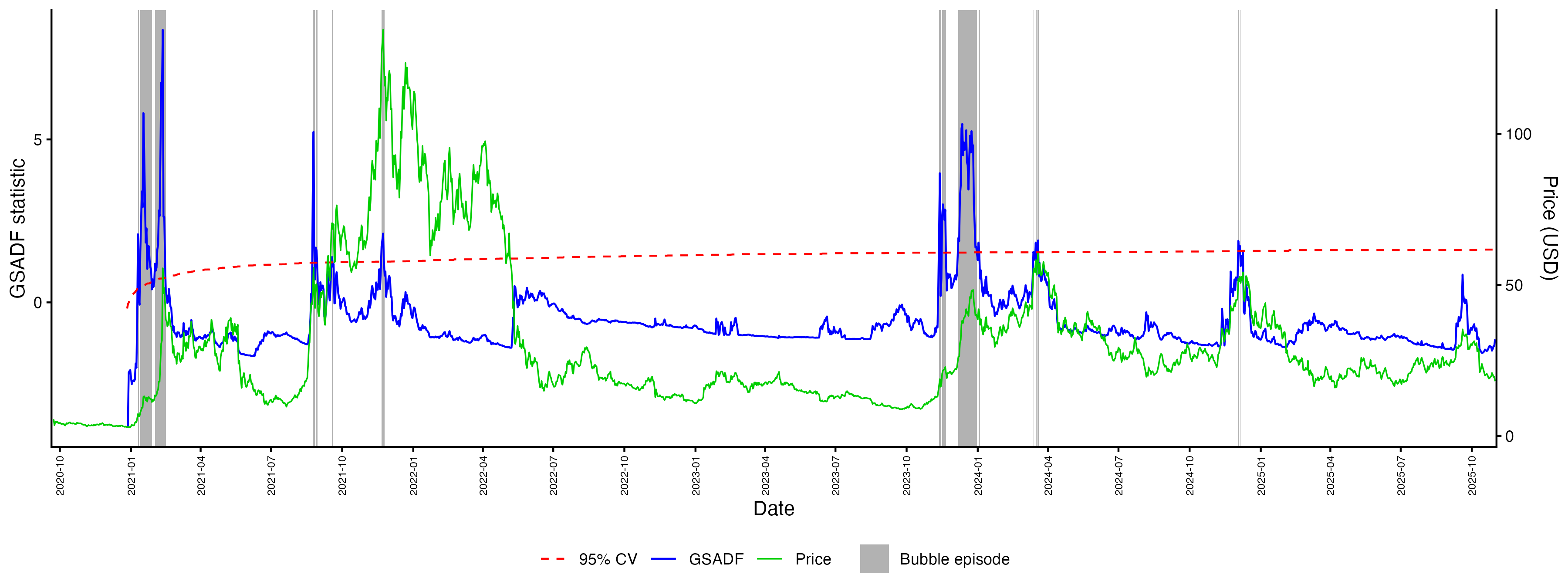

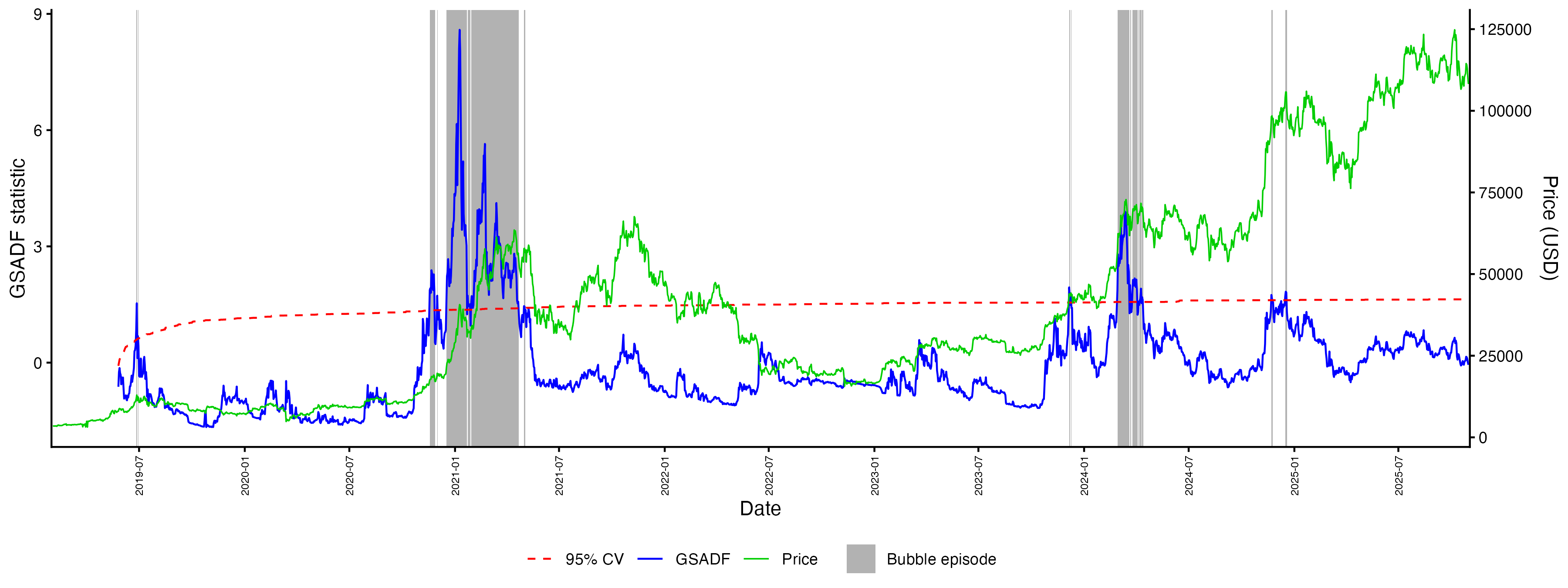

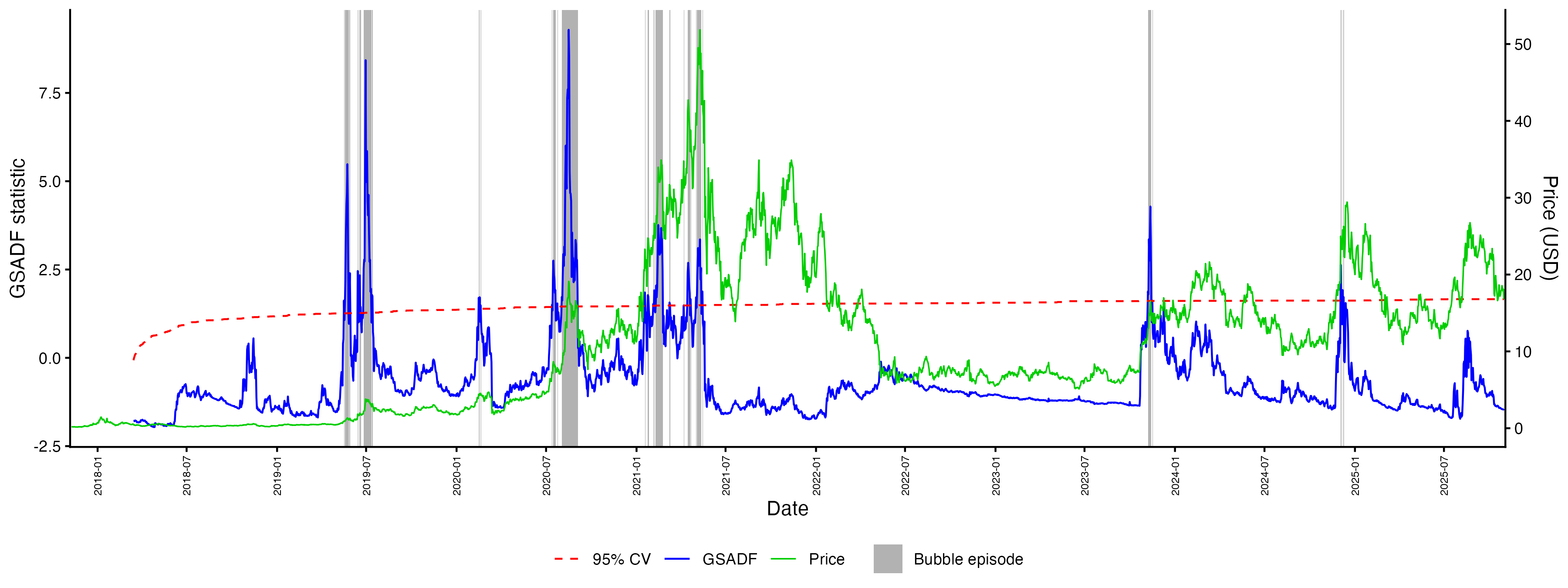

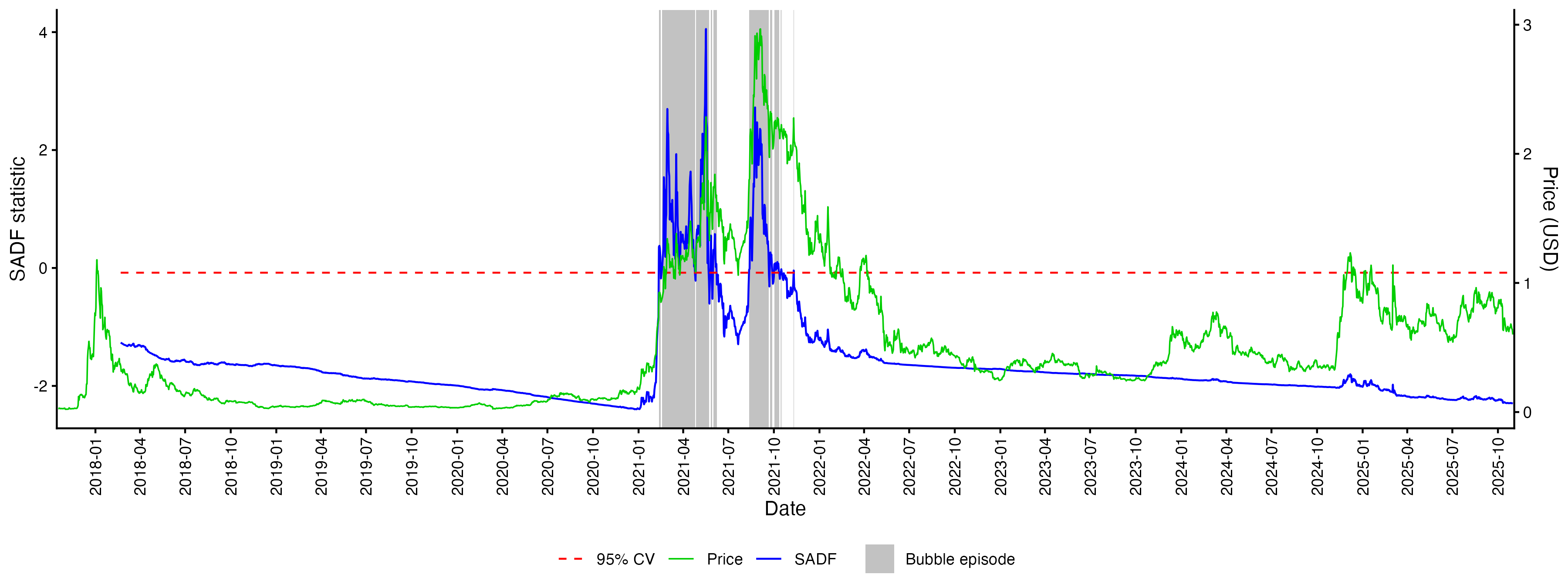

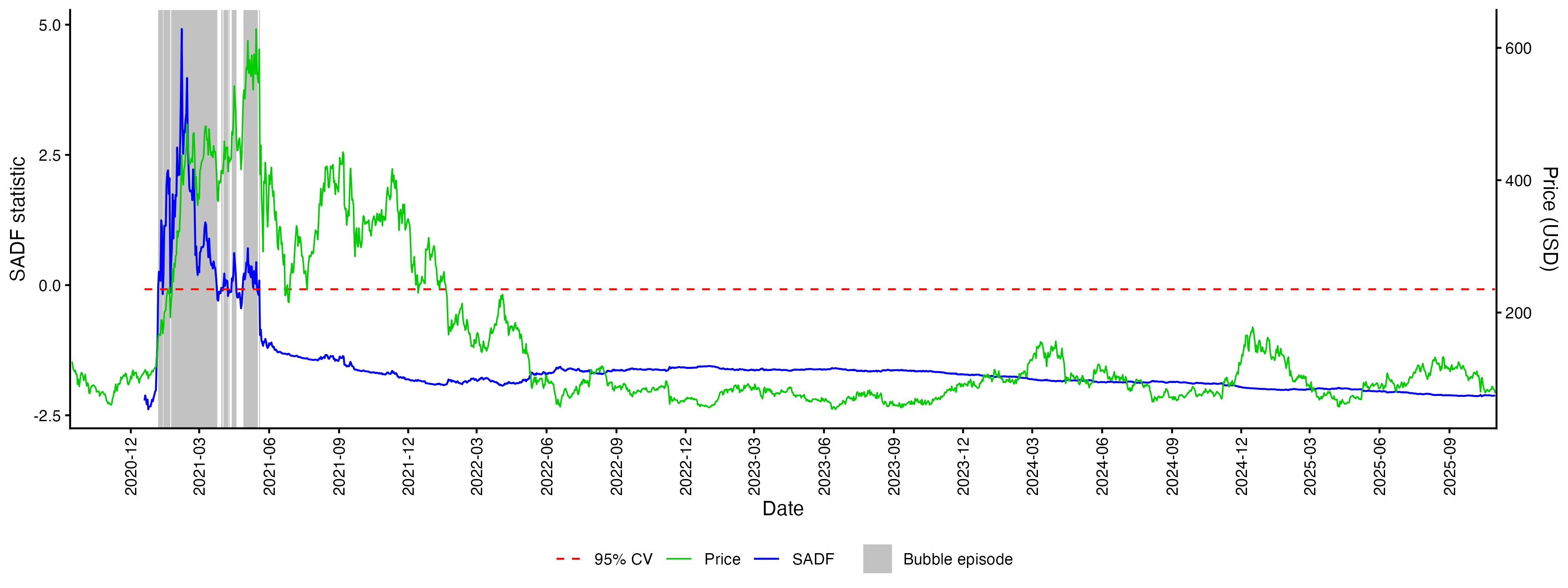

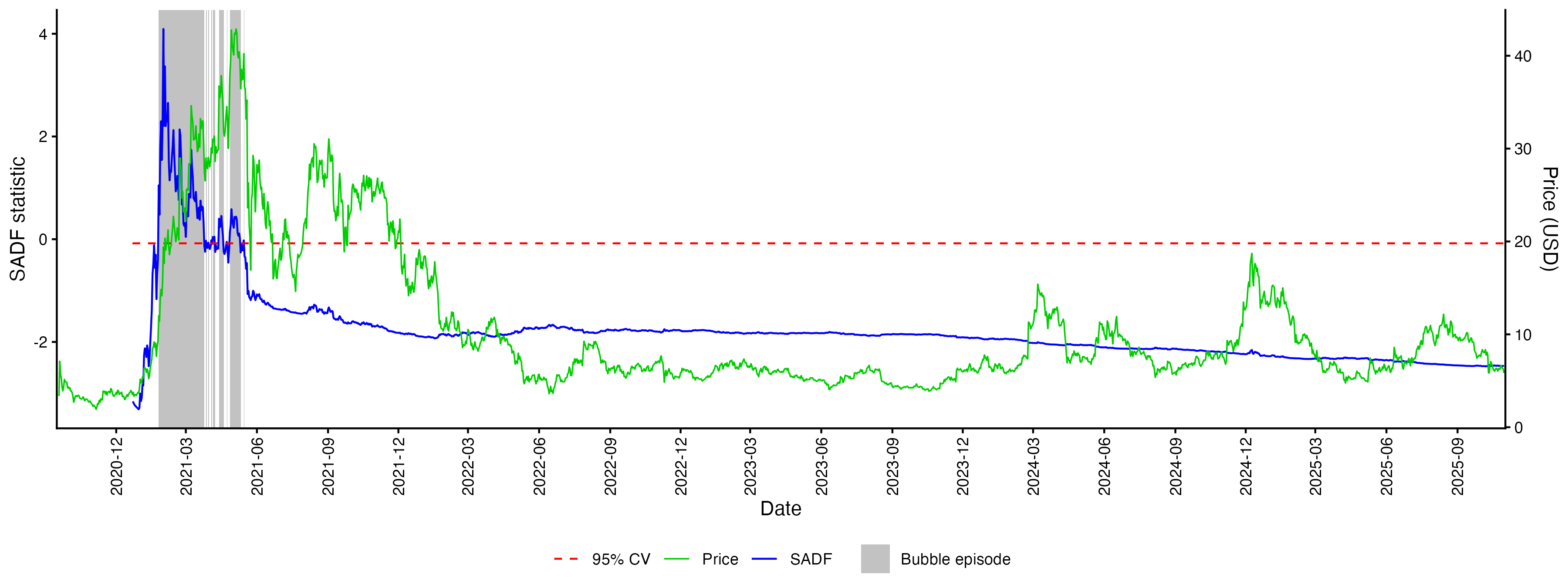

