This lecture establishes the conceptual foundation for the entire course. It traces fintech's evolution from the first credit cards in the 1950s to today's embedded finance era, examines how the 2008 financial crisis catalysed the modern fintech boom, and maps the spectrum of collaboration models through which banks and fintech companies interact. By the end, you will have both a vocabulary and a five-question evaluation framework applicable to any fintech company you encounter.

- Describe the defining characteristics of fintech and trace its historical evolution from early electronic banking to modern embedded finance. [Understand]

- Explain how the 2008 financial crisis acted as a catalyst for fintech innovation by eroding trust in traditional institutions. [Understand]

- Classify the major collaboration models between traditional financial institutions and fintech companies. [Apply]

- Compare the competitive advantages and disadvantages of incumbent banks vs. fintech startups across key service dimensions. [Analyze]

- Evaluate which collaboration model best fits a given strategic scenario. [Evaluate]

Why Fintech Matters

Frames 1–5 · Opening, Ecosystem, Personal Connection

Welcome to Financial Technology. This course examines how technology is transforming every corner of financial services — from payments and lending to insurance and wealth management. This first lecture establishes the foundation: what fintech is, where it came from, and where it is going.

Think about the last 48 hours. How many financial transactions did you make? How many involved a traditional bank branch? Now open your phone — how many apps touch your money? Banking, payments, investment, insurance? Each one is a fintech story.

Count the financial apps on your phone. For each, ask:

- Is this from a traditional bank, a fintech startup, or a big tech company?

Bring your count to the discussion. Most MSc students have 5–10 financial apps — and most are not from their bank.

"The revolution started in a garage, not a boardroom. This is the tension at the heart of fintech: speed vs. scale, innovation vs. regulation."

Foundational Concepts

Frames 6–9 · Definitions, Seven Verticals, Timeline, Value ChainWhat Is Fintech? Definitions Across Perspectives

The term "fintech" was first used in the early 1990s but gained mainstream adoption after 2010. One reason the concept resists a single clean definition is that every stakeholder emphasises a different dimension of it.

| Perspective | Definition Focus |

|---|---|

| Academic | Technology-enabled financial innovation |

| Industry | Companies using technology to improve financial services |

| Regulatory | New entrants requiring new oversight frameworks |

| Consumer | Faster, cheaper, more accessible financial products |

Academics see innovation. Industry sees competition. Regulators see risk. Consumers see convenience. Fintech is all four simultaneously.

Fintech is not a product — it is a force that reshapes how financial services are created, delivered, and consumed.

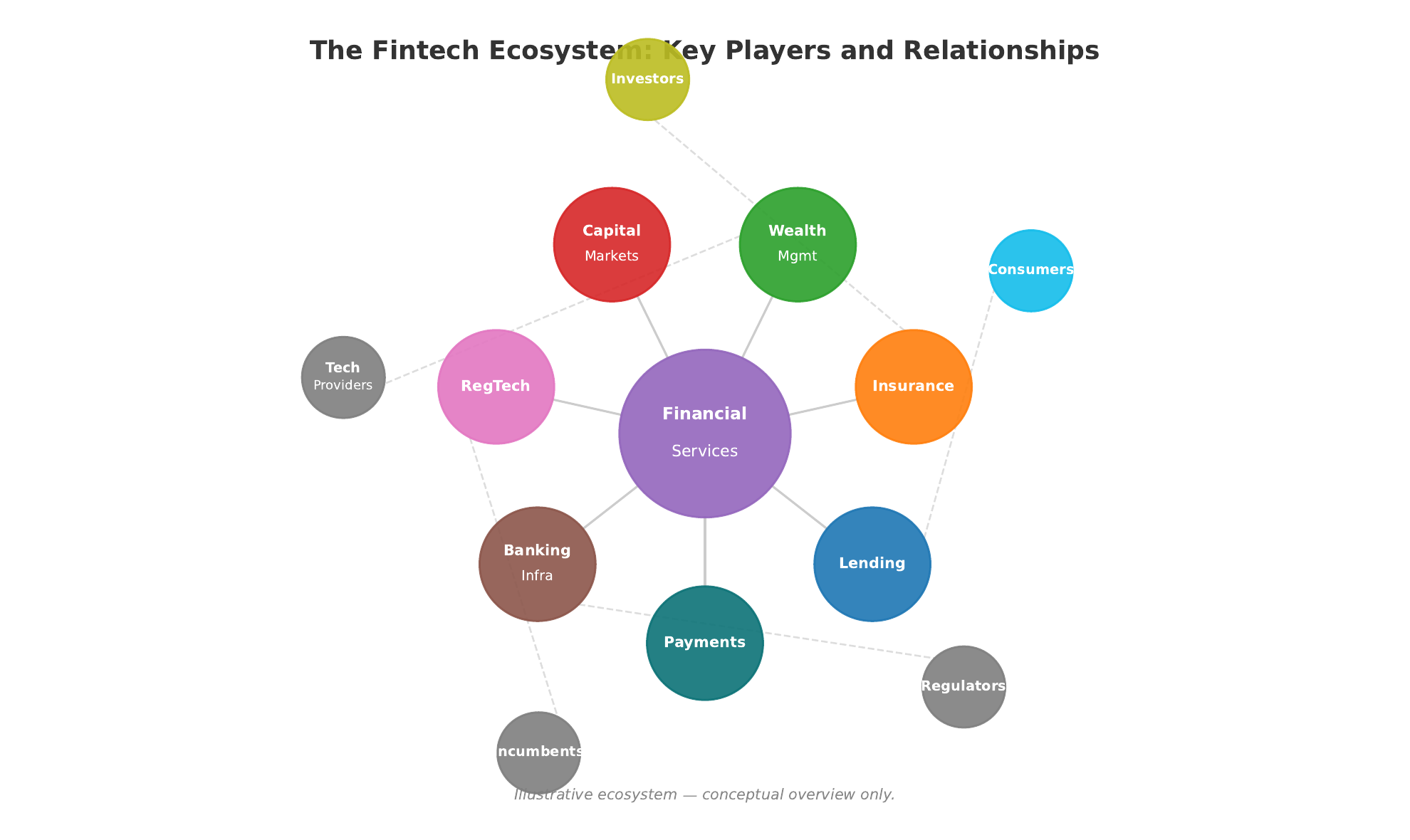

The Scope of Fintech — Seven Verticals

Fintech is not a single industry but a cluster of distinct markets, each with its own dynamics, regulation, and competitive landscape. This course is structured around them:

- Payments — mobile wallets, real-time transfers, cross-border remittances

- Lending — peer-to-peer, alternative credit scoring, buy-now-pay-later (BNPL)

- Insurance (Insurtech) — on-demand, parametric, automated claims

- Wealth Management — robo-advisors, micro-investing, social trading

- Capital Markets — algorithmic trading, tokenization, crowdfunding

- RegTech — compliance automation, identity verification, transaction monitoring

- Banking Infrastructure — neobanks, Banking-as-a-Service (BaaS), open banking APIs

Each vertical is a lecture in this course. Today we see the forest; starting with Lecture 2, we examine each tree. Lectures 3–7 each deep-dive into one or more of these verticals.

