A3: Will CBDCs Kill Commercial Banks?

Introduction

A CBDC (Central Bank Digital Currency — digital money issued directly by a country's central bank, like a digital version of cash) could cause bank disintermediation (when people move their money from commercial banks to the central bank's digital currency). This model simulates how bank deposits D change over time using a differential equation (a formula describing how something changes from one moment to the next):

dD/dt = -α(r_CBDC - r_D)D + β·confidence(t)

Where:

- α (alpha) = rate sensitivity — how strongly the interest rate gap drives deposit outflow

- r_CBDC = interest rate on CBDC

- r_D = interest rate on bank deposits

- β (beta) = confidence sensitivity — how much public confidence affects deposits

- ODE = Ordinary Differential Equation — a math formula that describes continuous change over time

Variations to Explore

Variation 1: Increase Rate Sensitivity

Task: Change α from 0.8 to 2.0

Question: How much faster do deposits flee when people are more sensitive to interest rate differences?

Variation 2: Zero CBDC Interest Rate

Task: Set CBDC rate to 0% in all scenarios (instead of 0%, 1%, 2%)

Question: Do banks still lose deposits even if CBDC pays nothing? Why or why not?

Variation 3: Early Crisis

Task: Move crisis start from quarter 8 to quarter 2

Question: How does an early crisis change the outcomes? Why does timing matter?

Open Extension

Task: Add a "tiered CBDC" scenario where:

- CBDC pays 2% interest on the first EUR 3,000

- CBDC pays 0% interest above EUR 3,000

Question: How does this tiered structure protect banks compared to a flat 2% CBDC rate? Who benefits most from this policy design?

How to Run

- Google Colab (recommended): Upload the chart.py file to Google Colab

- Install dependencies: Run

!pip install scipyin a Colab cell (needed for solving the differential equation) - Run the code: Execute the chart.py file

- Create variations: Modify parameters and observe changes

Time Allocation

- 45 minutes: Run variations 1-3, analyze results, prepare slides

- 10 minutes: Present findings to class

Deliverables

- Presentation slides (5-7 slides) showing:

- The baseline model and what it means

- Results from all three variations with charts

- Your interpretation of what changes

- (Optional) Extension results for tiered CBDC

- Key insight: What is the most important policy lever for protecting banks from CBDC competition?

References

- Brunnermeier, M. K., & Niepelt, D. (2019). On the Equivalence of Private and Public Money. Journal of Monetary Economics, 106, 27-41.

- Bindseil, U. (2020). Tiered CBDC and the financial system. ECB Working Paper Series, No. 2351.