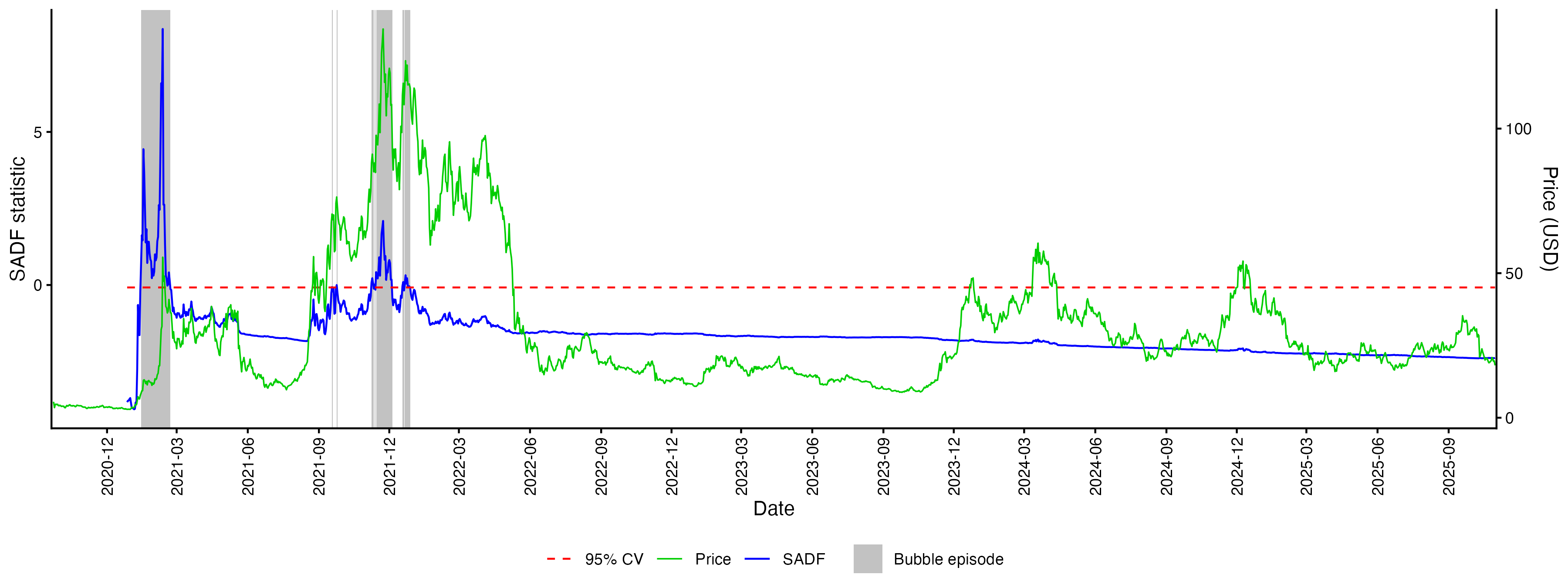

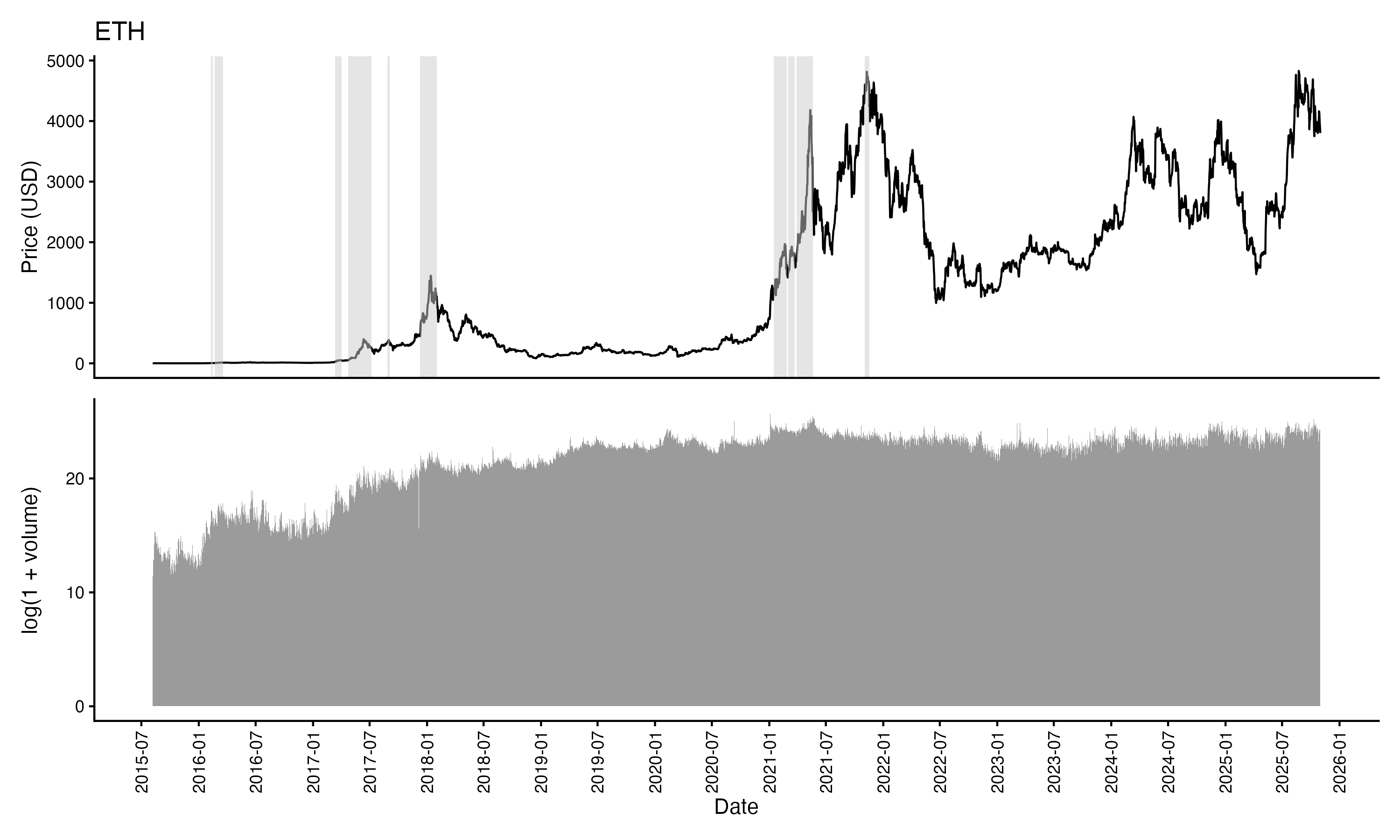

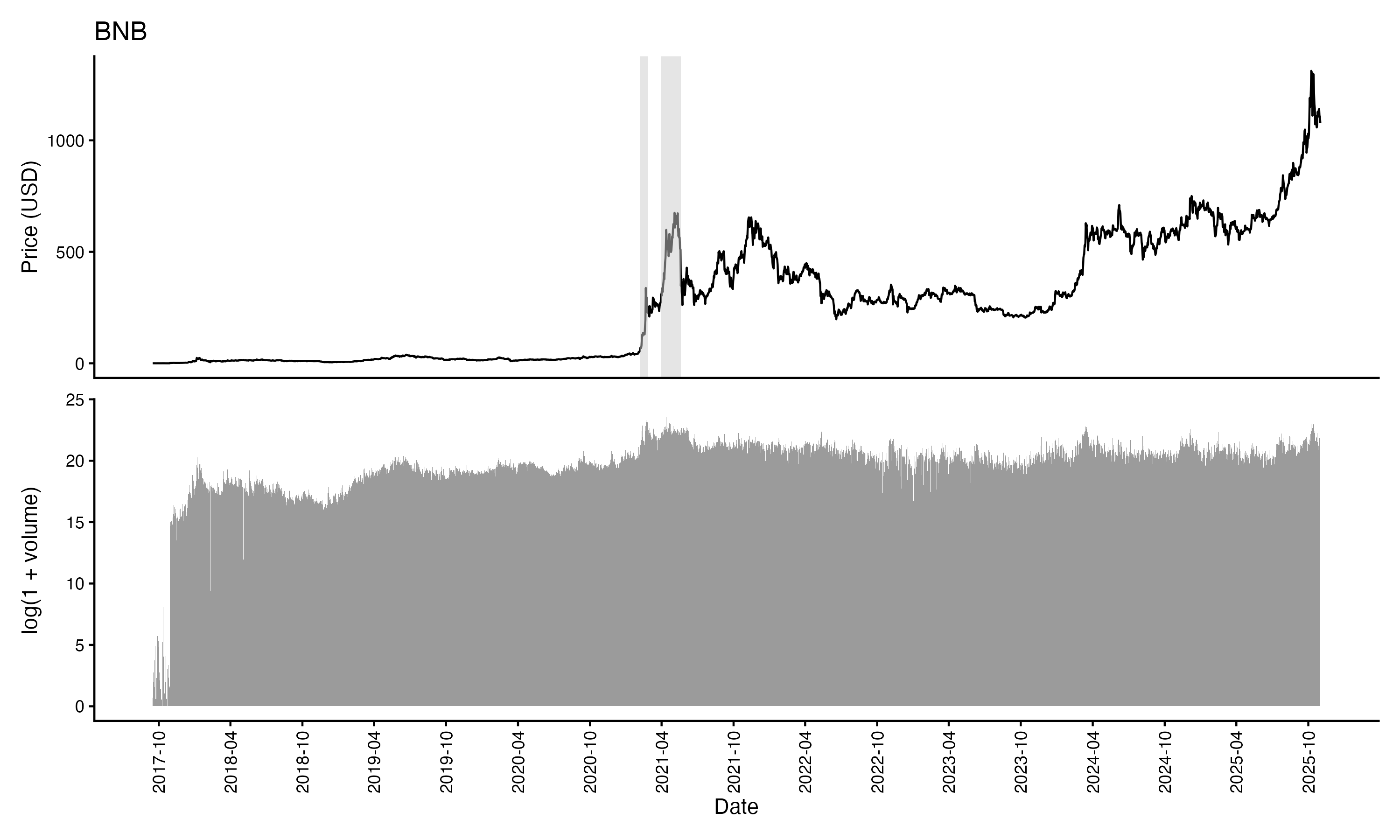

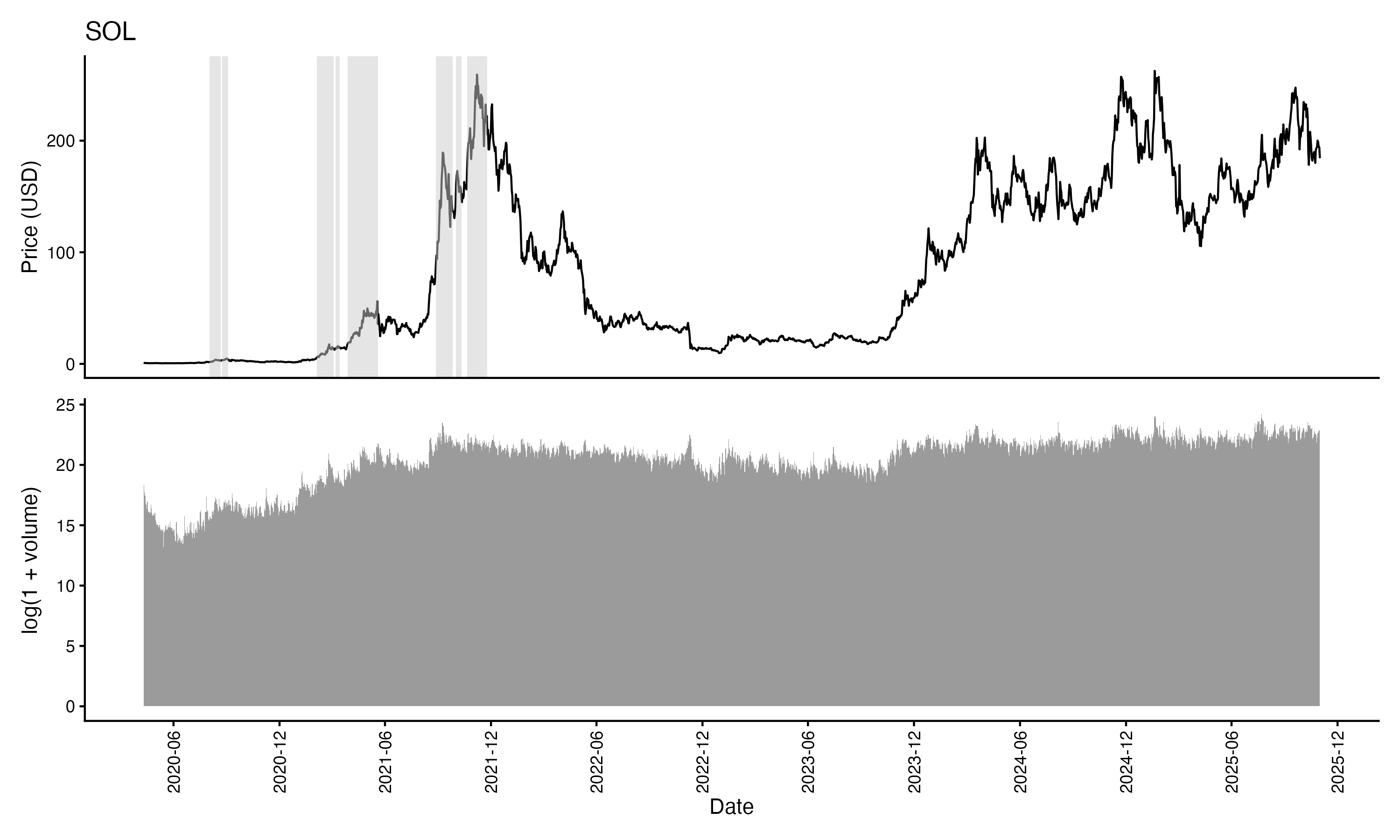

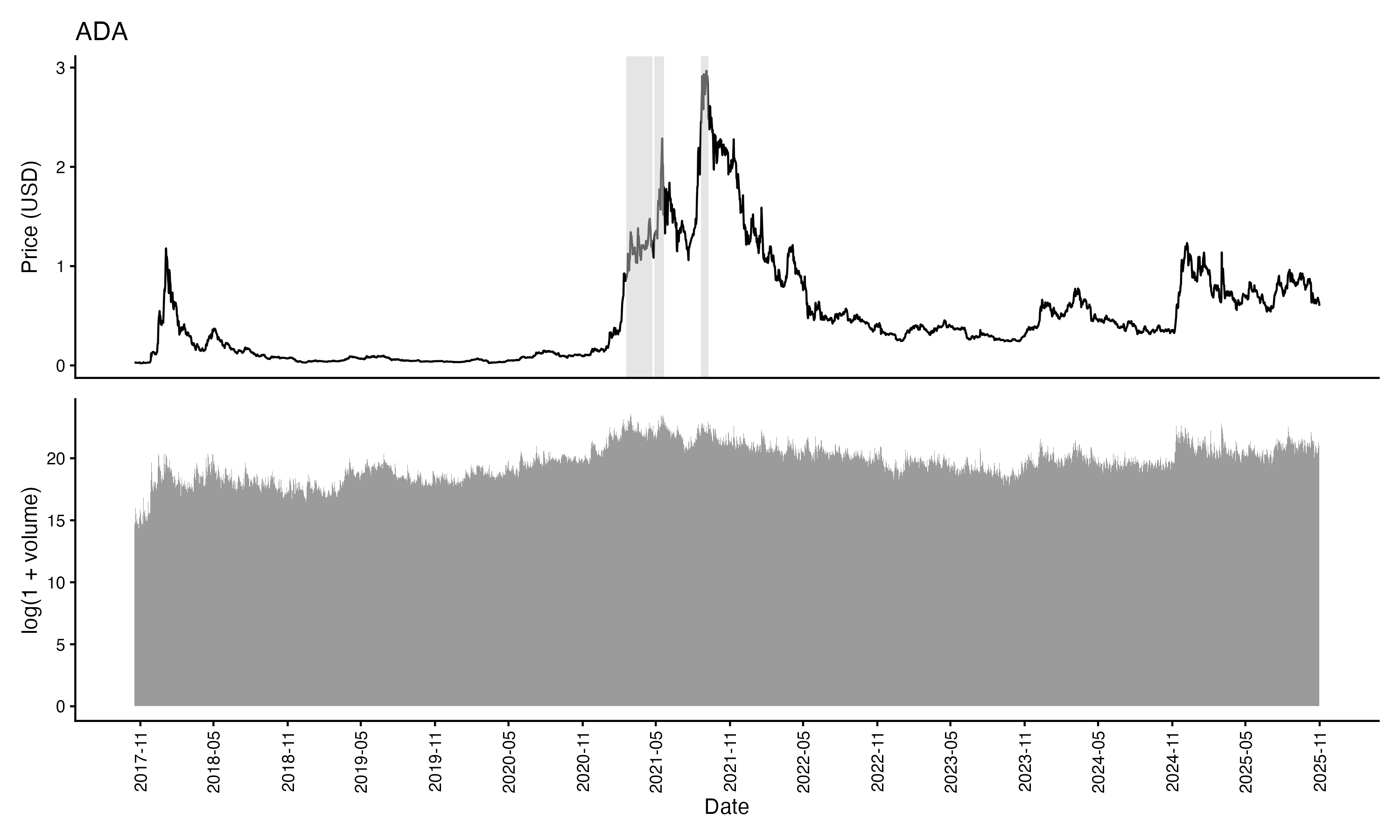