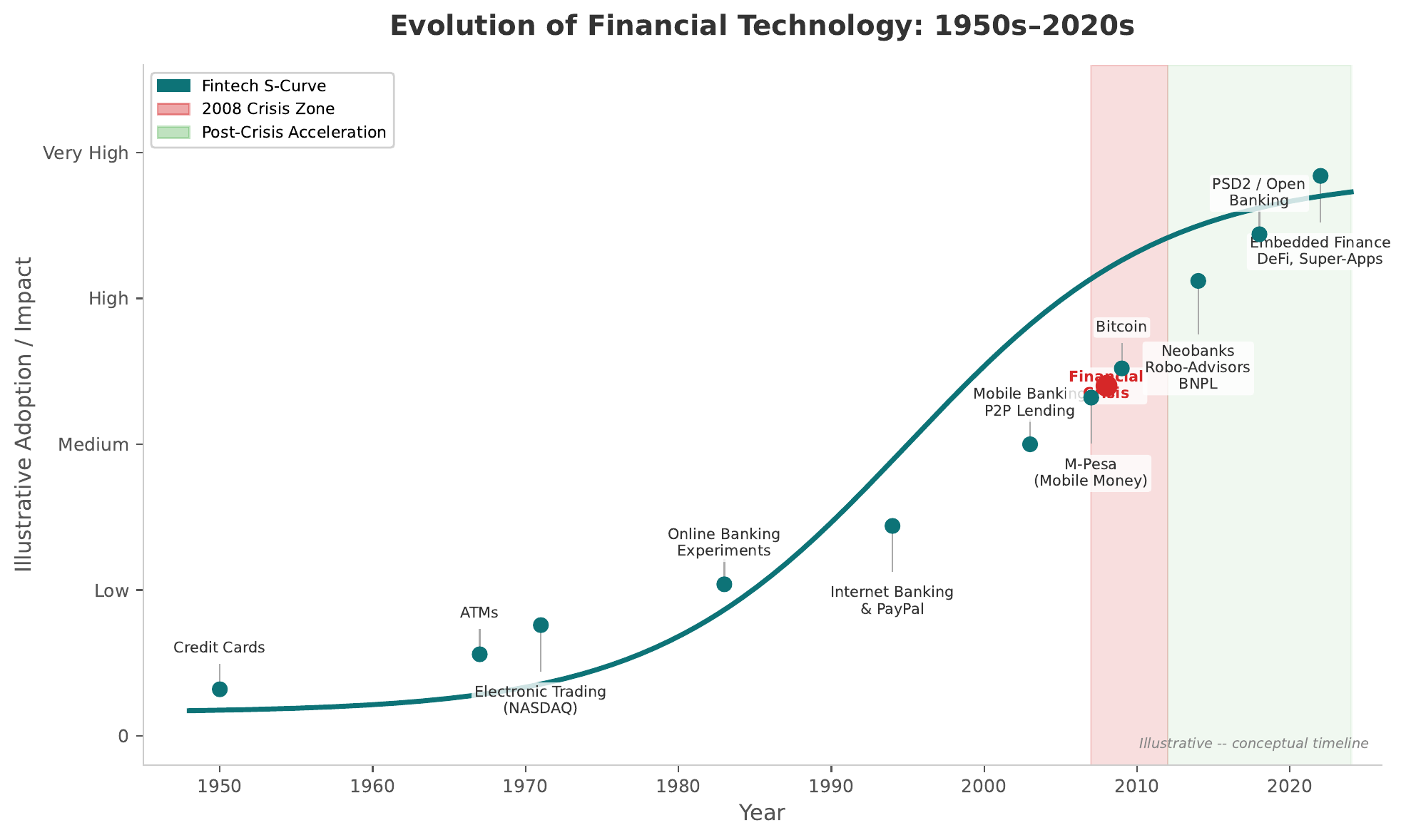

From Abacus to Algorithm — A Timeline of Financial Innovation

- What you see: Major fintech milestones from the 1950s to the 2020s — credit cards, ATMs, online banking, mobile payments, blockchain, embedded finance.

- Key pattern: The pace of innovation accelerates. The gap between credit cards (1950s) and ATMs (1960s) was a decade. The gap between mobile payments and blockchain was just years.

- Takeaway: Each wave builds on the infrastructure of the previous one. Today's innovations stand on decades of accumulated technology.