Show Model Answer Presentation

Slide 3

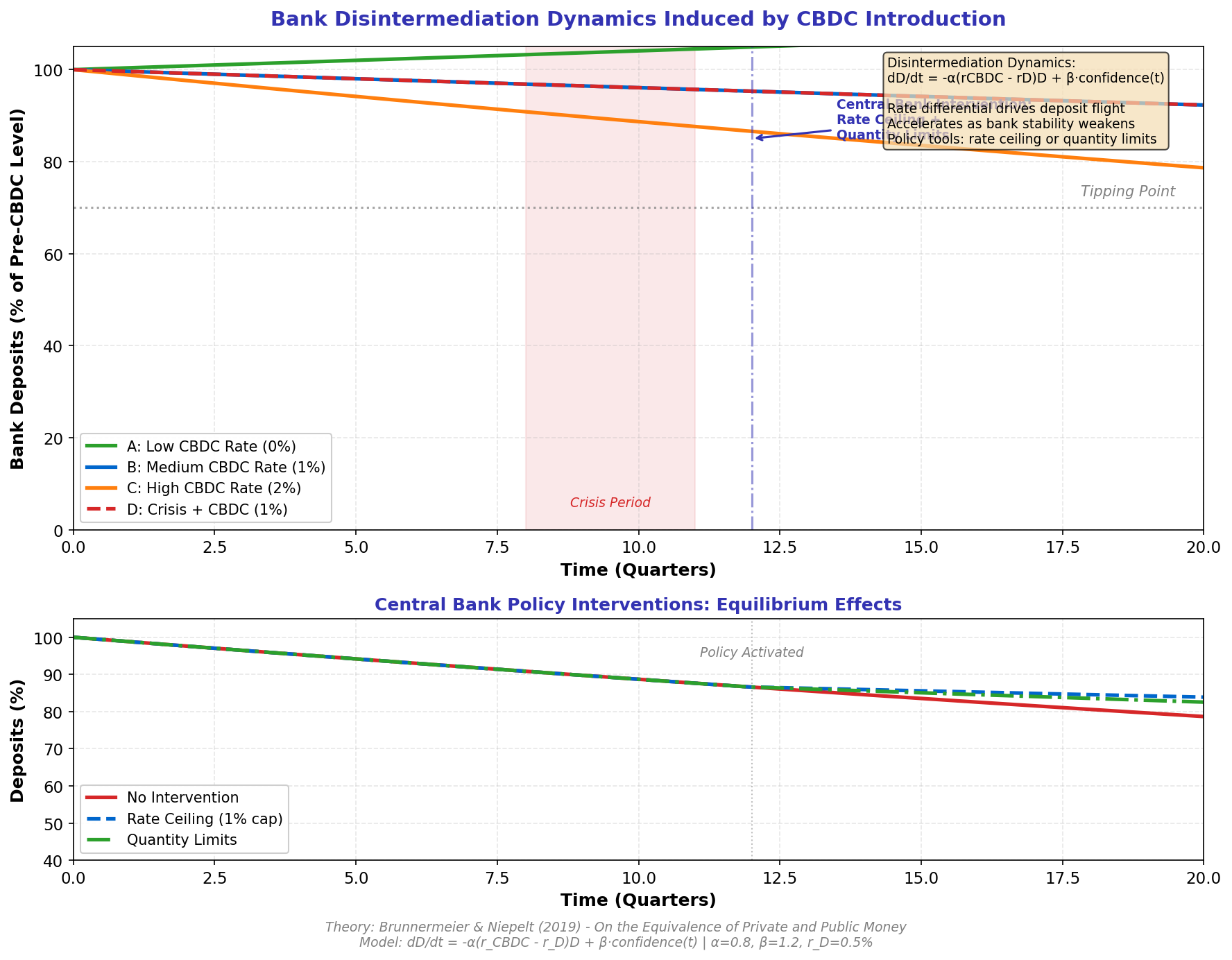

Baseline Results: Four Scenarios

Key Findings:

- 0% CBDC rate (green): Deposits barely change (<5% loss over 5 years)

- 1% CBDC rate (blue): Deposits fall to ~85% after 5 years

- 2% CBDC rate (orange): Deposits crash to ~65% (35% loss)

- Crisis + 1% CBDC (red): Combined shock drives deposits to ~70%, nearing tipping point

Slide 4

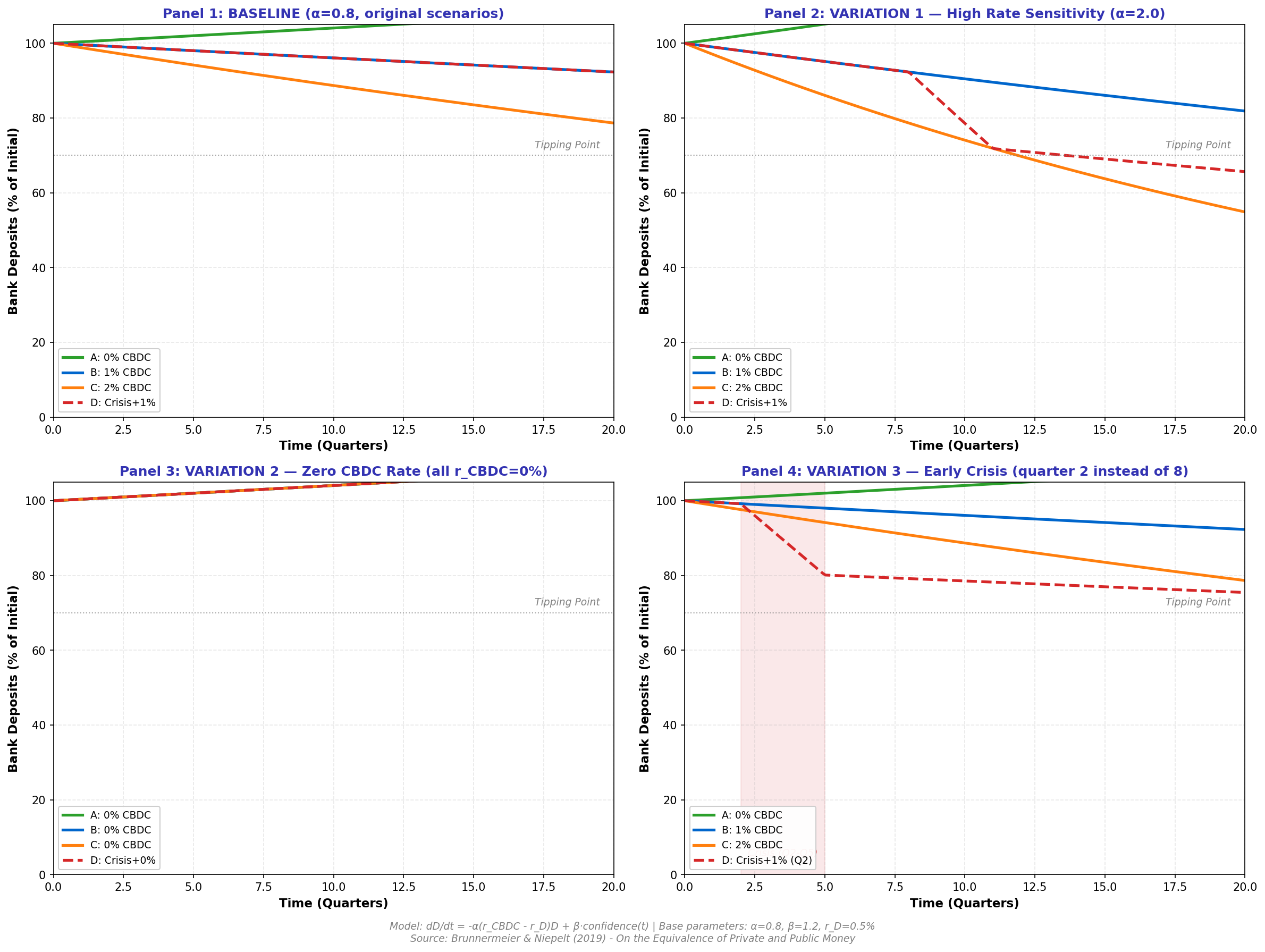

Variation 1: High Rate Sensitivity (α = 2.0)

Panel 2 (top-right): When α = 2.0 instead of 0.8, deposit outflow accelerates dramatically.

Result: With 2% CBDC rate, deposits collapse to ~40% (60% loss) — bank failure territory.

Interpretation: If people are highly sensitive to interest rates, even small CBDC rate advantages trigger massive disintermediation.