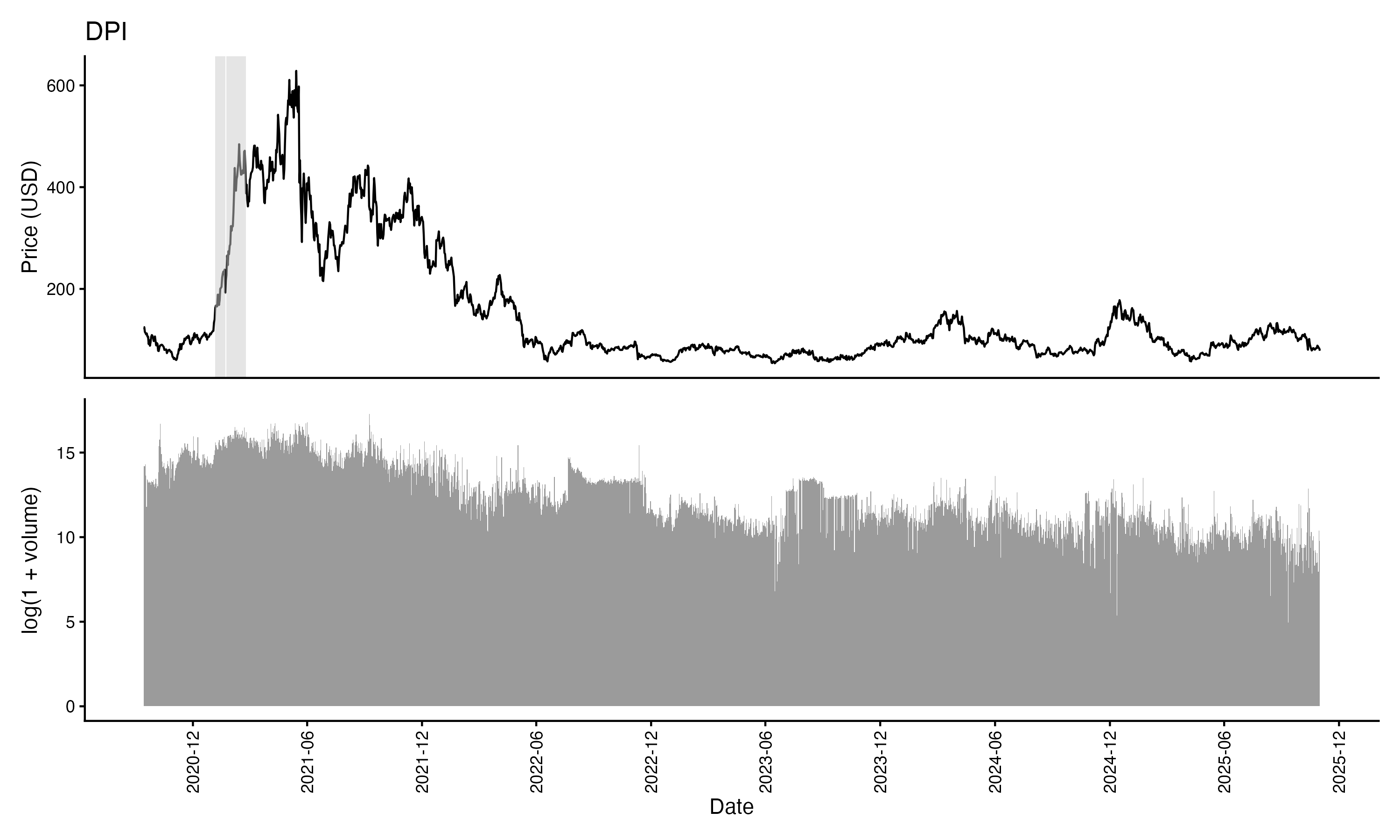

All assets exhibit recurrent bubble regimes with heterogeneous frequency and intensity. ETH shows highest bubble coverage (19.53% SADF), while DPI spends more time in bubble states than NFTI.