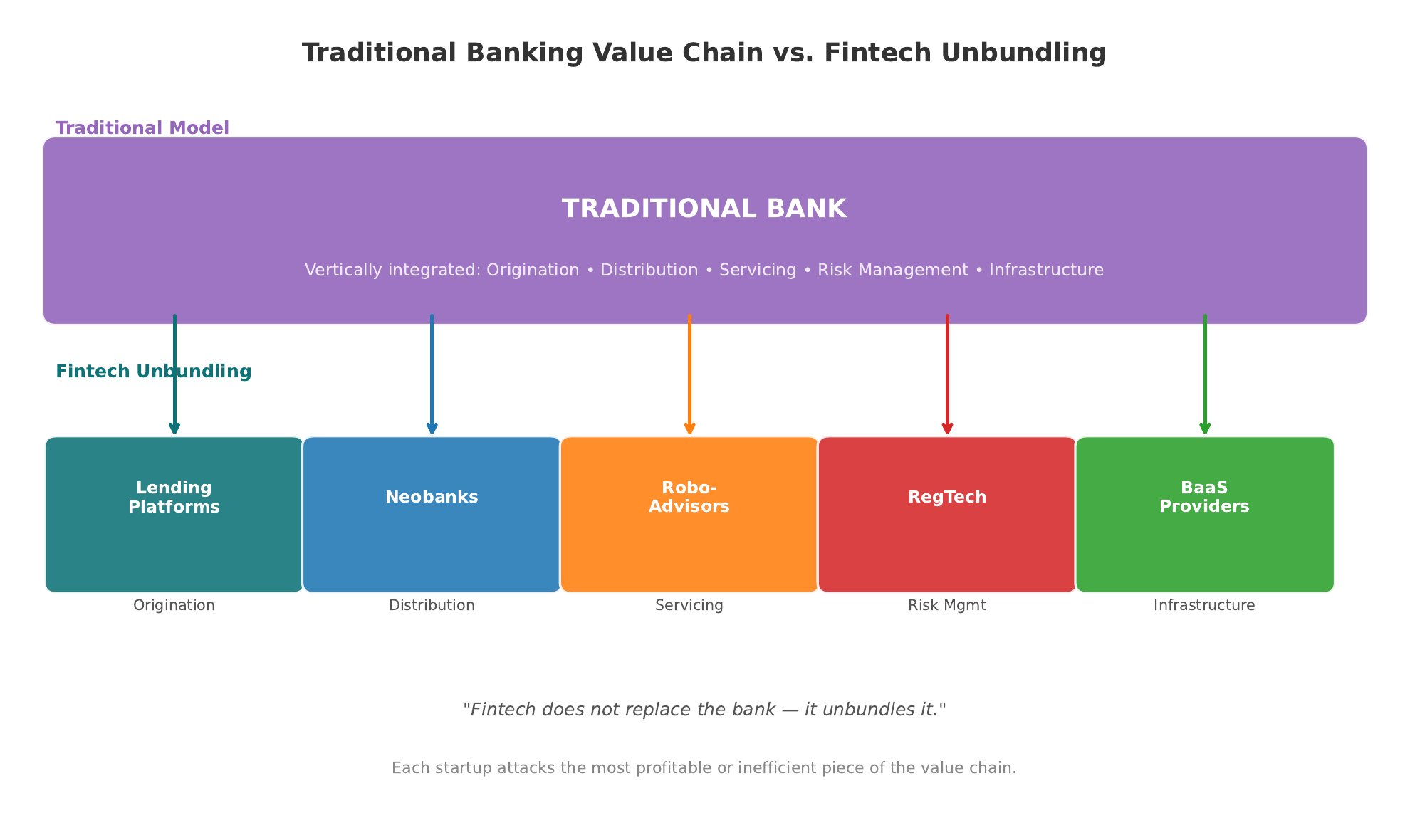

Traditional Banking vs. Fintech — What Changed?

- What you see: The traditional bank as a vertically integrated institution versus specialized fintech companies attacking each layer.

- Key pattern: Fintech does not replace the bank. It unbundles it — each startup attacks the most profitable or most inefficient piece.

- Takeaway: The question is not "Will banks disappear?" but "Which parts of banking can survive unbundling?"

The Great Recession Catalyst

Frames 10–13 · Pre-2008, Trust Collapse, Three Forces, Post-Crisis BoomBefore 2008 — The Trust Assumption

Before the financial crisis, the banking landscape was stable and, for incumbents, comfortably defended. The key features of the pre-2008 era were:

- High trust in institutions — taken for granted rather than earned

- Limited alternatives for consumers; banking choice was narrow

- Regulatory frameworks designed to protect incumbents from competition

- Innovation that happened inside banks — a new savings product, not a new business model

Trust in banks was not earned — it was assumed. The crisis exposed the assumption. In 2007, over 80% of consumers in developed markets expressed high trust in their primary bank.

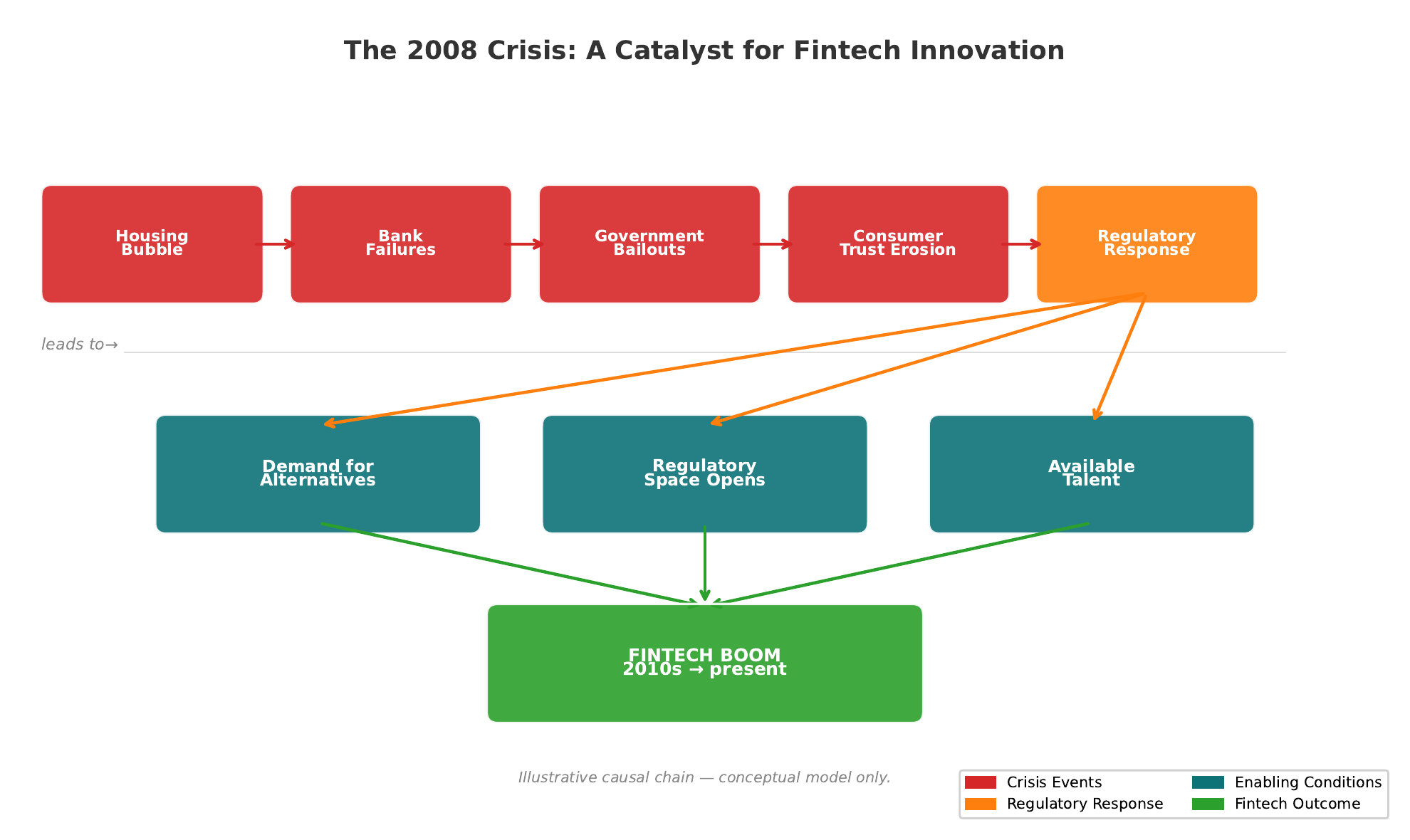

The 2008 Crisis — Trust Collapses

- What you see: A causal chain from the housing bubble to the opening of space for fintech entrants.

- Key pattern: Each step reduced a barrier to fintech entry. Trust erosion created demand. Regulatory response created opportunity. Unemployment created talent supply.

- Takeaway: The 2008 crisis did not cause fintech, but it removed the barriers that had held it back for decades.

Three Forces That Opened the Door

The fintech boom after 2010 required the simultaneous convergence of three distinct forces:

Fintech needed all three forces simultaneously. Technology alone was not enough — it needed demand and regulatory permission. The smartphone was necessary but not sufficient. The crisis provided the push; the technology provided the path.

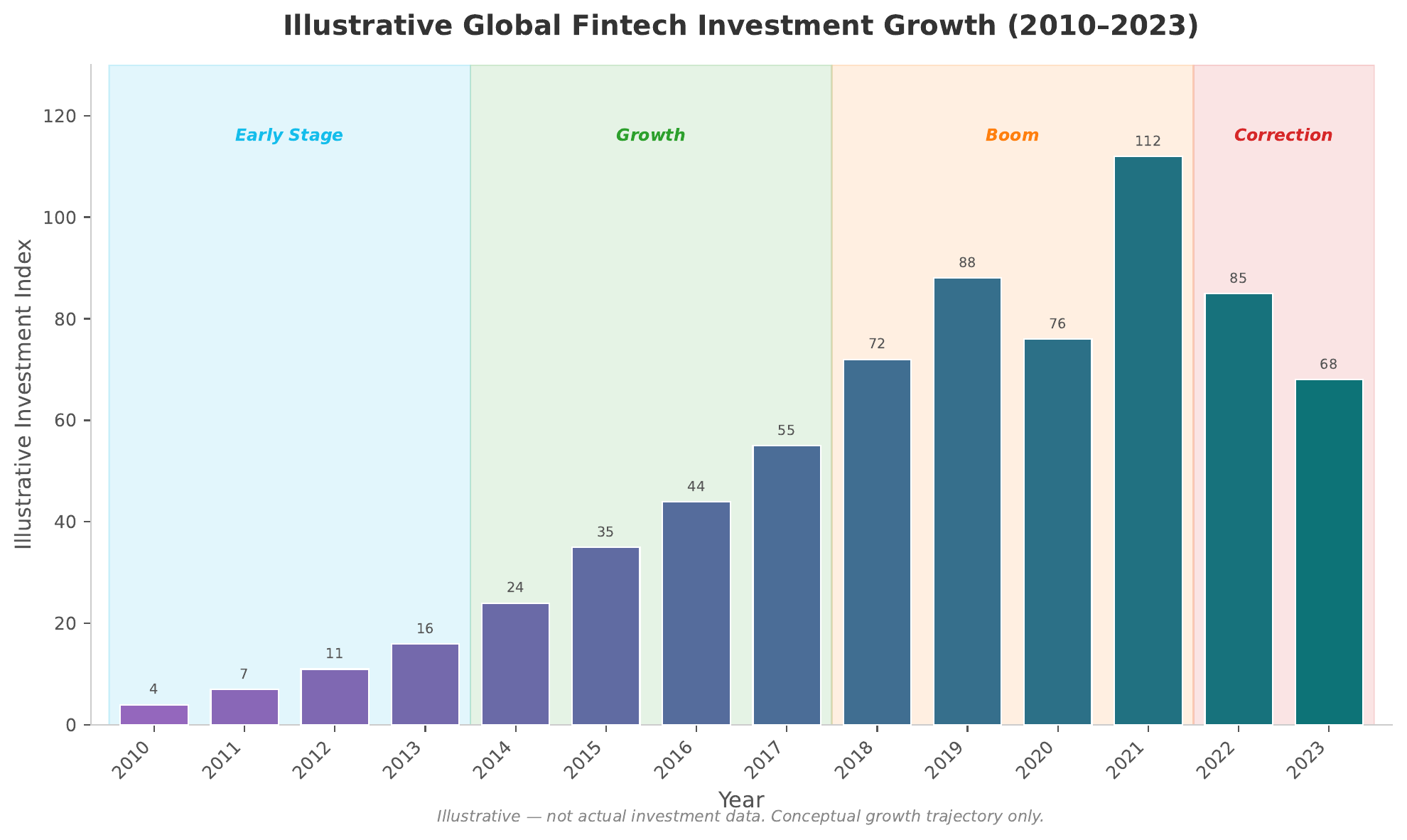

Post-Crisis Fintech Boom

- After 2010, venture capital flooded into fintech. Initial investments were small (seed/Series A).

- By 2020, fintech companies were raising billions in single funding rounds.

- The pandemic in 2020 further accelerated digital adoption — functioning as a second demand shock, though with a different mechanism than 2008.