Three Boom-Bust Phases

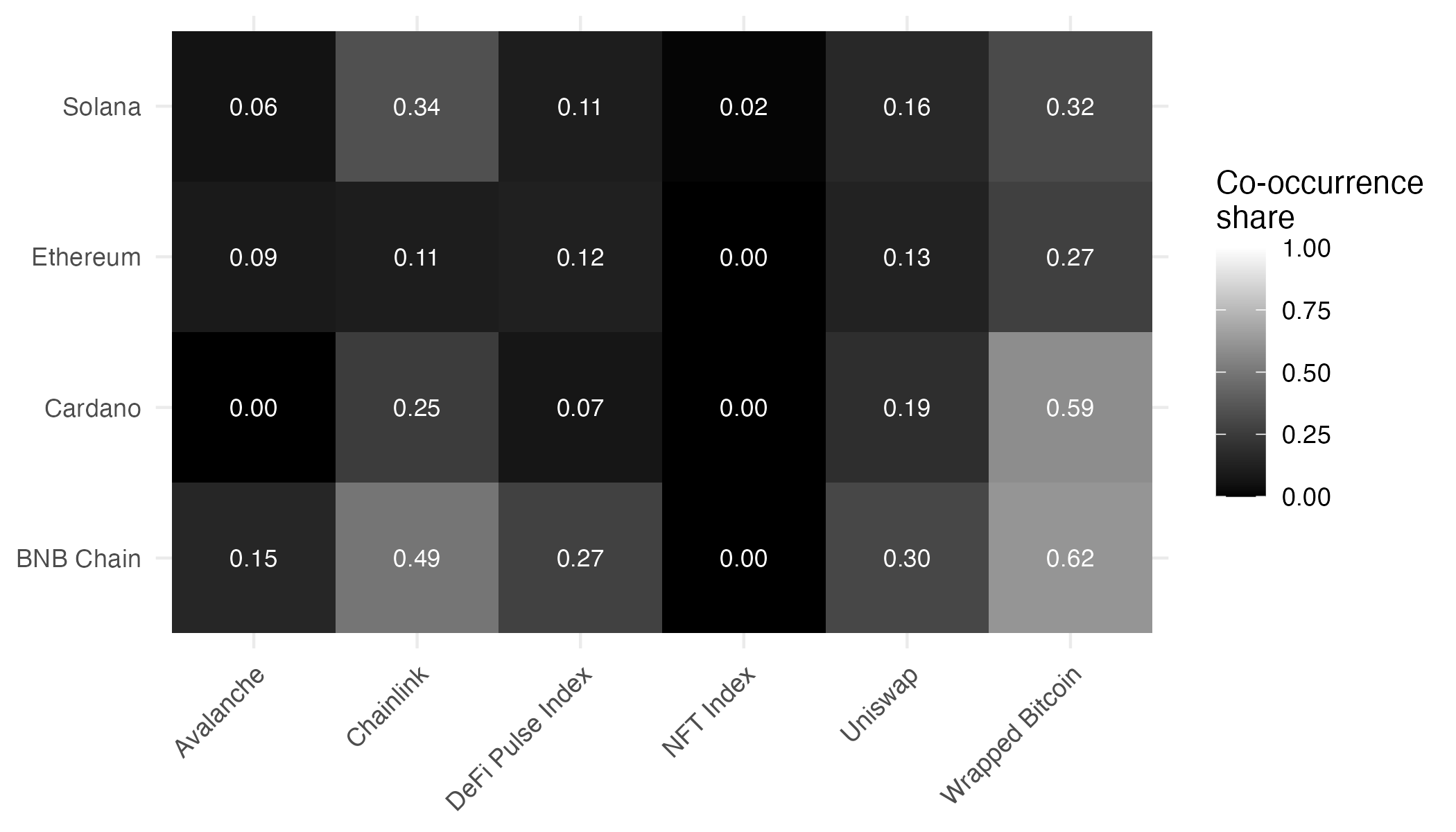

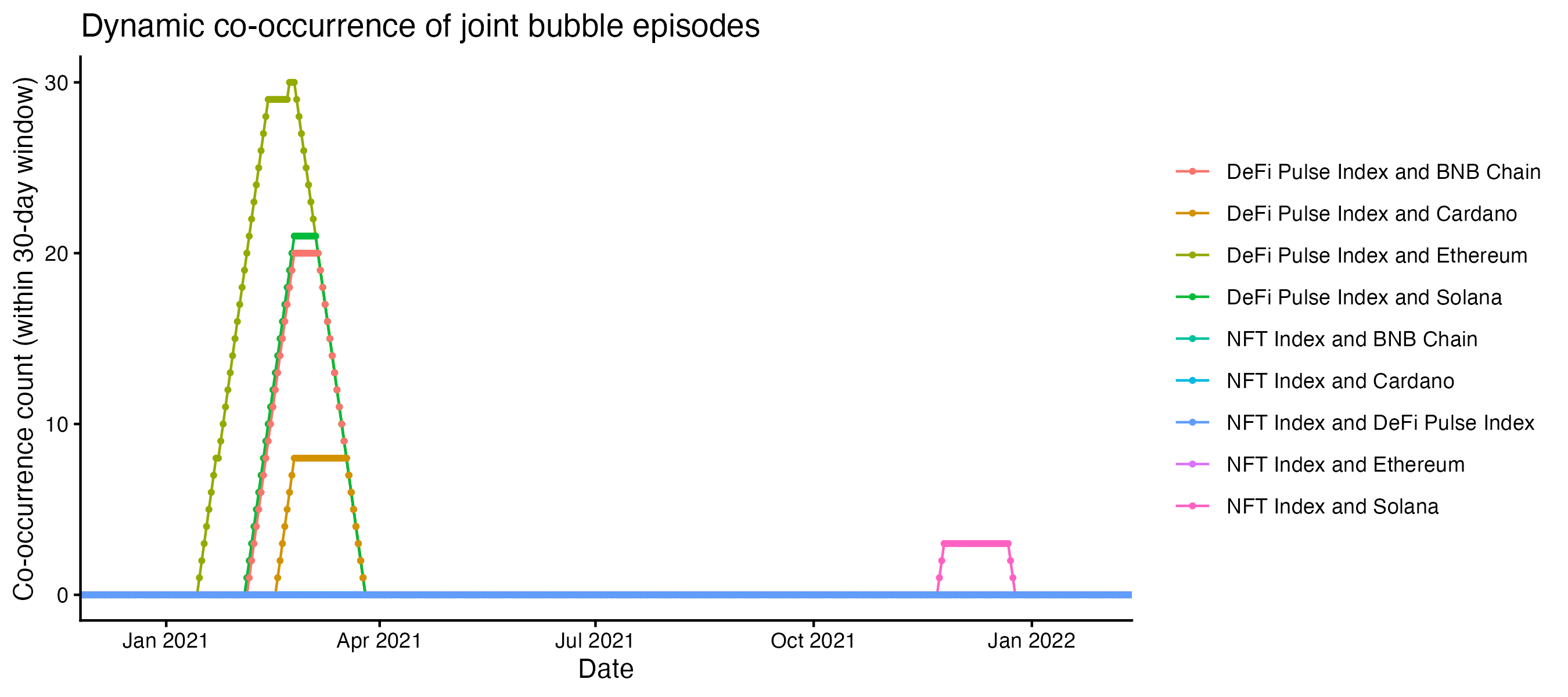

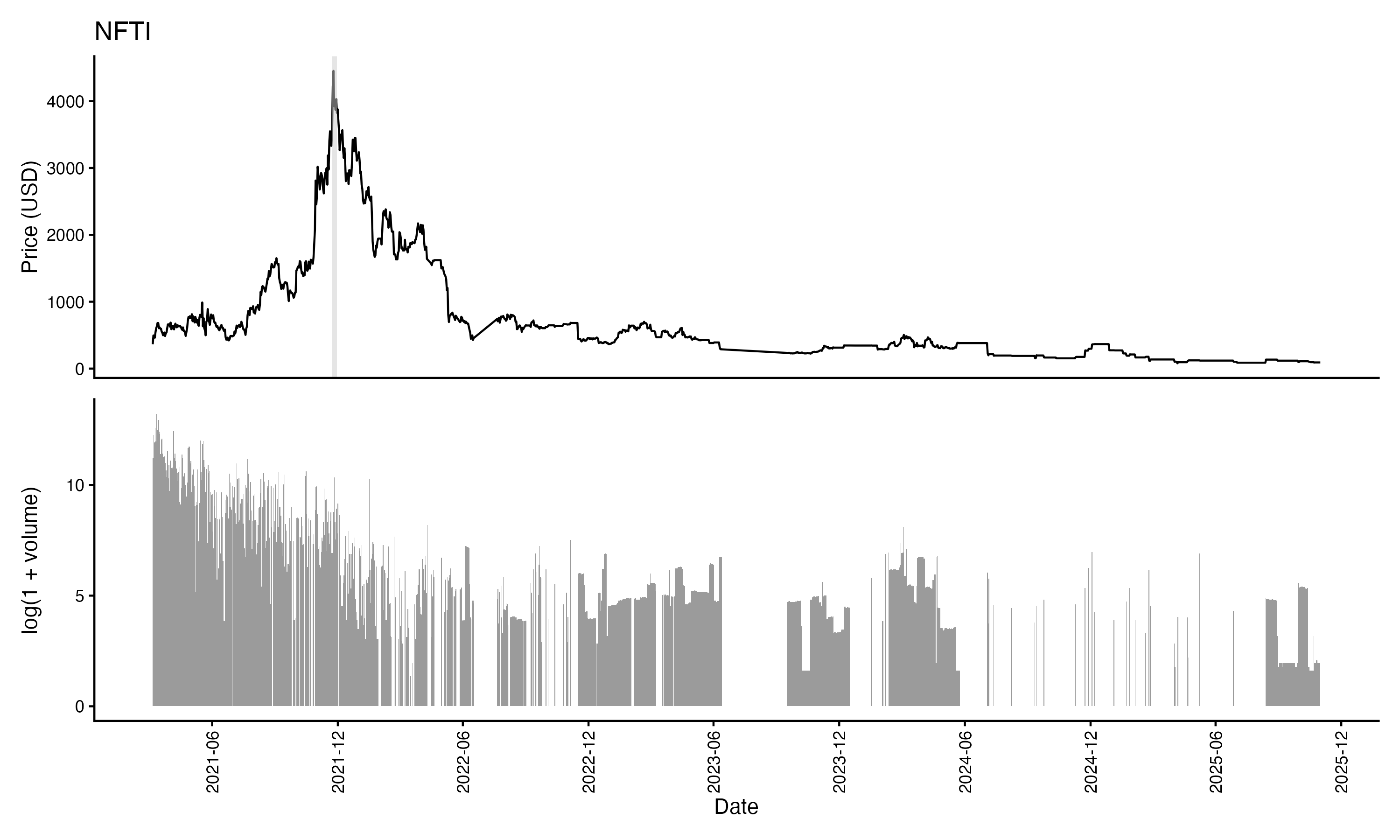

Bubble episodes cluster around: (1) DeFi Summer 2020, (2) Crypto/DeFi boom early 2021, and (3) NFT-centered bull run late 2021. Co-occurrence patterns show synchronized exuberance.

Liquidity Association

Bubble regimes systematically associated with elevated trading activity. Joint bubble days display pronounced increases in log trade volume relative to non-bubble periods.