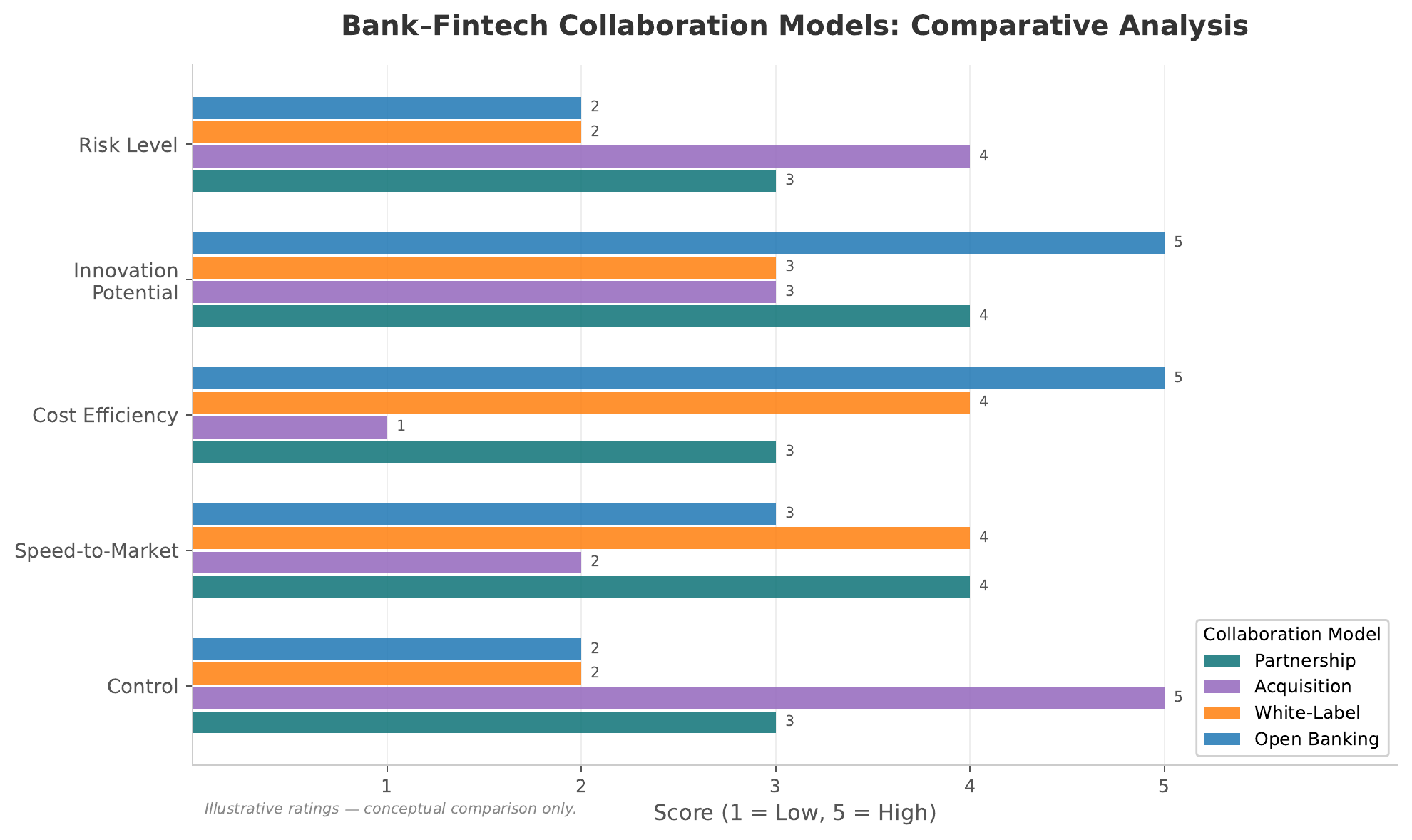

Collaboration Models

Frames 14–17 · Spectrum, Partnership, Acquisition/White-Label, Open BankingThe dominant early narrative — "fintech will kill banks" — has given way to a more nuanced reality: banks and fintechs need each other. The question is not whether to collaborate, but which model to use.

- What you see: Four distinct models for how banks and fintechs work together, scored across five dimensions.

- Key pattern: No single model dominates. Partnerships offer speed but less control. Acquisitions offer control but are expensive and slow.

- Takeaway: The "right" model depends on the bank's strategic priorities and the fintech's maturity.

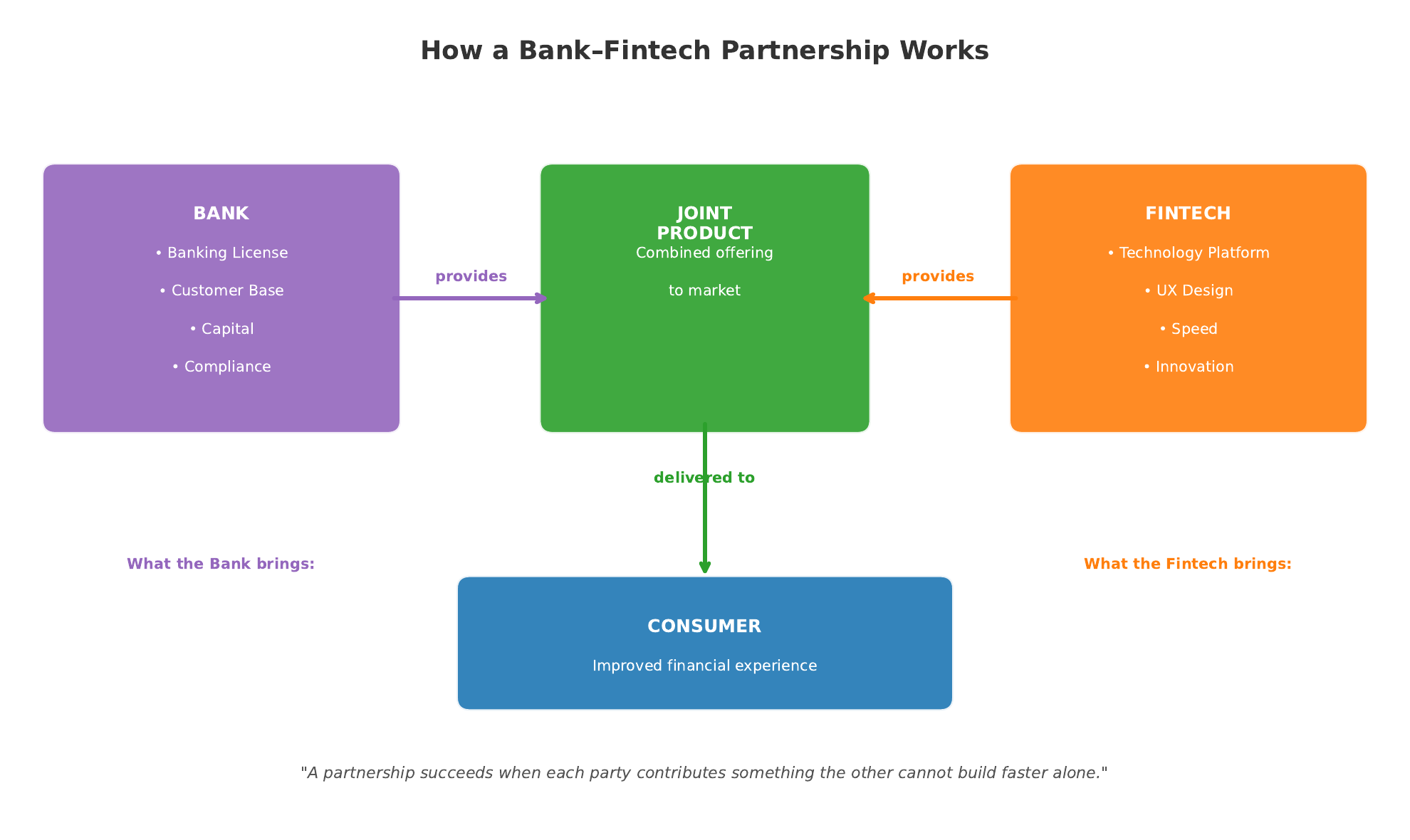

Partnership Model — How It Works

Partnerships are the most common collaboration model. The logic is straightforward:

- Banking license and regulatory standing

- Existing customer base and trust

- Capital and compliance infrastructure

- Technology platform and modern architecture

- Superior user experience and design

- Speed, agility, and innovation capacity

A partnership succeeds when each party contributes something the other cannot build faster alone. Real-world examples: Goldman Sachs + Apple (Apple Card), JPMorgan + OnDeck (small business lending), BBVA + Atom Bank.

Acquisition and White-Label — Two More Paths

Bank buys fintech outright. Gains technology and talent immediately.

Risk: Culture clash kills innovation. The acquired team leaves.

Pattern: Large bank buys Series B fintech for its technology stack.

Fintech builds infrastructure; bank puts its brand on top. Banking-as-a-Service (BaaS). The fintech is invisible to the consumer.

Pattern: Neobank runs on a licensed bank's infrastructure.

Acquisition buys the past. White-label rents the present. Partnership builds the future.

White-label and BaaS are growing fastest — they let banks innovate without building, and fintechs scale without a banking license.

Open Banking — The Regulatory Path

Open banking is a regulatory mandate requiring banks to share customer data via APIs with authorised third parties. It transforms bank data from a competitive moat into a shared resource.

| Regulation | Jurisdiction | In Force |

|---|---|---|

| PSD2 (Payment Services Directive 2) | European Union | 2018 |

| Open Banking Standard | United Kingdom | 2018 |

| PIX + Open Finance | Brazil | 2020–2021 |

| Account Aggregator Framework | India | 2021 |

The open banking flow: Consumer consents → Bank (data holder) shares via API → Fintech app (data user) processes and enriches → Consumer receives improved service. The entire process occurs with the consumer's explicit permission.

Open banking turns the bank's greatest asset — customer data — into a shared resource. The bank that adapts fastest wins. PSD2 (EU, 2018) was the first major open banking mandate; the UK's Open Banking Standard, Brazil's PIX, and India's Account Aggregator followed.

Risks and Challenges

Frames 18–20 · Failure Modes, Consumer Protection, CybersecurityFintech's speed and innovation come with real risks. Understanding these is essential not only for practitioners but for any analyst evaluating fintech companies.

Common Failure Modes

- Regulatory risk — Operating without adequate licences; crossing jurisdictional boundaries without authorisation. The most common cause of fintech failure.

- Trust risk — Data breaches; lack of deposit insurance; unclear complaint resolution pathways. Fintechs can lose consumer trust faster than they built it.

- Scalability risk — Customer acquisition costs exceed lifetime value; unit economics never work at scale. A product can be great and unprofitable simultaneously.

- Systemic risk — Fintech becomes "too connected to fail"; concentration in a small number of cloud providers creates shared vulnerability.

Fintech disruption is not risk-free. The question is whether fintech creates new risks or merely redistributes old ones from regulated institutions to unregulated platforms and, ultimately, to individual consumers.

The Consumer Protection Challenge

Traditional banks are regulated, insured, and supervised within clear legal frameworks. Fintech companies often operate in regulatory gaps — between banking law and technology law, between national jurisdictions, between existing licensing categories.

- Deposit insurance gaps: Funds held in fintech apps may not be covered by deposit guarantee schemes

- Data privacy vulnerabilities: Aggregating financial data creates new attack surfaces and misuse risks

- Algorithmic bias in lending: Alternative credit scoring models can encode and amplify historical biases

- Cross-border enforcement difficulties: A fintech in one jurisdiction serving customers in another falls through regulatory cracks

Innovation without consumer protection is not progress — it is risk transfer from institutions to individuals. This tension between innovation and protection is the central theme of L04 (Fintech Security and Regulation).

Cybersecurity and Operational Risk

| Risk Type | Traditional Bank | Fintech |

|---|---|---|

| Data breach | Internal systems, perimeter defence | Cloud + large API surface area |

| System outage | Redundant infrastructure | Dependence on single cloud provider |

| Fraud | Known patterns, established detection | Novel attack vectors, faster evolution |

| Compliance | Established frameworks, large teams | Evolving requirements, lean teams |

Fintech companies often have larger attack surfaces (more APIs, more cloud dependencies, more third-party integrations) but smaller security teams. The trade-off is speed-to-market versus security-in-depth. L07 (Technology of FinTech) covers identity, encryption, and cybersecurity in depth.

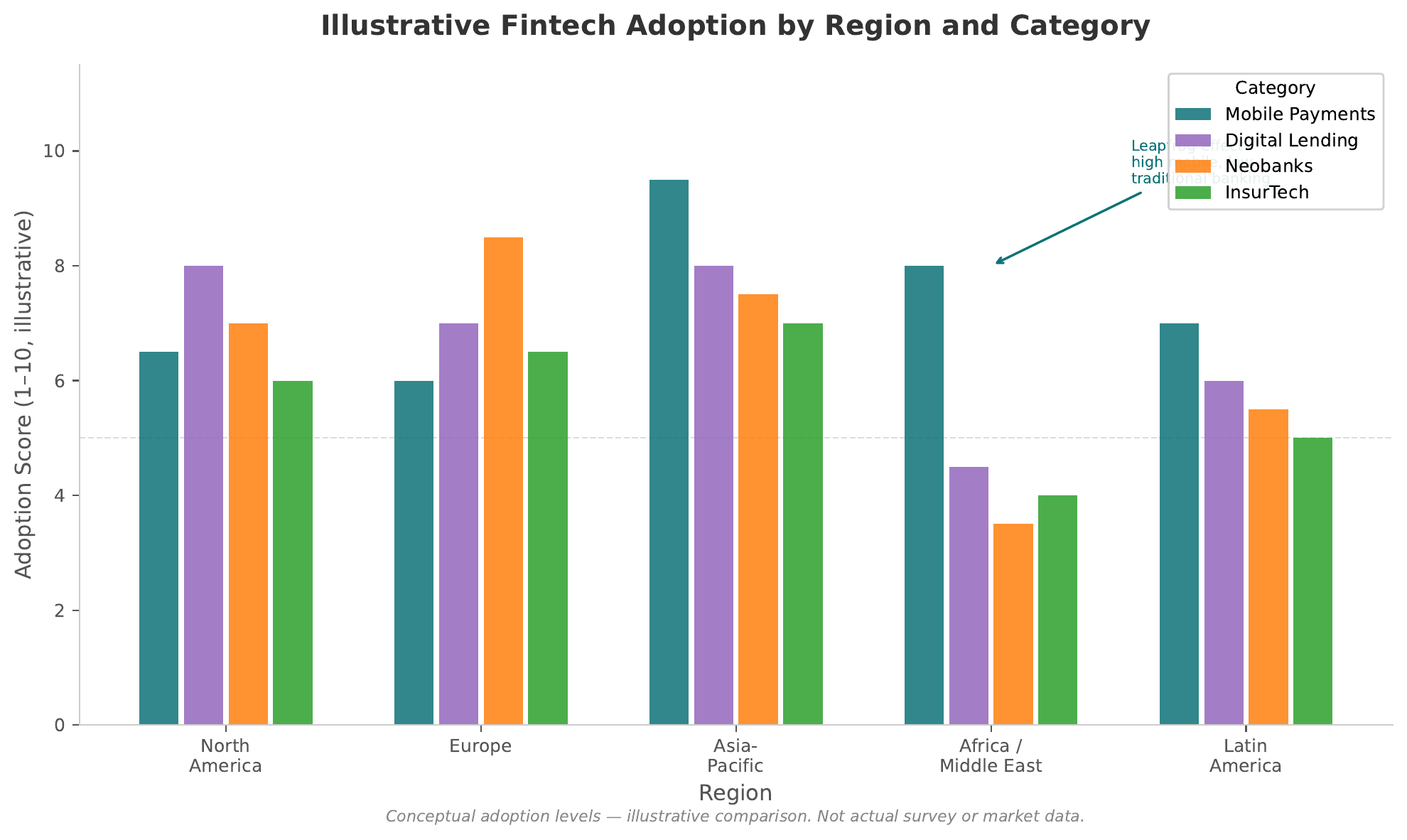

Global Landscape

Frames 21–23 · Regional Patterns, Key Trends, Three ScenariosFintech Around the World — Regional Patterns

- What you see: Fintech adoption varies dramatically by region, with Asia-Pacific and Africa leading in mobile payments while North America and Europe lead in digital lending and wealth management.

- Key pattern: Regions with weaker traditional banking infrastructure often leapfrog to fintech solutions — the "leapfrog effect." Lower incumbency resistance means faster adoption.

- Takeaway: The most transformative fintech innovations (M-Pesa, Alipay, PIX) emerged outside the US and Europe. Fintech is not a Western phenomenon.

Key Trends Reshaping Fintech

Five major structural trends are currently reshaping the industry. Each is examined in depth in subsequent lectures:

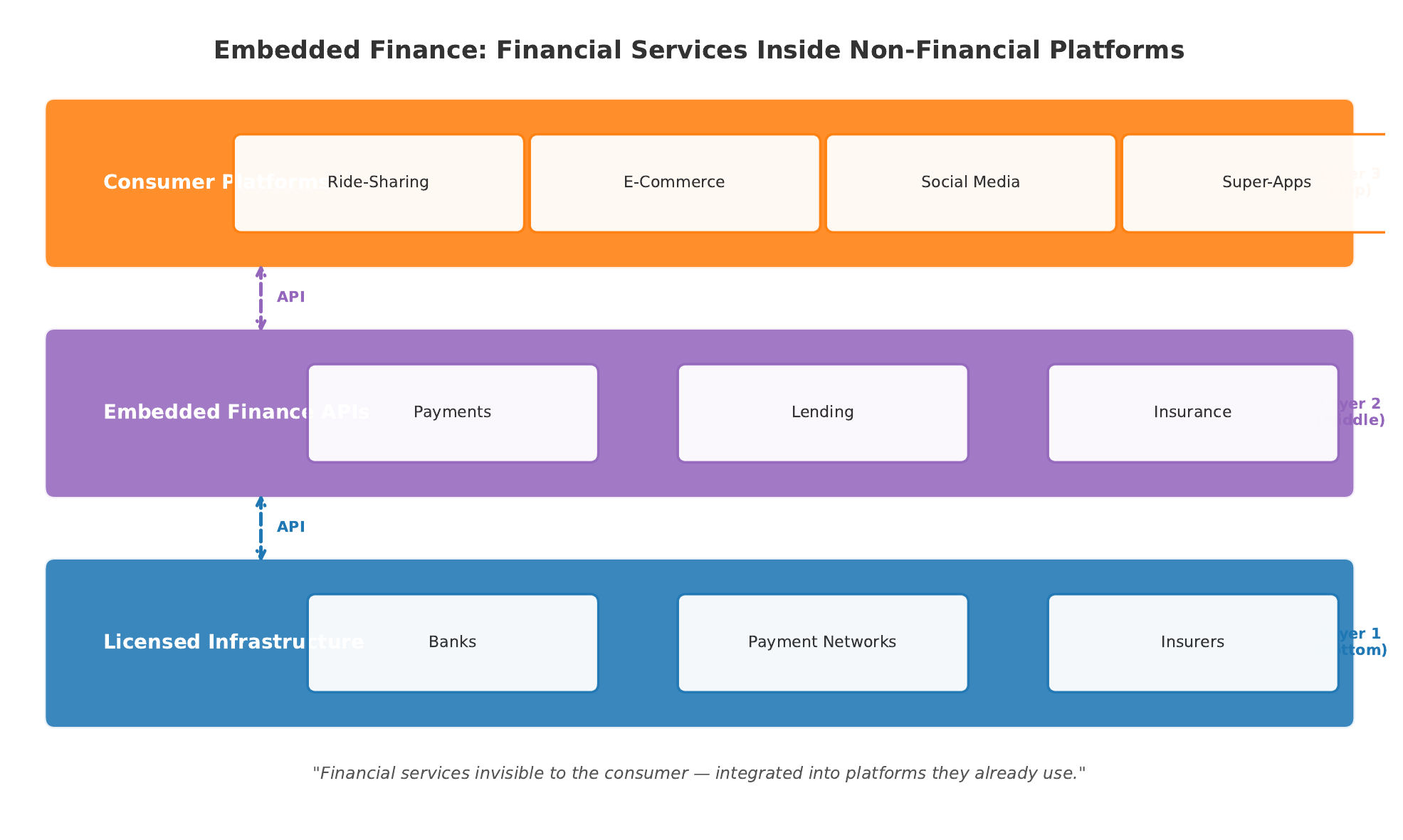

- Embedded finance — Financial services integrated into non-financial platforms (ride-sharing with payments, e-commerce with lending, social media with tipping). Finance disappears into the background of everyday life.