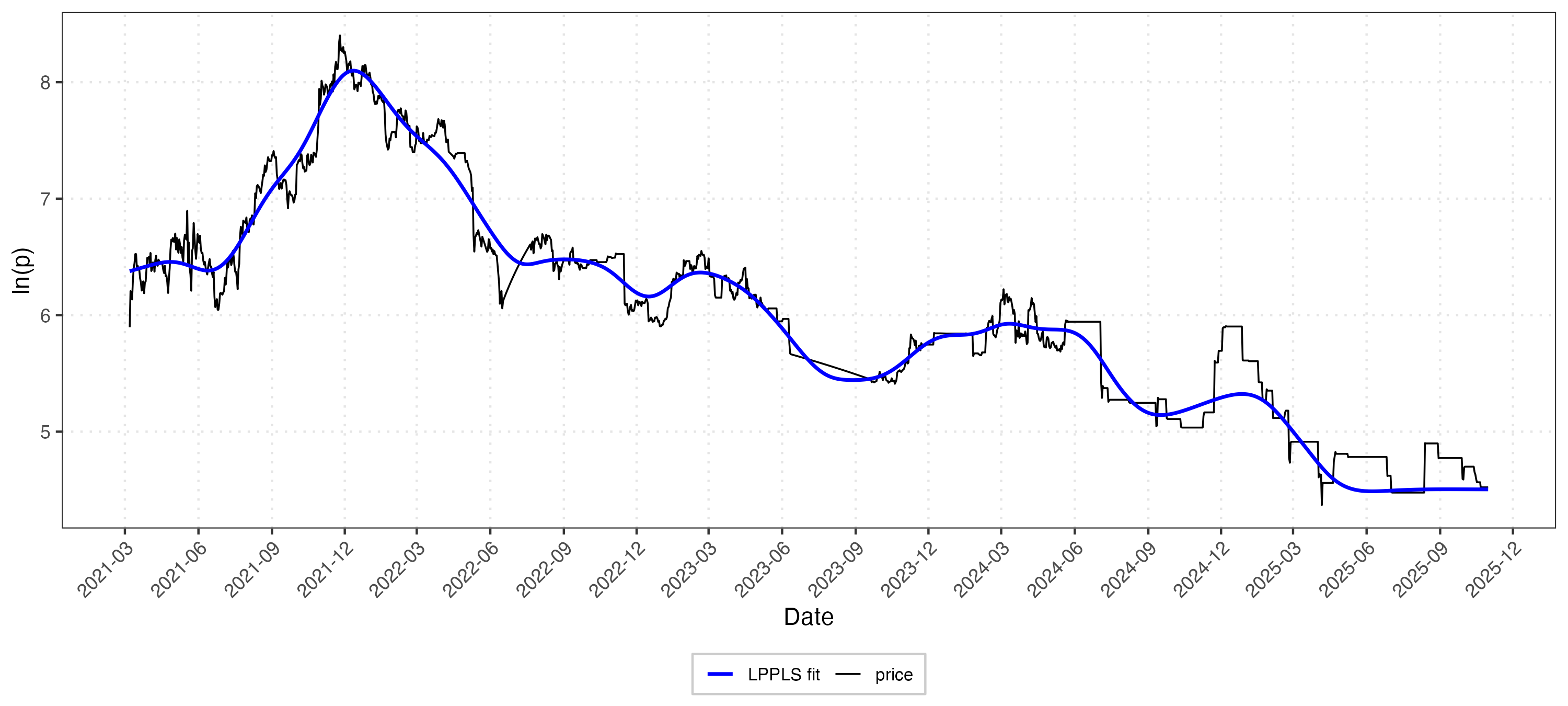

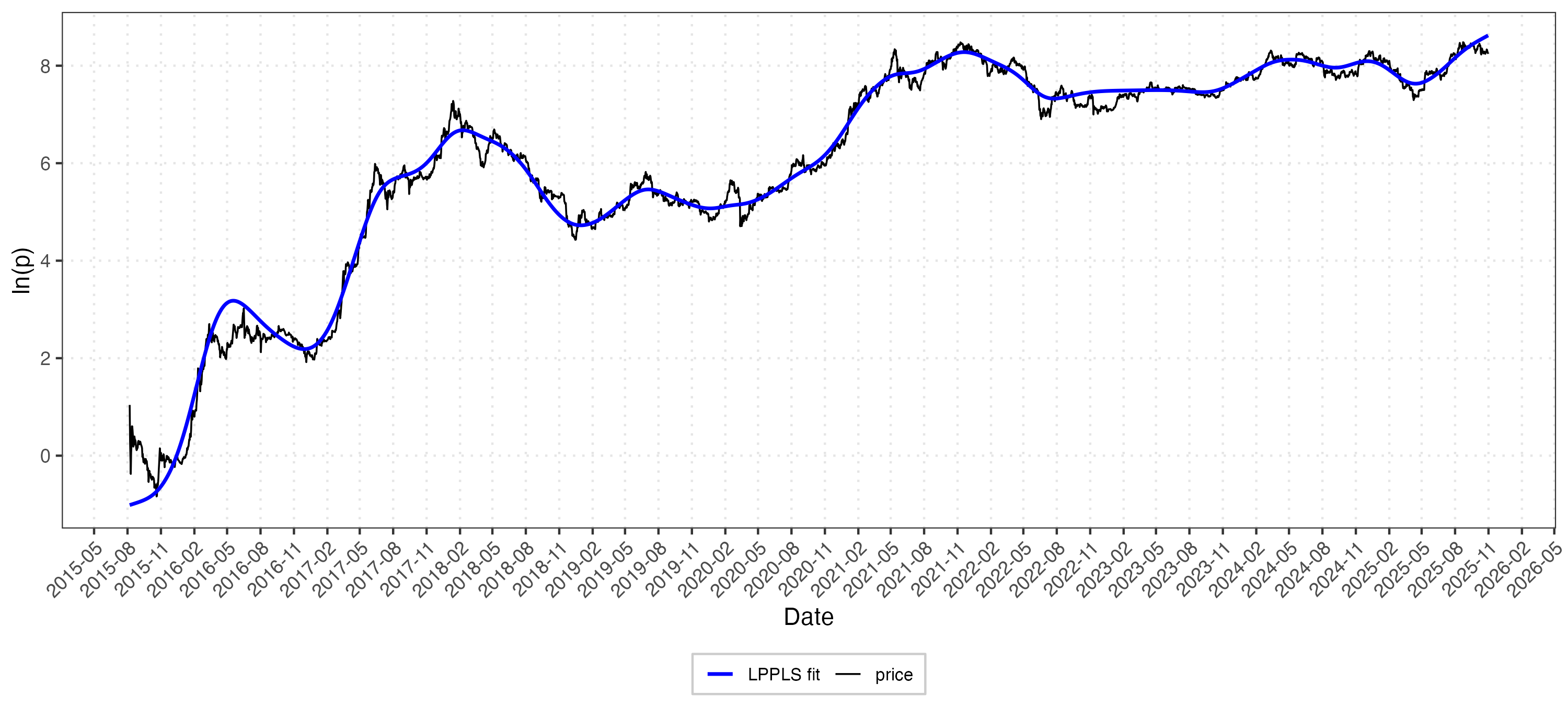

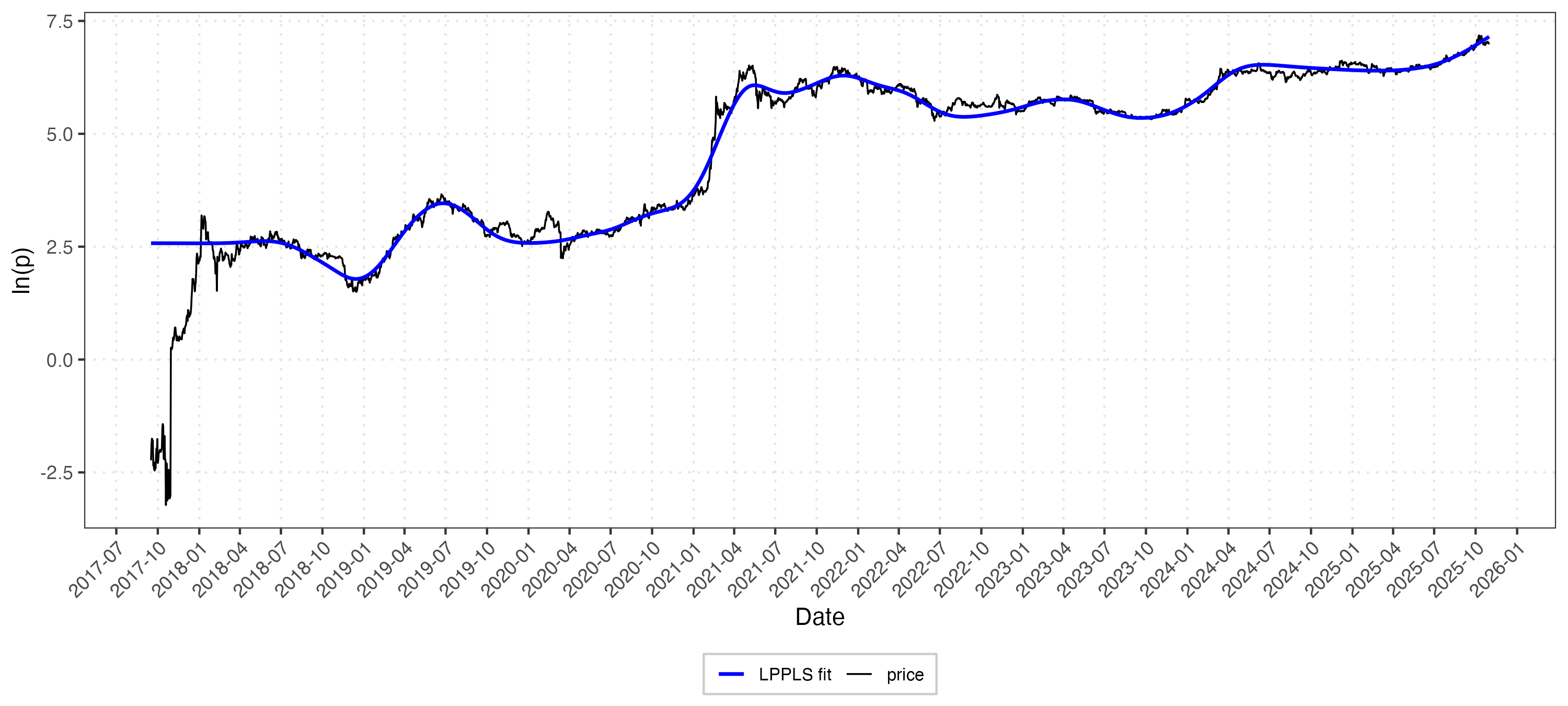

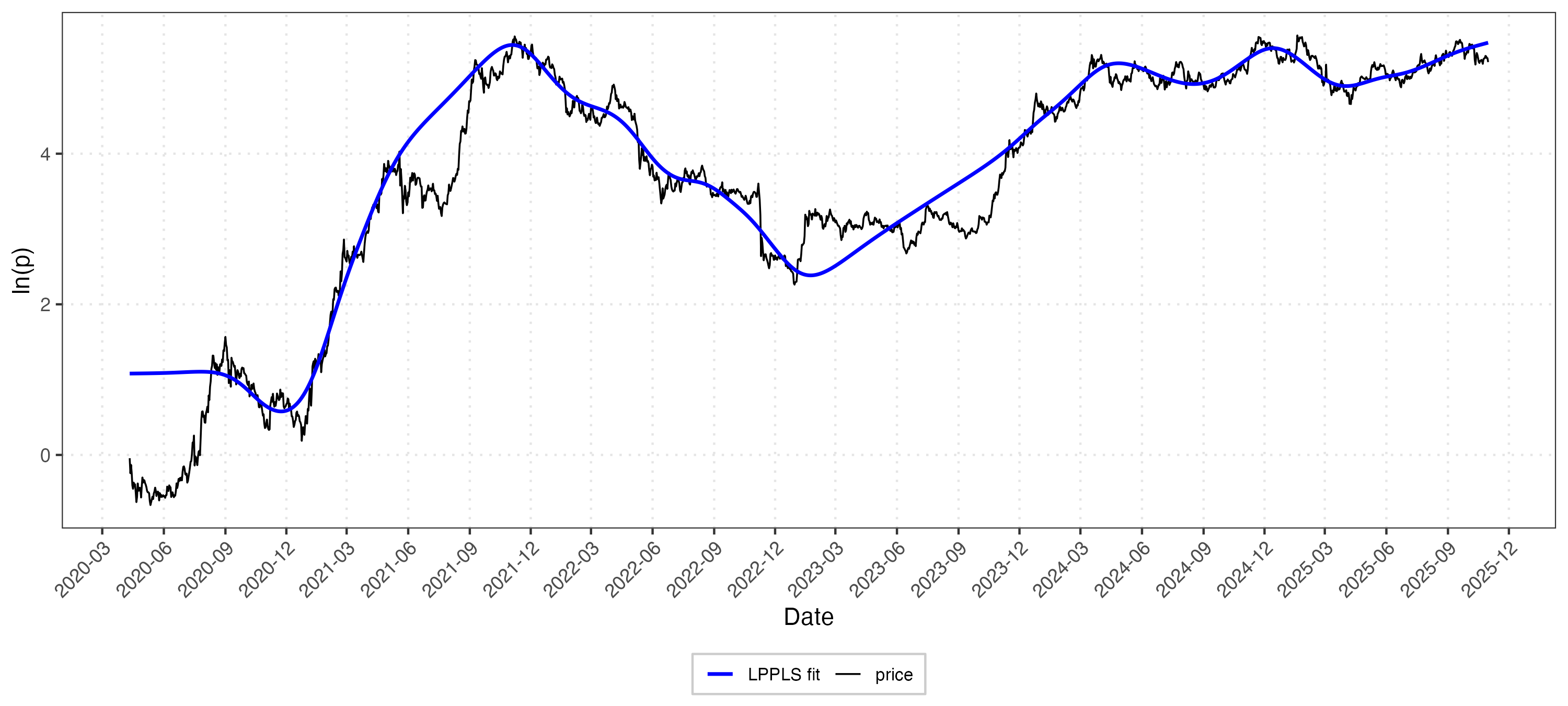

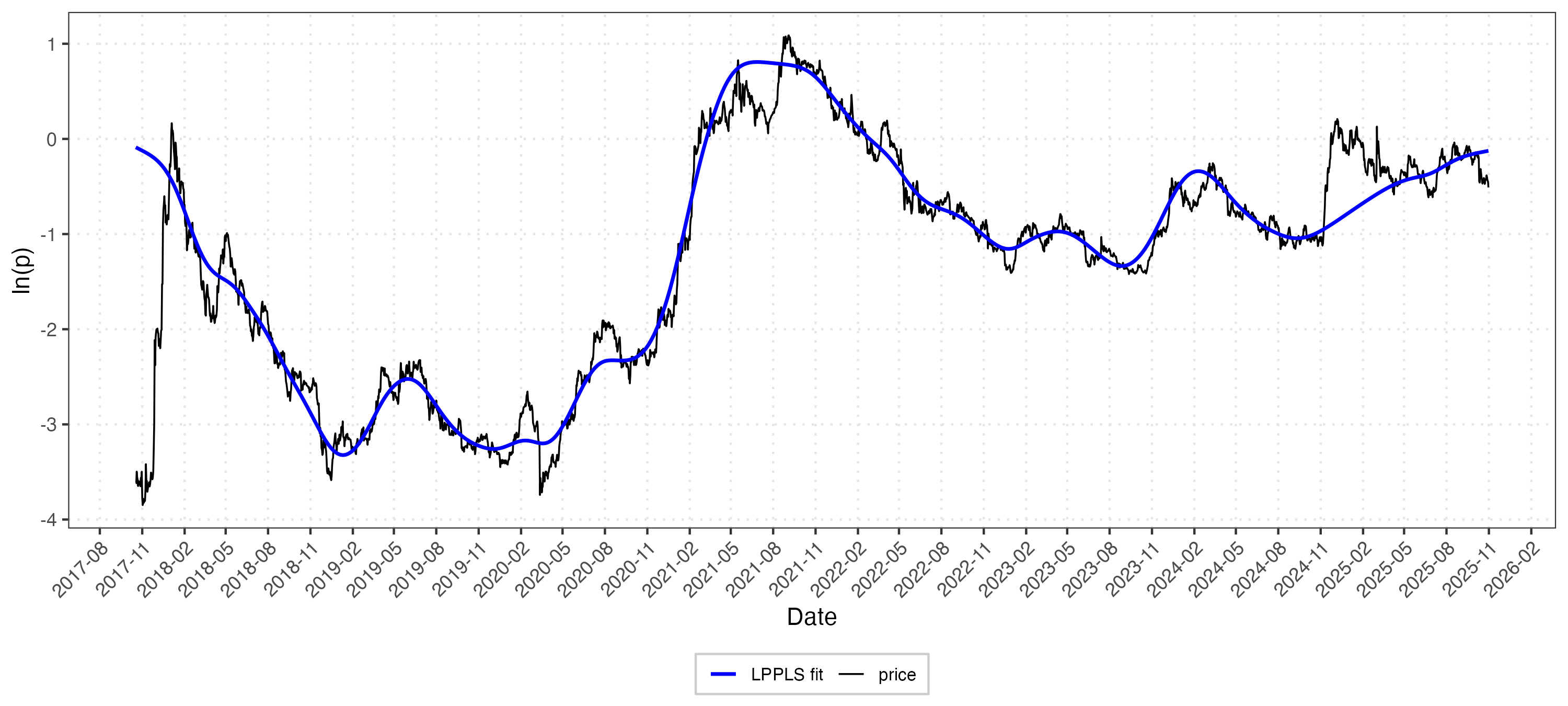

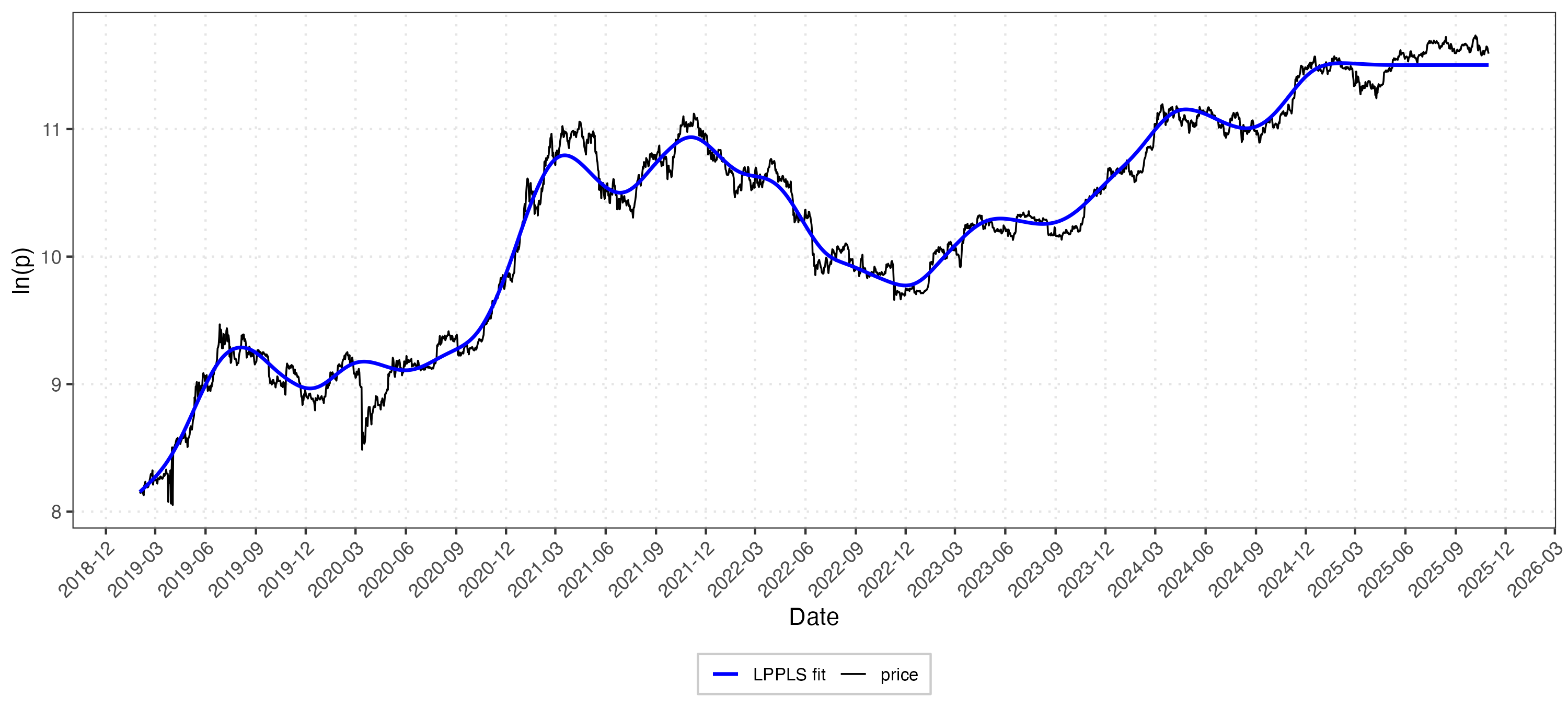

NFT Index

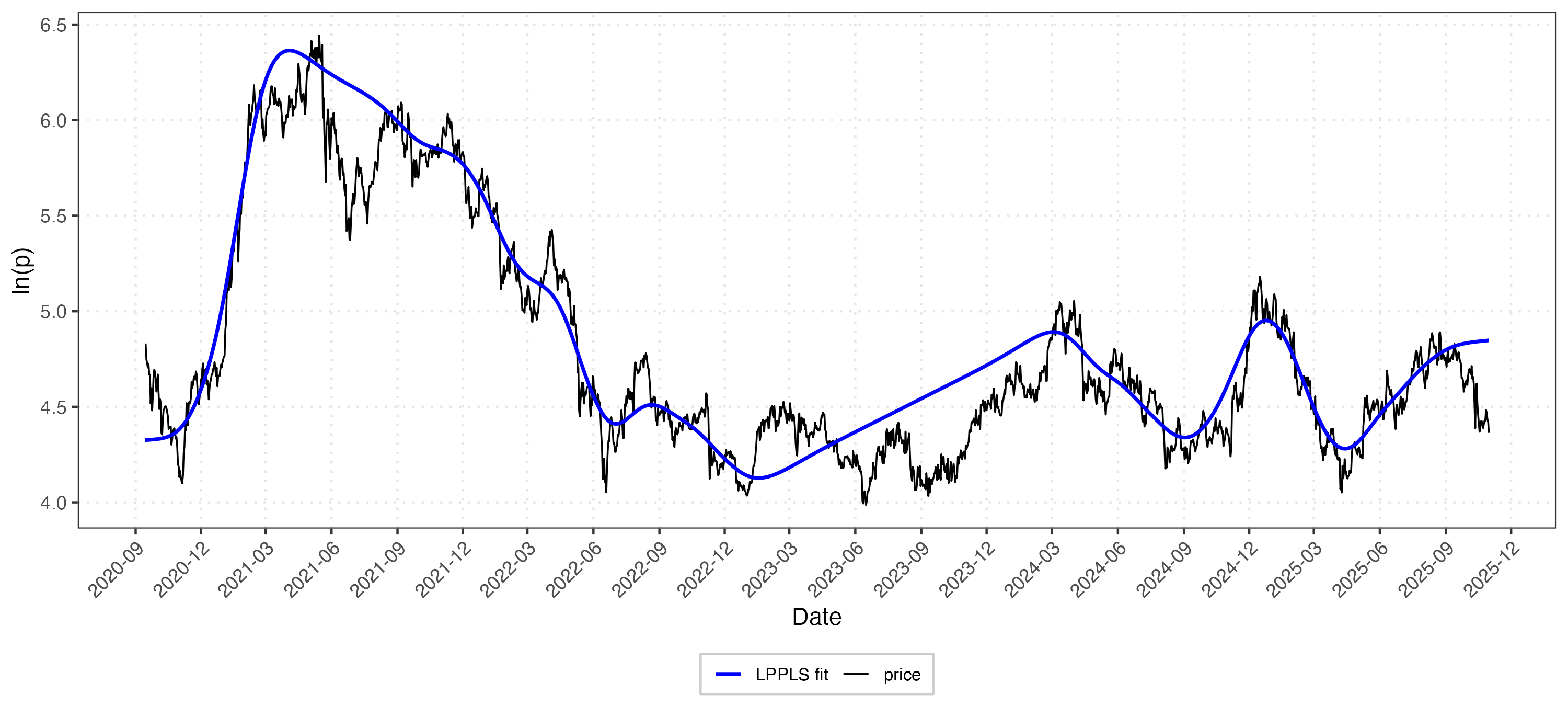

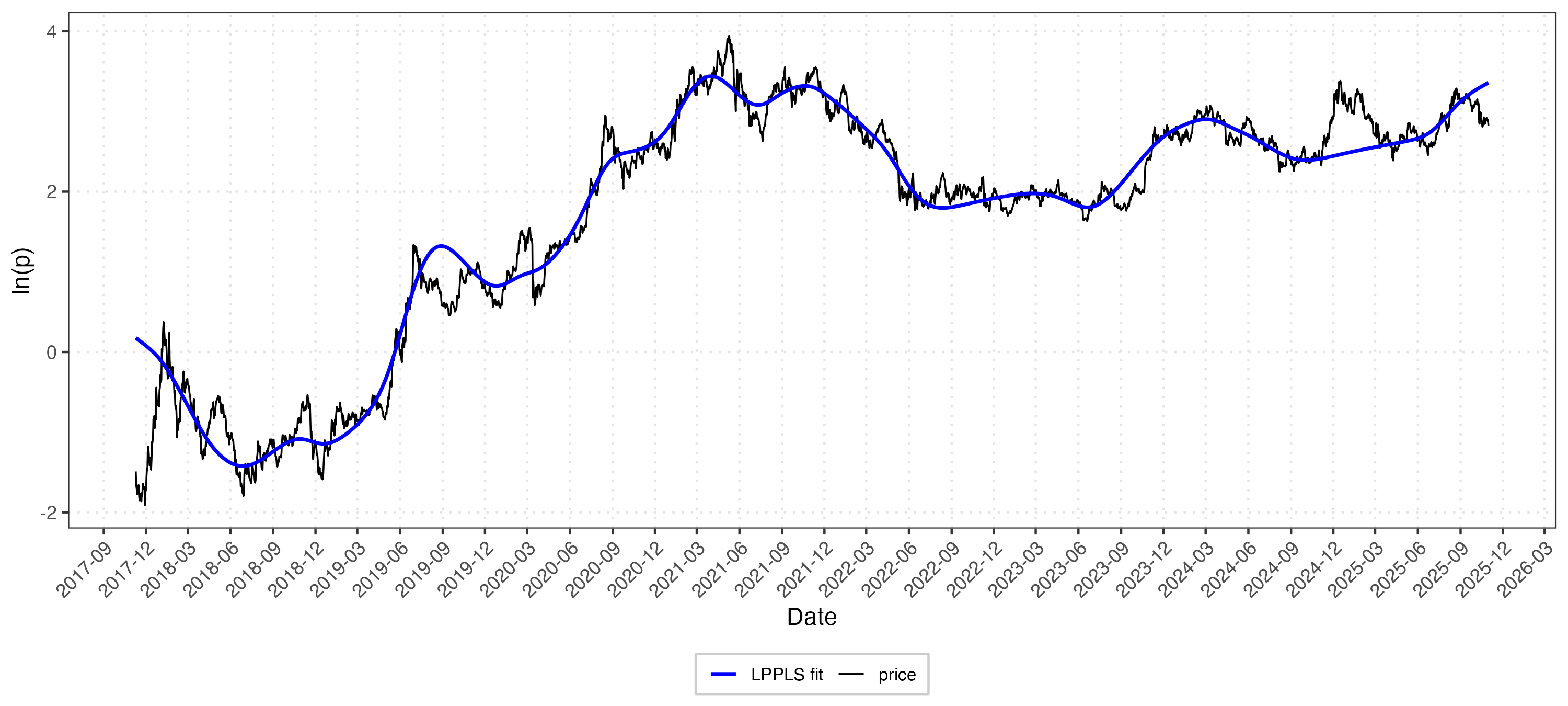

DeFi Pulse Index

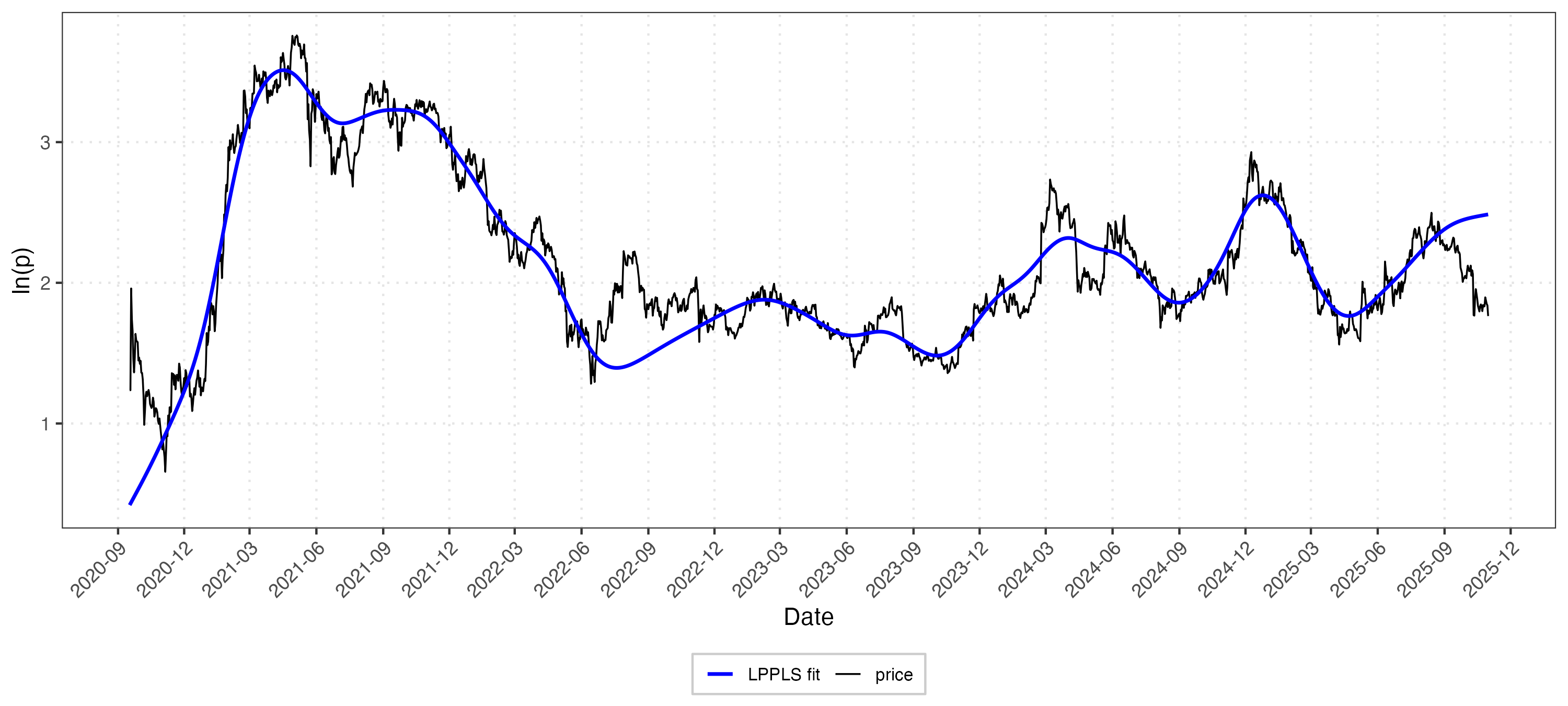

Ethereum

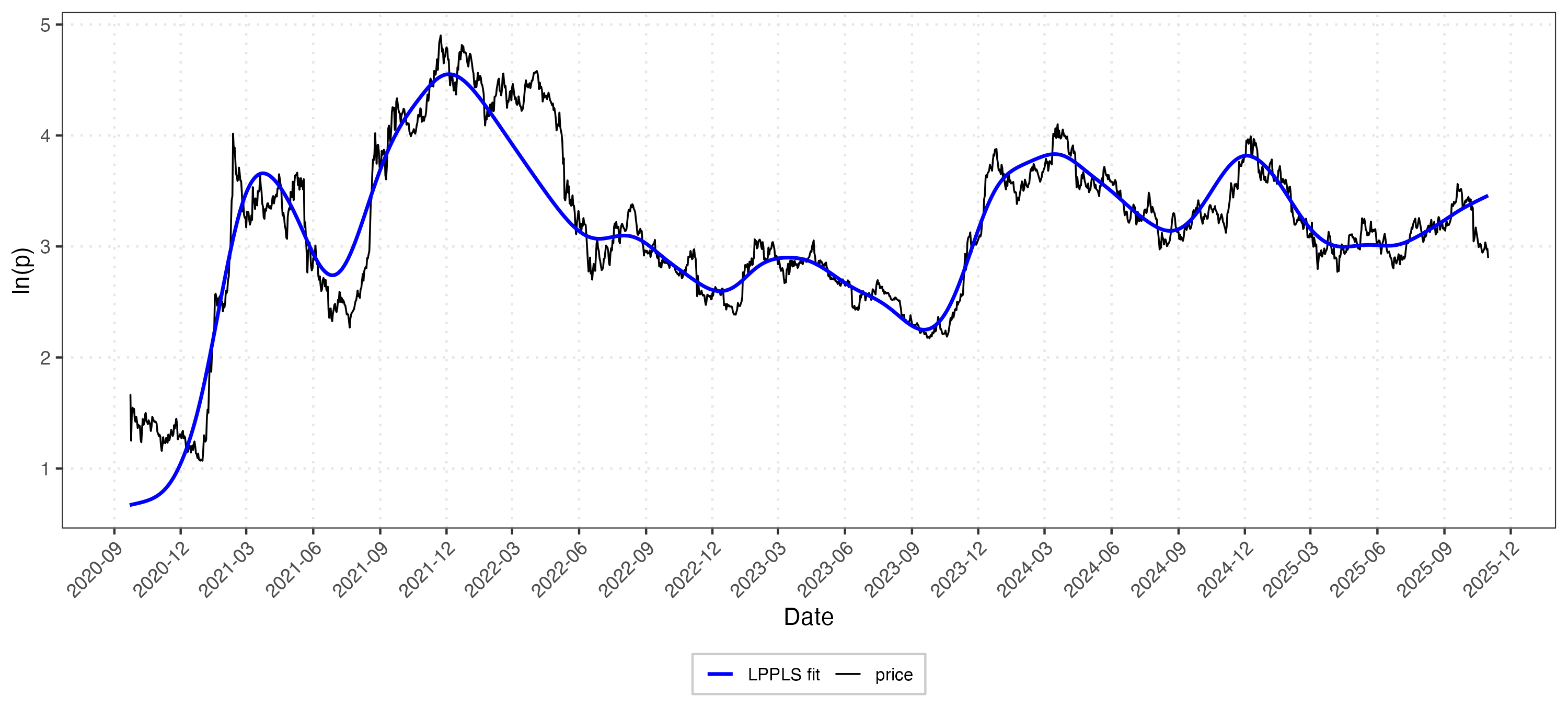

Binance Coin

Solana

Cardano

Uniswap

Avalanche

Wrapped Bitcoin

Chainlink

SADF Test