- Neobanks — Digital-only banks challenging incumbents on user experience and fees. Most remain unprofitable but are forcing incumbents to compete on experience.

- Decentralised finance (DeFi) — Financial services built on blockchain, removing intermediaries. High potential and high risk — regulatory status remains unsettled globally.

- Super-apps — Single platforms combining messaging, payments, shopping, and banking (WeChat, Grab, Gojek). Dominant in Asia; emerging elsewhere.

- Sustainable fintech — Green bonds, ESG scoring, carbon-tracking financial products. Growing consumer and regulatory demand is creating a new fintech sub-sector.

Each of these trends is both an opportunity and a threat. The winners will be those who combine innovation with trust. Lectures 3–7 examine these trends in depth. Today we establish the landscape.

The Future of Banking — Three Scenarios

The fintech literature offers three broad scenarios for how the competitive dynamic between banks and fintech resolves over the next decade. None is certain; each is possible:

Result: Banks look different but remain dominant. Fintech becomes a vendor category, not a competitor category.

Result: Banks become utilities — infrastructure, not customer-facing. The "dumb pipe" scenario.

Result: Specialisation by comparative advantage. Probably the most likely outcome.

The most likely outcome is coexistence — but which specific segments go to banks versus fintechs will define the next decade of finance. This question recurs throughout the course, with each lecture adding evidence for one scenario or another.

Stakeholder Impact

Frames 24–25 · Impact Analysis, Financial InclusionWho Wins, Who Loses?

Fintech affects every participant in the financial system, but the effects are neither uniform nor evenly distributed:

| Stakeholder | Gains | Risks |

|---|---|---|

| Consumers | More choice, lower fees, better UX | Less protection, digital exclusion risk |

| Incumbent Banks | Forced innovation, new partnership revenue | Competitive pressure, potential disintermediation |

| Regulators | New regulatory tools (RegTech) | Oversight complexity, innovation vs. stability trade-off |

| Fintech Companies | Large growth opportunity, low barriers | Funding cycle risk, regulatory uncertainty |

| Society | Financial inclusion gains, efficiency | Digital divide, algorithmic bias |

Fintech is not zero-sum. Both consumers and institutions can benefit — but the benefits are not evenly distributed. Financial inclusion — serving the unbanked and underbanked — is examined in detail in L02 (Fintech Ecosystem).

The Financial Inclusion Promise

Over 1.7 billion adults globally lack access to formal financial services. Fintech's greatest promise is reaching them — not through branches, but through smartphones.

How fintech enables financial inclusion:

- Mobile money serving unbanked populations — the M-Pesa model

- Alternative credit scoring using non-traditional data (phone usage, utility payments, social data)

- Micro-investing lowering minimum entry barriers to wealth-building

- Cross-border remittances dramatically reducing transfer costs for migrant workers

If fintech only serves the already-served, it is optimisation, not transformation. Inclusion is the test of genuine impact.

M-Pesa (Kenya, 2007) remains the canonical example. At its peak, it handled more than 50% of Kenya's GDP in transactions. See L02 for the full financial inclusion discussion.

Synthesis and Evaluation

Frames 26–31 · Five-Question Framework, Central Tension, Key TakeawaysFive Questions That Reveal Any Fintech's True Strategy

The following evaluation framework works for any fintech company you encounter — in this course, in the news, or in your career. Apply it consistently and you will see through surface narratives to underlying strategy.

-

Who is the customer?

-

What part of the value chain does it attack?

-

How does it make money?

-

What is its regulatory position?

-

Does it create or capture value?

These five questions work for any fintech company you encounter — in this course, in the news, or in your career. Apply these questions to a fintech you use. You will use this framework in the Workshop C evaluation exercise on Day 5.

The Central Tension Revisited

Technology is reshaping finance — but the outcome depends on design choices.

- Will fintech replace institutions or strengthen them?

- Will it include the excluded or serve only the already-served?

- Will it create resilience or fragility?

These are not technology questions — they are governance, regulation, and strategy questions. This course gives you the tools to answer them.

"Fintech is not a technology story. It is a governance story told in the language of technology."

Key Takeaways

Seven Things to Remember from Lecture 1

- Fintech defined: Technology-enabled innovation that creates new financial products, processes, or business models.

- Historical arc: From credit cards (1950s) through online banking (1990s) to embedded finance (2020s) — each wave built on the last.

- Crisis catalyst: The 2008 financial crisis eroded trust, opened regulatory space, and released talent — creating the conditions for fintech's explosive growth.

- Unbundling: Fintech companies attack specific layers of the banking value chain, not the entire bank.

- Collaboration spectrum: Banks and fintechs interact through partnership, acquisition, white-label, and open banking — each with distinct trade-offs.

- Global variation: Fintech adoption is highest where traditional banking infrastructure is weakest (the leapfrog effect).

- Evaluation tool: Five questions (customer, value chain, revenue model, regulatory position, value creation) reveal any fintech's true strategy.

Key Vocabulary

What Comes Next

Next: Lecture 2 — Fintech Ecosystem. Growth drivers, financial inclusion, trust in fintech, and how behavioural economics shapes digital financial products. L02 begins this afternoon at 11:30.

Before L02, think about: What fintech services do you trust more than your bank? Why?

L02: Ecosystem · L03: Payments · L04: Regulation · L05: Wealth Management · L06: Insurance · L07: Technology

Bring your phone app count from the exercise on Slide 5 to the L02 discussion.

Downloads

All 6 slide variants — PDF formatAll slide variants are available for download. The full variant (31 slides) is the primary lecture document. The mini variants are useful for quick review or mobile reading.