Supremum Augmented Dickey-Fuller test for detecting single bubble episodes using forward-recursive regression windows.

GSADF Test

Generalized SADF for multiple bubble detection with flexible start/end windows. More powerful for recurring episodes.

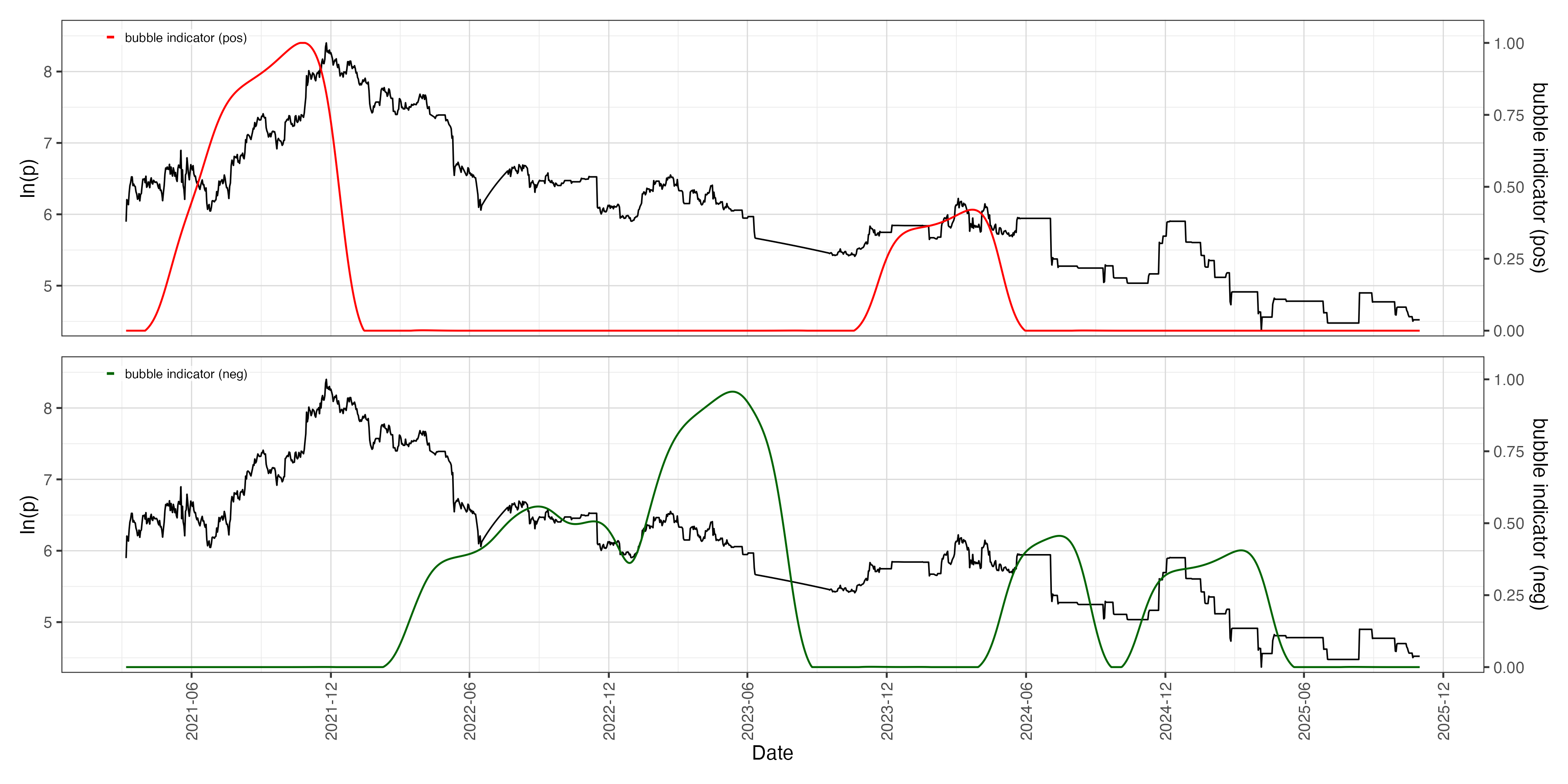

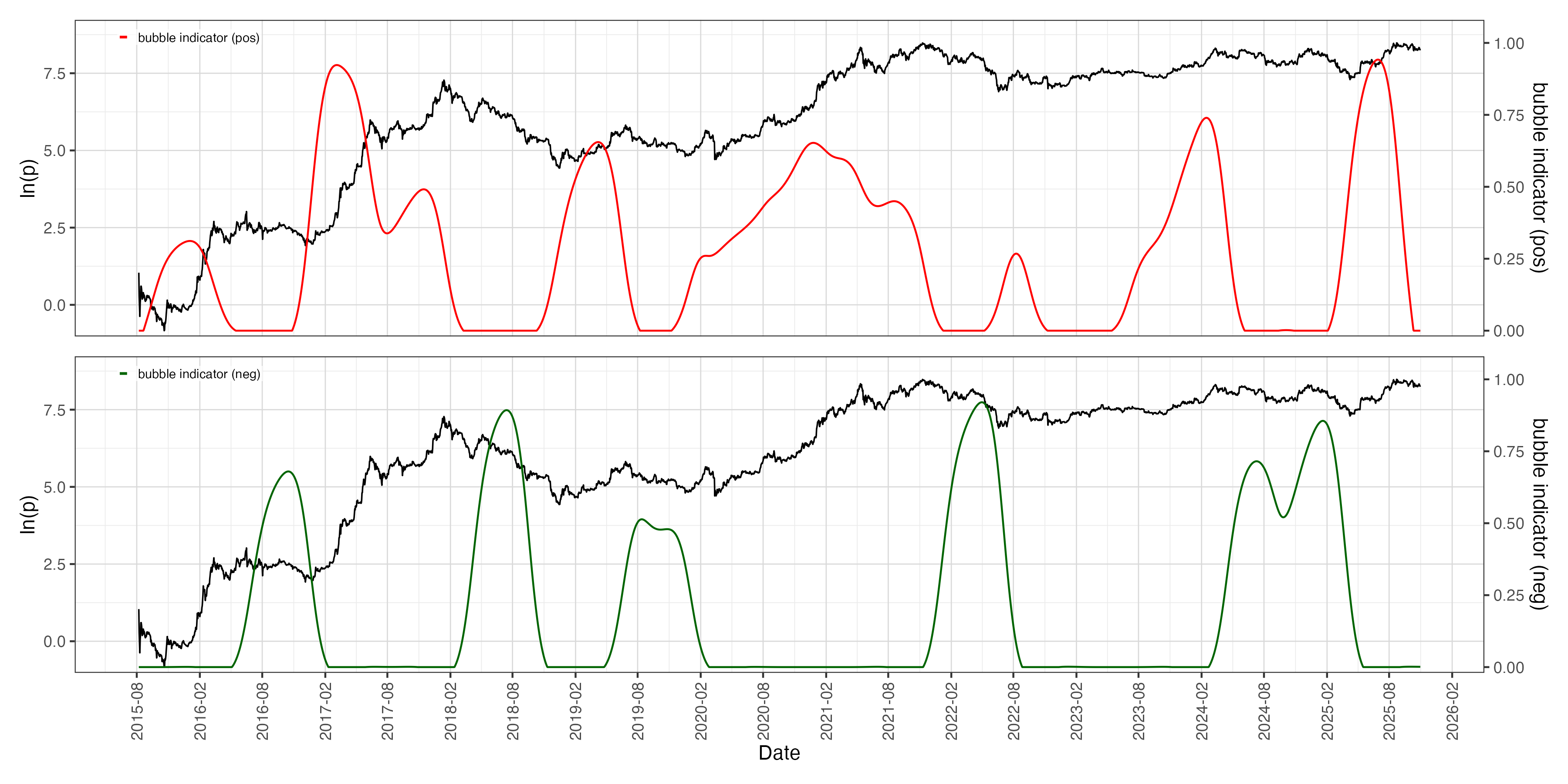

LPPLS Framework

Log-Periodic Power Law Singularity model for robustness check. Identifies bubble run-ups and crash predictions.

Date-Stamping

Joint bubble indicator requiring 7+ consecutive days of overlapping SADF and GSADF intervals for conservative identification.

Detecting Price Bubble Formation in NFT and DeFi Markets

Lennart J. Baals (University of Twente)

This deposit provides the full research code and executable analysis pipeline for Chapter 2 of a doctoral dissertation on risk management in digital finance. The work examines price bubble dynamics in NFT and DeFi markets using a reproducible R/Quarto workflow combining PSY bubble tests (SADF/GSADF), LPPLS robustness analysis, and liquidity assessment.

License

MIT License

Language

R (>=4.0)

Size

15.6 MB

Published

Jan 5, 2026

Repository Contents:

R Dependencies:

tidyverse, tseries, moments, exuber, arrow, patchwork, janitor

Related Publication:

Wang, Y., Horky, F., Baals, L. J., Lucey, B. M., & Vigne, S. A. (2022). Bubbles all the way down? Detecting and date-stamping bubble behaviours in NFT and DeFi markets. Journal of Chinese Economic and Business Studies, 20(4), 415-436. [DOI]

Funding: Swiss National Science Foundation (Grant IZCOZ0-213370): "Narrative Digital Finance: a tale of structural breaks, bubbles & market narratives"

Note: Raw market data excluded due to third-party licensing restrictions. Users must obtain data from original vendors (WorldCoinIndex, CoinGecko) independently.